SALT 2023 y/e update

Kicking the can.....

Dear reader,

MicroSalt disappointed markets today, falling to an 86p bid / 93p ask. Those whom are disappointed point to things like “tiny revenues” (£0.6m) and a “weak balance sheet” (31/12/23 was pre-IPO). Such analysis completely misses the point.

SALT is a food technology play. The whole business is asset light and whilst there is inventory for its B2C salt products these are a sideline. It’s not ever going to shake down enough salt shakers to make serious profits. In previous articles I’ve shown how the real thing is its B2B business.

An agreement with a B2B business will be a licencing deal. SALT will not be expected to produce any product themselves. They will simply earn a royalty on production. How strong a balance sheet do you need, exactly, to permit a licence deal and to accept royalties?!

Analysing the 2023 numbers has limitations too. SALT was on life support as a private company owned solely by TEK cash strapped and scraping pennies to afford an IPO. So why would you expect some amazing FY2023 numbers? It’s bizarre if you do - you need to take a reality check.

The IPO was post period February 2024 which raised £3.1m. It was the most succesful IPO in London in 2024 and probably in 2023 too. The recent warrant call may raise £3.4m more (although it’s likely to raise about 2/3 as TEK probably cannot find £1.2m and it only has 1 more week to do so). So SALT actually has something like a two-year runway - assuming zero revenue growth - and a far stronger balance sheet than looking backwards as at 5 months ago would reveal.

As for progress with B2B, yes, a rapid agreement by May 2024 would have been lovely. But B2B food technology moves conservatively. It has to. Big, global players move slowly like supertankers. There are tick boxes around compliance, supplier approval, safety, retooling, sign off and product approval, sales and marketing plans.

Today we’ve been given a date for customer B(epsi) - Q3 2024. Q3 begins in 32 days time. Reading the chat rooms no one appears to have picked up on this nugget.

Or this one:

Either one of these “commercial volume orders” and “purchasing agreements” will be transformative for SALT.

And SALT are INCREASINGLY confident. Let’s also see what happens with Warrants. In my article a few days ago (EYE SAY!) I set out all the insiders with warrants. Will insiders use or lose their warrants? That will be a hugely bullish signal if they use.

SALT speaks to significant progress in 2023.

“significant progress regarding positive trials undertaken during this year so far, or indeed the deepening of knowledge and relationships MicroSalt has with our key B2B customers and target customers. Furthermore, we are increasingly confident of announcing further commercial volume orders with Customer B in particular, in the third quarter of 2024.

In addition to our focus on B2B sales of MicroSalt® to food manufacturing companies where the Company has made substantial progress, MicroSalt has launched its low sodium salt in saltshakers during 2023. Approximately 400 supermarkets now carry these better-for-you saltshakers.

Beyond our primary focus on sales and marketing, I'm pleased to advise of several other developments during 2024, including:

- New employees, namely a new UK sales manager and a US based group financial controller;

- R&D projects focused on three new iterations of MicroSalt to expand its effectiveness across various additional food formulas and environments. We expect this should lead to entrance into additional markets and potential applications for MicroSalt both short and long term.”

Conclusion

Whilst today’s FY2023 results aren’t sparkling, did you actually expect them to be? The period relates to the pre-IPO and when it was on life support from TEK.

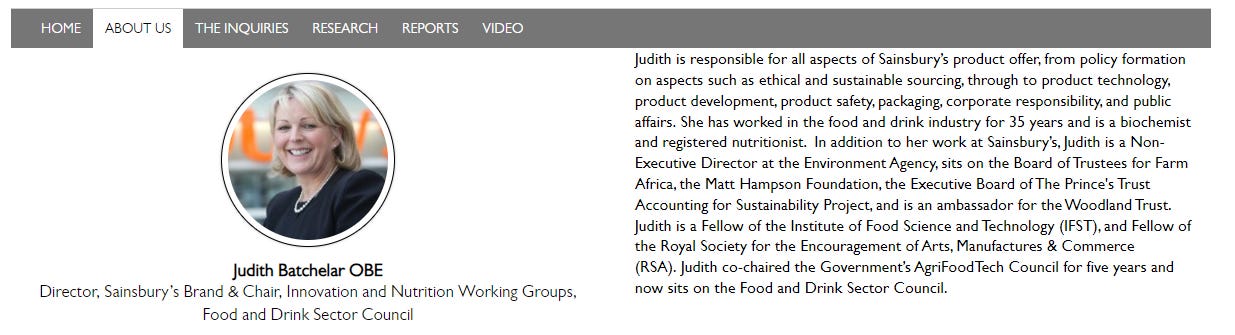

Post-IPO is has cash, it has its listed Plc status and the backing of ex-Sainsbury’s Judith Batchelor OBE, and backing from Chef Jack Stein is post period too. It is having some very interesting conversations with very large customers.

Apart from Judith’s experience at Sainsbury’s (as Director for overseeing the Sainsbury’s Brand), her current other commitment is as Chair at the FDF - the Food and Drink Federation, UK.

… Which is a powerful voice for food manufacturing… more than 1000 members.

SALT is actually well funded, albeit post period, has a great CEO/Chair, a great technology, a granted patent - preventing imitation - and is knocking on the doors of Food Technology businesses offering to solve one of their biggest challenges.

To red flag this is to lack understanding, instead I believe we will see SALT…..

salto de precio(As they would say in Mexico)

….later in 2024.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

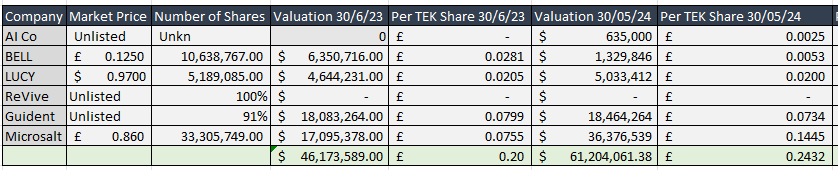

PS if you hold SALT via TEK here’s the 30/05/24 position:

(Each 9.8p TEK share buys the equivalent of 14.5p of SALT shares (33% off); plus shares in LUCY, BELL, Guident, ReVive, AI Co. are all bundled in for free)