SUP-ple work!

Supreme's blockbuster H1 FY2024 results

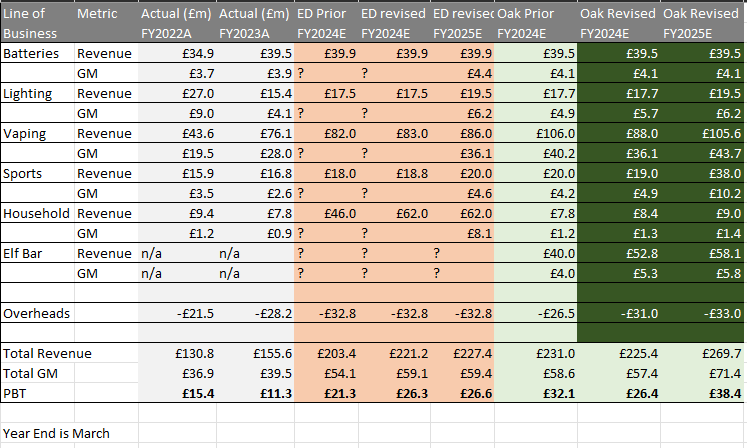

My Oak bloke forecast proves fairly spot on, apart from my use of “adjusted Overheads” (aka some overheads) and not the more accurate ALL Overheads in my estimate making!

Supreme reported growth across all categories and the results show some remarkable progress - beyond expectations in some areas.

Batteries were a solid performer, albeit there is a 2nd half weighting due to timing.

Lighting has improved margins which is great to see. Margins have returned to 2022 levels, and the logistics costs increased in FY2023 now appear a blip.

Vaping hasn’t increased as fast as the H2 FY2023 suggested (75%), and grew by 10% so I’ve tempered my expectations here for FY2024 and FY2025.

Sports, like Lighting, saw increasing margins. While it’s unlikely any new acquisition will appear in FY24 it is my belief this is coming and we will see a boost in FY25. Further penetration of Millions & Millions and Sealions could drive this.

Household has outperformed too and helps open doors.

Finally Elf Bar its managed Vape categories has overperformed too.

This is Supreme’s latest investor presentation:

Valuation Thoughts/upsides:

Ark - ability to scale revenue to £350m-£450m from the new facility with little additional overhead. This is why I’m assuming +7% overhead in FY25 on a +25% forecast profit lift.

The integrated nature of the business. Synergies can be generated by tacking parts on to the eco-system.

Master Product Agreement. The exciting idea here is that Supreme for the UK, is a bit like Samarkand is for China. In other words, an EU based consumer goods business who wishes to tackle the UK market could tap into Supreme’s footprint. This is another reason why I belive “Sports” will grow in FY25. Think about replicating Elf Bar but for Sports…. it’s a new ‘ealf’ Bar…. let’s say a Keto friendly Health Bar made in France who want to tap into the UK. What is that worth?

Smart - the moves to get ahead of legislation with Vaping is very sensible. The moral high ground. What is that sort of wisdom worth? If Supreme were part of Warren Buffett’s empire not doing something that would bring disrepute to the firm is the 1st and only rule of Berkshire Hathaway.

Overseas. Interesting to see ex-Europe sales quadrupled from £0.25m to £1m year on year.

Diluted adjusted EPS year on year also up 75% (4.3p to 7.7p a share) puts Supreme on a PE of 15.

Pod System for Vaping. I don’t think the value of this should be underestimated. If (when?) disposable Vapes are banned this will prove a boon for Supreme. It’s not released the pod system pending guidance from government.

When you strip out the “one off” effects in cash flow the business is generating over £24m a year of Free Cash Flow. Combined with a RCF of £35m there’s £60m of “fire power” for an acquisition.

Conclusion:

I see others have set a target price of 225p. That’s 80% upside from today. On today’s £145.5m market cap that’s a £261.9m market cap.

However if I’m right about the growing profitability and based on the FY25 estimate of £38.4m puts the company on a forecast 6.8 times PE. (£261.9/38.4)

Too low!

Based on the forecast FY24 earnings this is £261.9m / £26.4m which is a PE of 10.

Too low!

A PE of 15-20 times feels about right so target price 337p not 225p seems right to me.

This article is not advice. My advice is to get advice if you need advice.

Have a good evening

OAK

Thank you for sharing your thoughts and insights, Supreme is an investment oportunity which you do not stumble over too often. Theirs is anFMCG business which is easy do understand ,and they participate in at least two categories which present attractive growth opportunities. I agree with you that the price target set by ED is too low , i even think they might exceed their latest increased guidance. The Cfo in the investor presentation sounded very confident that these number were achievable .The business is highly cash generative and the higher interest environment will reveal weaker competitors /brands as future takeover targets..whats not to like...

Cracking numbers. Vaping legislation is a cloud that will drift off in the medium term and company appears to be really well placed to capitalise on distribution opportunities