Should you CRCL and never rebuy?

And is Corcel's past also its future?

Dear reader,

Management Teams sometimes exit and a replacement team parachutes in. The past team’s “hot prospects” get sold or dwindle and the new team acquire new opportunities.

I was deeply sceptical of Corcel whom I knew to have a Papua New Guinea Nickel business which morphed to an Australian Rare Earths, then onwards to an Angolan Oil business and finally today to a Brazilian Gas business. I say “a business”, it is an explorer and it is prospecting.

By my reckoning they’ve raised a load of money and spent most of that in 2024. 3bn shares in issue means holders have been diluted a fair bit if you were unlucky to own going back one or more years. As at 30/06/22 there were 401m shares in issue for example. (Ouch!)

I watched a recent Bing Bong Bing Bong stock box interview. Out of curiosity I ran the numbers. I’m not sure why I did but I was curious.

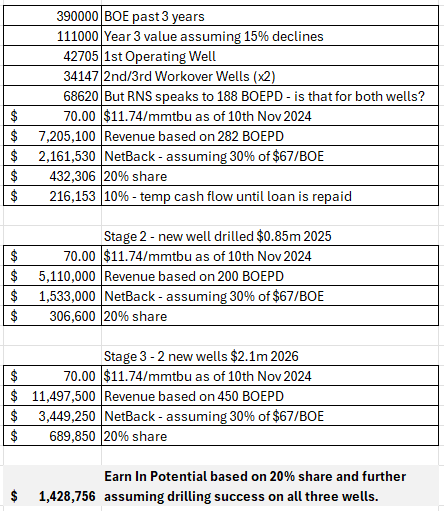

The interview discusses the Brazilian gas field it is prospectively working over ahead of a potential buy. The interviewer confuses a loan made by Corcel to the small owner called Petroborn with the large Brazilian company Petrobras. Piecing together the clues we find that production was 390kboe over the past 3 years. Assuming a 15% decline that means a year 3 of about 111kboe. The current well producing at 117boepd equals 42.7kboe meaning the two workovers are about 34kboe each. This is confirmed by the RNS speculating on a rate of 188BOEPD which equates to 68kboe. Brazilian gas prices were last assessed as $11.74/mmbtu so that equates to something like a $2.2m netback and a $432k share for Corcel at 20% but until the $550k loan is repaid proceeds are paid at 30% - so ~$650k means it will take 10 months production to repay the loan.

If Corcel proceed, a further $0.85m tranche is advanced in 1H25 (i.e. the repaid loan is lent a 2nd time!) with a further $2.1m advanced in 2026. It’s not made clear in the RNS but it appears an “advance” constitutes merely a further loan or shall we say a forward payment and would mean a total loan of $3.5m (less repayments based on 20%-30% of revenue).

It’s not clear to me how CRCL intend to fund these follow on advances. Well, it is clear. Dilution. It has to be. It would seem you could just about fund Stage 1 and 2 out of existing cash but $2.1m in 2026? No, I think a further raise will be required for that. However the 20% share, assuming success in the 2 workovers and 3 new wells and CRCL could get close to 1,000 BOEPD (as set out by the interviewee) would be worth around £1m net profit per year, suggesting that to buy out the remaining 80% at £12m or below would be reasonably good value (Less than 3X EBITDA earnings). The RNS suggests debt funding might be possible for that (let’s say) £12m. After all, if growing cash flows can be demonstrated, further expansion should be easier to fund. Cash flow from operations will presumably be used to repay the $3.5m of loans to Petroborn too.

There is also the further upside of the potential purchase of 100% of the adjacent 182km² TUC-T-172 exploration block too.

Angola

In addition to Brazil, Angola had a number of inconclusive test results in 2024, at its KON-11 Block (Tobias Field) in Angola. There were specific reasons for this, and the next step is to pursue an enhanced understanding of the subsurface conditions including the natural fracture system characteristics, any formation damage and residual issues with water inflow should be the current focus.

Ex-Chairman Antoine Karam: "While initial results in Angola have not allowed immediate reactivation of the Tobias Field as originally hoped, the block partners are undertaking a detailed review of how to best utilise and exploit the two wells recently completed and further develop the full potential of the block. The Company and its block partners believe KON-11 continues to offer significant developmental potential and that these early testing results are by no means a definitive outcome.

Assuming even a miserly $25/bbl netback there are rich rewards. $25 is conservative considering these are brownfield targets with existing infrastructure, where low marginal field tax rates exist and an extremely supportive government and oil ministry are keen to see onshore production to make up for declines in offshore production.

Based on the prospective million barrels (mmbbls) at the net to CRCL share we are looking at $200m (£160m) of prospective earnings for Corcel solely based on historic levels of resource (assuming these are 100% recoverable). Angola offers a further throw of the dice but once again it’s not clear how further work is funded.

£160m over 15 years would exceed £10m EBITDA per annum.

Conclusion

CRCL today is a £5.1m market cap and 3bn shares with perhaps £1m cash (and has just lent £0.4m). Could it become cash generative in 2025? Folks like Align Research appear to have doubled their £50k bet to £100k recently. A further 1bn shares at today’s 0.17p would raise £1.7m more cash in a further raise. I can’t help but feel that’s what’s going to be needed here. At 0.17p post funding that would make it a £6.8m market cap with 4bn shares.

With that £2.7m of cash less advances to Petroborn (which are steadily repaid) also affords some level of development of Angola too.

With that additional cash there’s a reasonable chance it can build a £5m turnover which less £1.4m admin costs and tax is a £2.7m net profit business. That puts CRCL on a v.cheap P/E of 2.5X. (£2.7m/£6.8m). If it can get to a net profit, and particularly to be cash generative, its runway after that could drive this to multiples of today’s share price.

The question is what do you describe as “reasonable chance”? It’s a highly speculative share with a dreadful past track record. Corcel had the name “Corcel” above the door but were different leaders and different assets to today. In different jurisdictions. Both Angola and Brazil offer supportive regimes.

Consider the Brazil gas assets are already producing (and proven), the Angolan oil assets need to be understood but tap them in the right place and they could be producing (again) too. There is a new management team in place all with blue chip backgrounds at Shell, Halliburton, Chevron and Weatherford. Morever the CEO is already involved in an 800 person Brazilian O&G services firm Conterp. The CEO and CCO have bought CRCL shares recently too.

Should this be a 2025 idea? It’s an intriguing thought but I am going to resist.

One for a speculative punt only.

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"