Bushveld - SPR - A Specially Pleasing Result?

Bushveld - SPR - A Specially Pleasing Result?

Or a Spiteful Plundering Result?

Is this a desperate deal “just to keep the lights on” and “flogging off the family silver” as some people believe? Or is this a smart deal? Let’s examine the facts.

This evening our market cap is £35m (up £5m from my prior post). I wrote previously in my 5 drivers to value about intangibles and surely they were worth something? Turns out they are :)

'#1 “The proposed disposal of a 50% interest is estimated to result in a book value loss of US$9.8 million.”

#2 “The proposed disposal of the Company's interest in Mokopane is estimated to result in a book value loss of US$49.8 million”

Scary numbers. Yet another disasterous deal…… or is it?

Hang on.

For a start it really only owns 57.6% not 64% because Mining Charter III regulations for Mokopane means a transfer of 5% of the equity to the Bakenberg community and 5% to an Employee Share Ownership Scheme in time.

We know that the Coal Mine (Imaloto - well if you are, then you shouldn’t be in the book at zero price, then) has a DFS and just needs an FID. Yet it is in the books at $0.

What about the Brits?

No, not the Brits. Brits. The 2nd mine. Both Brits and Mokopane combined were valued at $53.5m in the 2022 accounts after the Coal was written off to zero. So Brits is now worth not a lot-o either. Zero to be exact.

Zero when BMN’s Vanadium reserves are/were 547MT and selling Mokopane (298MT) leaves 66.8MT at Brits and 172.2MT at Vametco. Brits is on the edge of the Vametco mine - a mining extension.

Mokopane meanwhile needs a DFS, needs a FID or a business who can make all that investment themselves. BMN was sat on a wonderful resource which wasn’t going to generate a Rand of income for many years to come.

Does that sound like selling unused family silver that needs expensive restoration, and then putting the rest of the family silver under the floor boards?

“Sometimes the value isn’t in what you sell it for, it’s the extent it solves your problem.”

What has been BMN’s problem?

Cash? Yeah - but isn’t that the symptom? So what’s been the problem? The answer I’ve felt for a while is Vanchem.

Higher cost, ok a more flexible range of outputs, but hungry for capital, and subject to load shedding. Dragging things down. In result after result I’ve quietly thought if the business only had Vametco we’d been profitably doing nicely. Others have said the same.

So today’s news to sell 50% to an interested party could be great news. What’s more, Vanchem gets the much needed investment (albeit the $7-$10m announcement for Kiln 1 I find strange because the estimated refurbishment cost is $37m, and as 50% owner SPR, you’ll be coughing up more than $7-10m). But there might be reasons why however much it is it is worth doing.

But is Vanchem a symptom too? Crucially, the problem withVanchem has been input. Mokopane is only 200km away and contains rich ore. That’s great news for Vanchem…. in the future.

I think you need to consider how much of a synergy the slag from the Highveld Steel works feeding into Vanchem could be worth. According to this source - potentially concentrations of 25% - compared to 1.8% at Mokopane, and less from its current 3rd party sources. If you’re sceptical, it’s there in the RNS read it again “significant synergistic benefits” and “Bushveld would share in the benefit of such optimisation.”

As they’re wont to say in Dragon’s Den, 50% of something is better than 100% of nothing.

Let’s not forget that the 4 phases of expansion from 3,841 to 8,000 mt V pa. One of the measures was to improve the feed quality to Vanchem. That was estimated at $33m. So on top of what we receive we also have avoided that cost. Also half of Kiln 1 will be paid for. That just leaves Kiln 2 and then expanding Vametco’s single kiln to get to 8,000. It’s not just about the volume it’s also about the price per tonne. Fixed costs means the per tonne cost drops. Easier to achieve 8000 with 2 businesses than 1.

Getting to 8000 any time soon seemed an impossibility - yet at a stroke it’s now within reach. What is that worth reader?

(Hint: BNP Paribus estimates the vaue of each of the 4 phases at around 11p/share)

Plus by my estimates we appear to be 15% diluted. $4.5m + $12.5m @ 6p is 283.3m shares on top of 1.56bn.

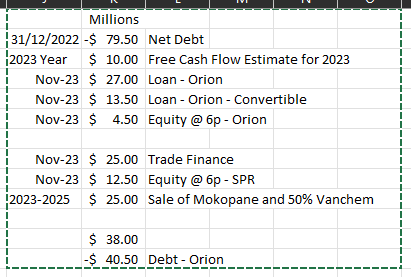

And importantly nearly (net) debt free.

Here’s my calculations - appreciate there is November 2023’s closure of the Orion and SPR deals. There’s the H1 results where we will know whether the net debt and FCF is on track (or not). So while there might be a bit of variance fundamentally the news is nearly net debt free… in 2023.

So let’s take stock.

So today’s market price £35m buys you 74% of Vametco and 50% of Vanchem Plants, 74% of the Vametco Vanadium mine, 100% of Brits, 40% of a Electrolyser Plant valued at £8m (book), 29% of Enerox valued at £7m (m-2-m) or potentially £58m PE20 FY2025, a coal mine worth Imalato minus less than £2m of o/s debt once Orion/SPR close - or zero net debt fairly early in 2024.

Does this deal sell the family silver? Plenty of Silverware left, and safer, plus shinier by my estimation. The fact people thought they’d sold the family silver exposes a lack of understanding of BMN’s assets in the first place. I believe, reader, the paper loss hides an obvious profit, and removes risk. Removes the problem. That’s because:

“Sometimes the value isn’t in what you sell it for, it’s the extent it solves your problem.”

Final thought: Was it both Pleasing and Plundering?

Mokopane was admittedly sold at hugely below its true value. The Pre-Feasibility Study (PFS) results estimated a pre-tax NPV9% of US$418.0m and a pre-tax IRR of 24.8% using a conservative long-term US$:ZAR12.75 exchange rate and a real vanadium price of US$7.50/lb (US$16.53/kg) for V2O5 flakes at >98 %

Note the FX and discount rate more or less cancel the higher current vanadium price - but IRR of 24.8% and NPV of $418m…. and that doesn’t include the Iron and Titanium! (Those being the “PQ asset” in BMN’s intangibles)

SPR should be very happy bunnies - like Orion - they’ve got sprinkles and have scooped out a large mouthful of our Sundae…. but we still get to enjoy the Sundae too, and having a cash-rich partner (about to get much richer thanks for us) and through their vanadium slag from Highveld SPR gives us a strong ally, to share costs and contribute ore which is to our benefit.

The shareholders are the bag holders here. Fortune M. sprinkled stardust around and his sweat words and honest appearance intoxicated many investors. Myself included. Everything was based on "hopium". As it is normal in the West, the new money wins over old money. Given the fact that SA is a very corrupt country, the new CEO probably 'old friends' with SPR and the lack of hard earn out facts (apart from a lame future 'slack' delivery) and a devastating dilution (this year), there will be only a very small chance for a serious SP recovery. Orion will add insult to injury and lower their conversion price to 0,025-0,03GBP instead of the 0,06. Why should they bail out useless old shareholders? Based on the closing stock price from 9/12/23 I guess the maximum achievable performance will be some 50%. Not bad for a new investor, sad for the bag holders.

Let us wait for the official reaction of the CEO. Maybe he'll be able to sweat mouth every worry away in a FM style...