Painting THS-tle

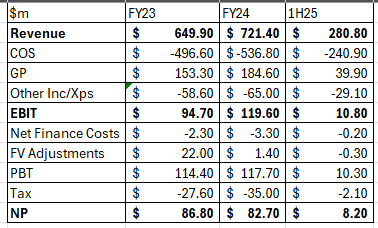

Considering the 1H25 **ACTUAL** performance at Tharisa

Dear reader

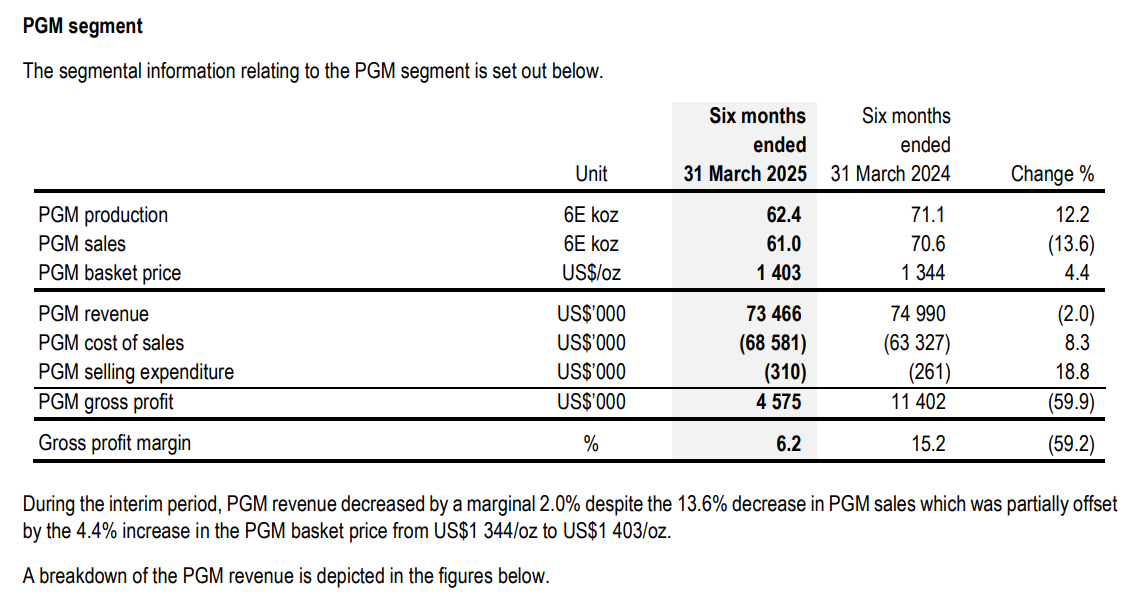

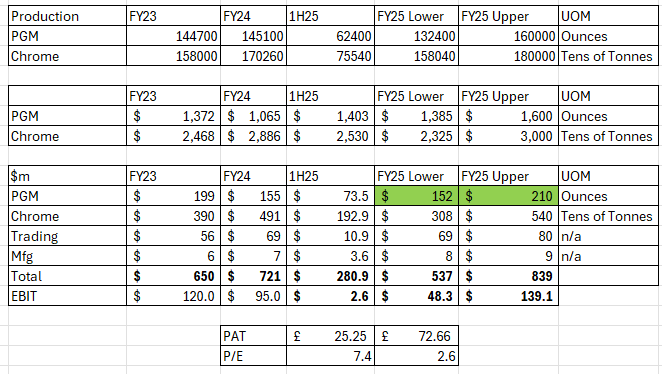

Diving into the detail of the 1H25 results we see an 8.3% increase to PGM cost of sales.

This increase is really just a larger share of shared costs from 35% to 42% so no actual increase other than an increase of proportion.

Interestingly 61koz of sales doesn’t match production, so there’s a timing issue to production that may partially go into Inventory, but also if you multiply sales of 61Koz of PGMs by $1403/oz basket price then it sums to $85m and it doesn’t match the actual $73,466,000 PGM revenue either. There’s about a $12m difference. In 2024 there’s a larger difference. It seems there’s a sliding discount in place that gets silently netted off revenue and from the basket price, just for PGMs. This means my model needs adjusting (see below). There’s absolutely no mention of this hidden revenue reduction in the accounts, and I’ve not seen it ever mentioned in any other analysis of Tharisa.

CHROME

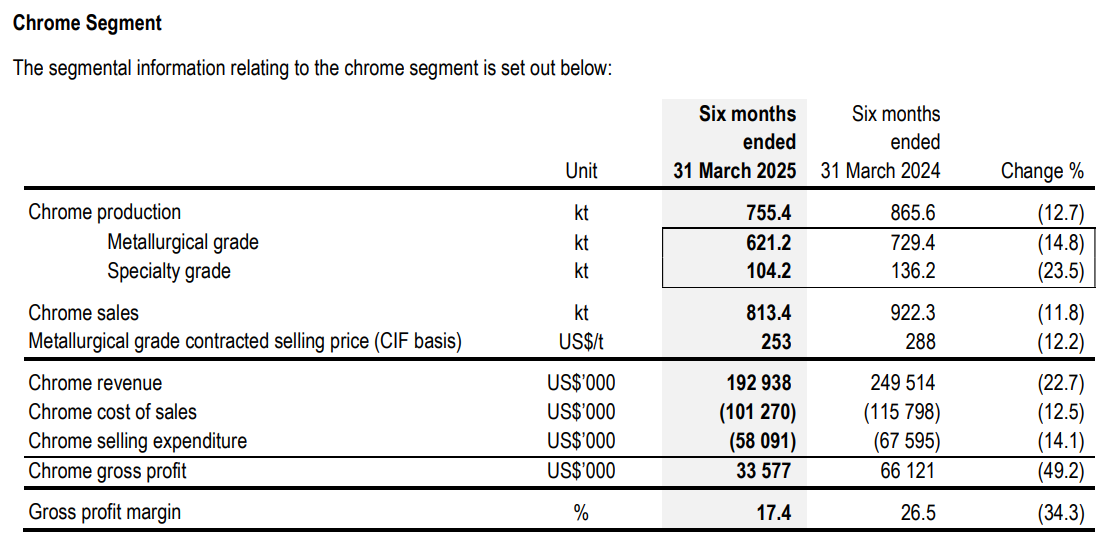

A 22.7% drop in Chrome revenue year on year is a large reason for THS’ fall in profit. The -12.5% fall in cost of sale is just a reduction of proportion (with PGMs).

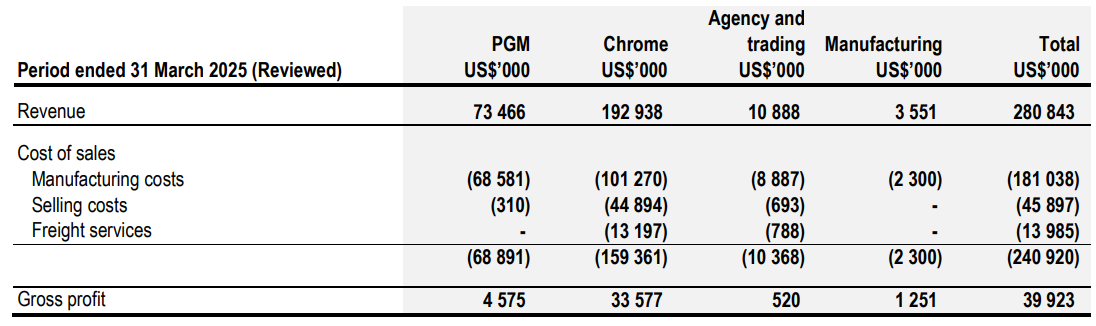

But Chrome is not the only reason. Agency and Trading is down from $41.9m in 1H24 to $10.9m in 1H25, although this only reduces gross profit by $2.4m. This is because it’s a low margin activity. So not really an issue.

An activity of operating a 3rd party chrome plant that has come to an end it seems. It makes sense to focus on producing chrome instead of “toll milling” as this appears to be. The bulk of profit is in the price of chrome not the fixed toll for processing someone else’s chrome.

The P&L outcome is at the top end of expectations, even if net profit is 80% down on FY24, in the first half.

My model changes to reduce PGM income by a sliding scale based on my finding. The impact on the lower and upper price earnings is actually not that significant. It moves to a 2.6X - 7.4X lower and upper forecast.

The model has the 1H25 actuals, along with a forecast FY25 out turn for 2H25 i.e. from 1st April 2025 - 30th September.

Chrome as I write is $300/tonne according to THS. It has bounced strongly. In my lower case I’m still using a low $232.50 per tonne forecast price to arrive at a $48.3m result for FY2025. It is almost certainly going to be higher than this.

PGMs

Of course the above analysis assumes either a $1385 basket in the lower case or $1,600 basket for the upper case. Which is it?

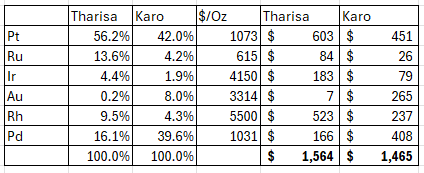

Well the latter, pretty much. Today’s $1,564 basket price is now a mere $36 below the upper end assumption for PGMs. The basket is heading higher and I suspect $1600 will prove to be conservative.

KARO

Of course Karo’s basket at $1,465/ounce is also nearly $100/oz higher compared to my March article. THS (who holds 65.59% of Karo) tell us the go slow continues, although studies, infrastructure and optimisations continue. It makes sense. If PGMs are going to strengthen in price in 2025 (or beyond) then the attractiveness only increases.

Karo is a Tier 1 low-cost, open-pit PGM and Chrome asset located on the Great Dyke in Zimbabwe capable of 174 koz/year for 11 years LoM and NPV10 of $494m. Given the 131.4Koz it would more than double Tharisa’s PGMs and likely take Tharisa above $1bn revenue a year. The capital cost is $391m and $154.8m has so far been committed and $98.1m spent with spending slowed while debt capital is considered.

The combined resource size for Tharisa Mine and Karo comes to 1 billion tonnes containing 52 Moz of 6E PGMs. Tharisa Mine has a potential 40yr life, of which the first 18 will be open pit, with a 20 year underground option. The I&I of Karo is 10Moz of 6E PGMs. This is based on 100m depth even though the resource goes to 1000m. In fact previous estimates of Karo by Zimplats, were 96Moz of 4E PGMs (so more inc. 6E) or c.10x the resource being currently measured in the Stage 1 production plan.

Other benefits to Karo is a supportive tax regime of 15% for 10 years and ability to export (rather than sell to a government monopsony), and no BEE (black empowerment) legislation where you effectively give away a share of ownership for nothing. There are other miners in the area like Zimplats and AngloPlat so an educated and (mining) experienced workforce too.

If we consider that Zimplats is ASX listed and valued at A$1.33bn today. That’s a £645m market cap or £1m per Koz produced per year, or £29,000 per Koz per year remaining (i.e. a 34 year life).

Using that logic for Karo that would equate to a £557m valuation for THS based on an 85% ownership (i.e. 100 years x 226 koz x £29,000 = £655m) once built. Karo’s $391m capex less $154.8m spent leaves $236m or £176m left to spend implying a large upside if Karo were completed on a read across. Appreciating that a half-built mine is worth not as much as a completed and producing mine!

Consider too that Zimplats 2024 profit was $8.2m vs $563m in 2021. Will the good times come back? Its £645m market cap was ~£2bn back in 2021.

That implies if PGMs boom again like in 2021, that the market would - or at least should - value Karo at £1.66bn - again on a read across basis and once it has been completed - this would require 15 months lead time, we are told.

Will all of these read across benefits accrue to THS? No, not 100% of them. The idea is to finance via debt and project finance, and potentially via an offtake and a strategic investment. This slide explains the progress made in finalising a deal for Karo. Some aspects are in advanced talks or are “progressing” but have taken a lot of time.

REDOX

It is interesting to note the update that:

“Redox One has again met its development timelines and we are on track for building and testing larger long storage redox flow batteries using chrome-based electrolytes manufactured by the Group, by the end of this calendar year, as we ramp up to develop and test MW scale batteries.”

These could offer an alternative to Vanadium Flow batteries where Chrome is an awful lot cheaper, and plentiful, and be a compelling business in its own right.

To develop MW scale is an impressive goal. Given the recent power blackout episode in Spain inexpensive MW scale BESS would be worth a great deal to utility companies all over the world.

Shareholder Returns & Cash

A $5m buyback and 1.5c dividend will cost $9.4m total.

Considering current assets - current liabilities are a net $138.8m of net current assets, that’s 60% of the market cap. Long-term net assets are $792.3m less -$177.1m.

That’s an incredible 68% discount to NAV. Where the NAV of something like Karo is at book and not at the read across value - considering Zimplats.

Operating Cash flow before w/c changes in 1H25 was $43.5m, reduced by around 60% from the average prior year rates of cash flow generation which averages around $200m per year.

Conclusion

Yesterday I said the weak 1Q25 result was compensated by a stronger 2Q25 result. But the strong 1Q25 unit selling price was detracted by a weaker 2Q25 price.

Can weather disrupt again in the future? Absolutely. Would every other PGM miner be similarly affected? Tharisa mine is an open pit so the underground miners presumably less so.

The forward picture is pretty positive and the Interim Report offers further perspective why.

I hope the two articles, yesterday’s “painful THS-tle” and today’s “painting THS-tle” offer perspective why I believe this OB25 for 25 idea will rebound in 2025.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Any ideas about what fair value represents on this company?