Tech sea for TEKMAR

Can Tekmar Group plc TGP its price?

Dear reader,

A £7.5m market cap. A £50m 2025 pipeline, a £400m post 2025 future pipeline and a current “strong” order book. FY25 results to the 30th September 2025 are pending. Is Tekmar, ticker TGP, at a deep disconnect? Let’s find out.

It would be ironic after all, for a company which is all about connections to have a deep disconnect, although the deep bit would be fitting.

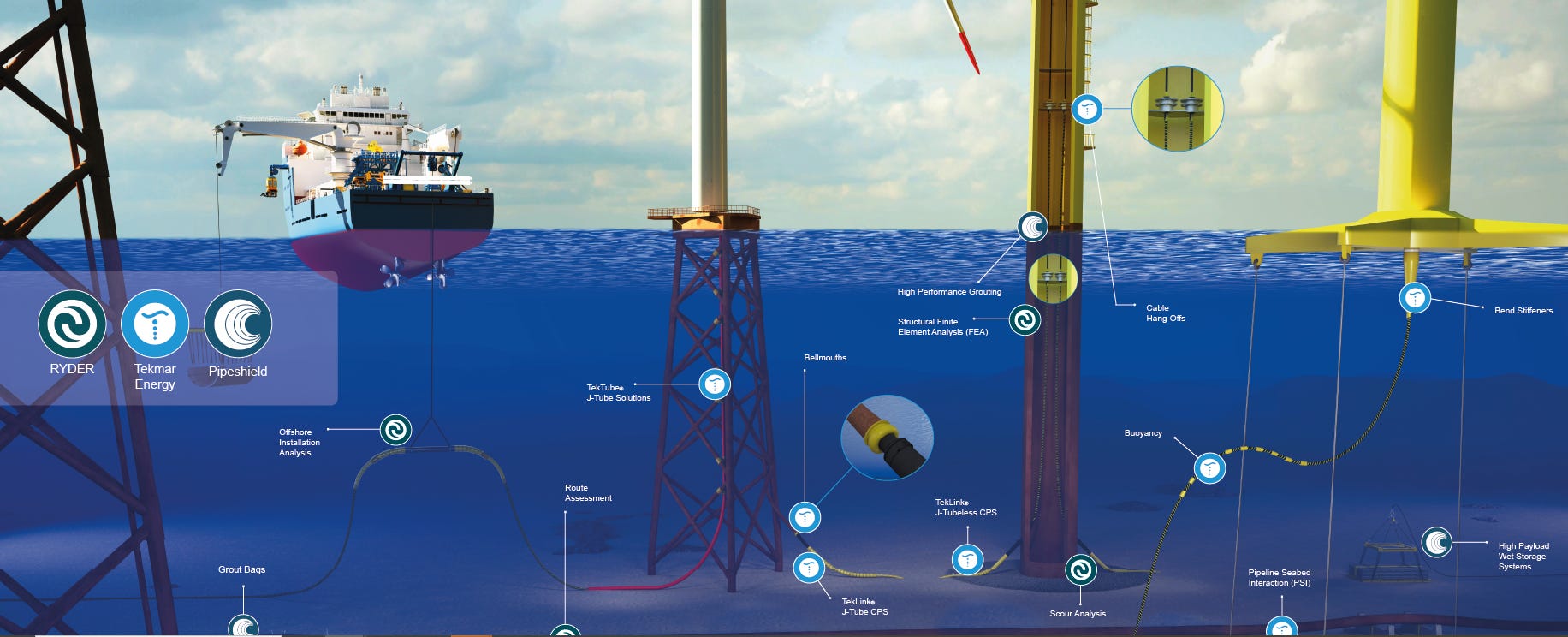

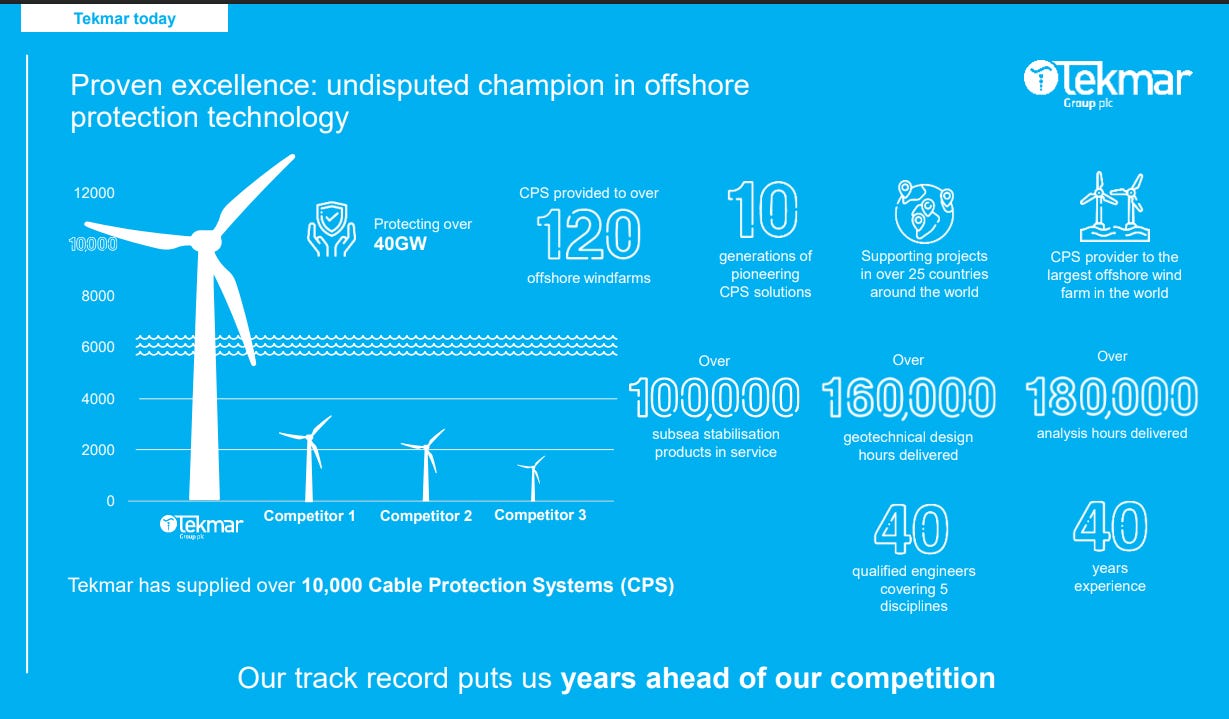

Because fitting is what TGP does under the sea: Undersea protection for fixtures and fittings for offshore Wind, Telecoms, Interconnectors and Marine Civils. This picture explains:

Global reach: This £7.5m market cap somehow runs a global span of 11 offices and 10 representatives across the globe employing 133 people costing £13.2m in wages in FY24. Tekmar describe its position in FY25, going into FY26 as having 70% spare capacity but that £1m of savings have been made. Will those stats be enough for a turnaround?

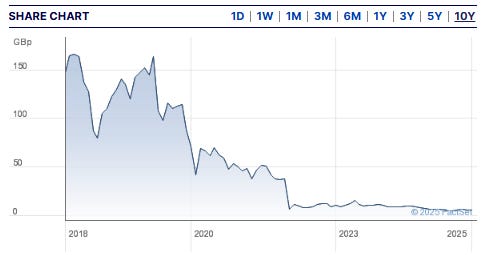

I say turnaround because a shareholder who bought 7 years ago has lost 97% of their money. Mega ouch. Is today’s 5.5p a share a bargain or a value trap?

Consider that Global Offshore Wind is growing. Fast. But also the build out of subsea interconnectors is growing and even the build out of subsea oil and gas pipelines is growing. Even after Trump’s US attempts at cancellations (one is overturned by a US Judge this morning) of those apparently “cancer-causing Windmills” that are “driving the whales loco, it’s driving them crazy”. ROFL. As Patchface the clown might say “under the sea, the whales are loco and I know oh-oh-oh.”. No one else knows this. Only Patchface….. and President Trump.

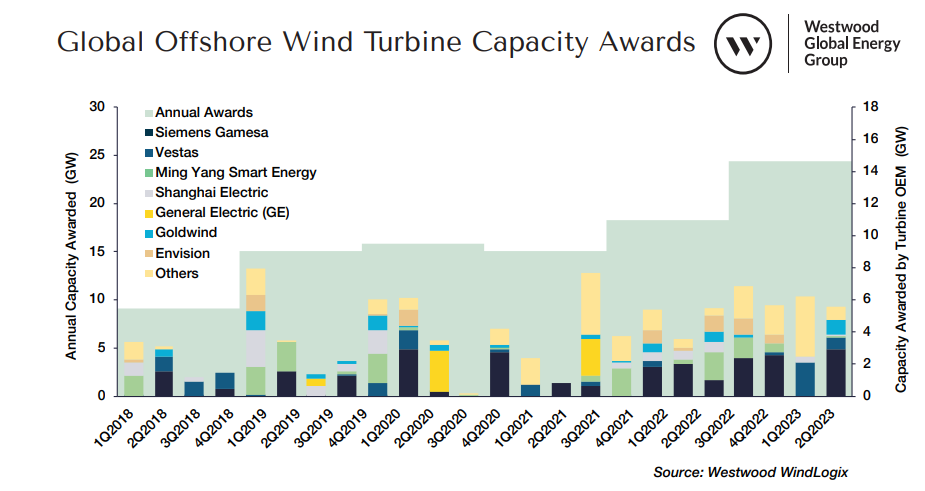

Meanwhile in the real world, offshore awards have grown in the 2020s relative to the 2010s thanks to Ed Milli in the UK but despite inflation, covid and supply chain crisis with awards exceeding 14GW in 2023 but with periods of disruption in 2020 and 2021. The knock on effect of that disruption was in the 2023 and 2024 financials.

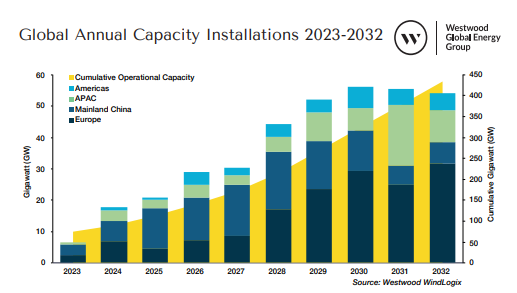

The 2023 award, meanwhile, is completely dwarfed compared with the outlook for 2026 and beyond. Of course this forecast isn’t nailed on but the need for energy is certain.

Covid reared its head for Tekmar in the aftermath and explain the dramatic fall in revenue - a knock on impact in 2020-2022 that fed through to declining revenues in 2023 and 2024, even while the pipeline rebuilt post covid and slammed into disrupted supply.

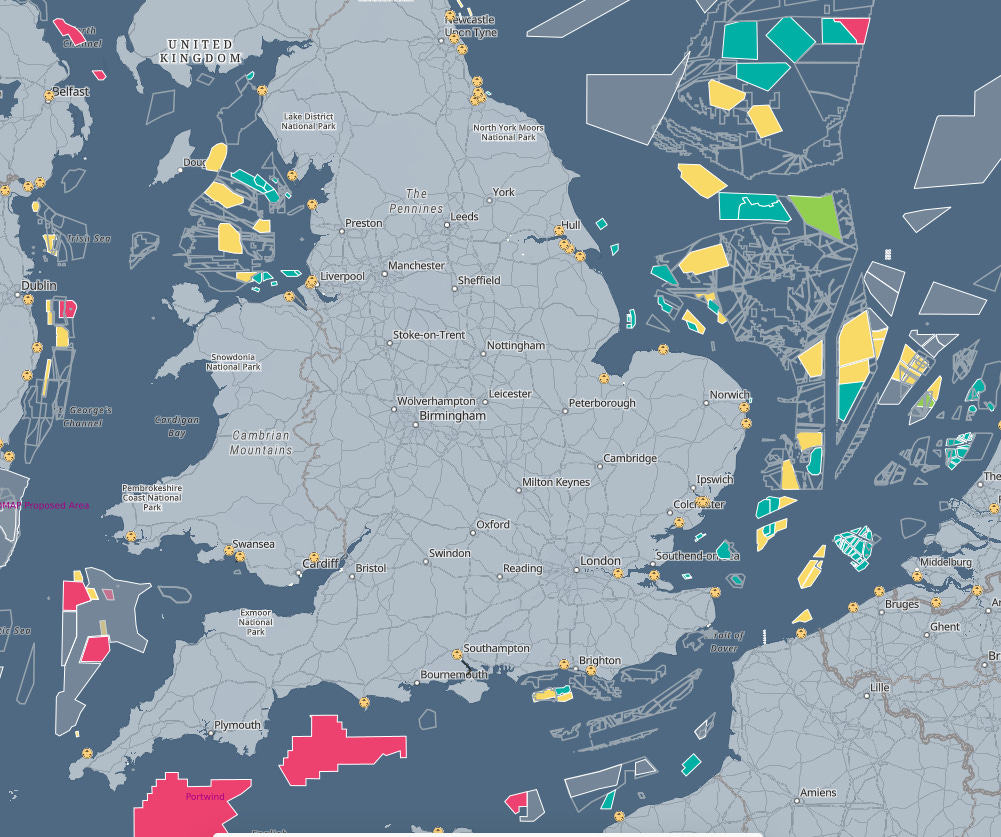

This UK wind map is part of a global map, where green is live and red/yellow is in construction/planning gives an idea of the vastness of future work. The UK is a “mature” territory yet has vast tracts of wind farms under construction. Boris promised we would be a Wind Superpower in the 2030s. He wasn’t wrong, it appears.

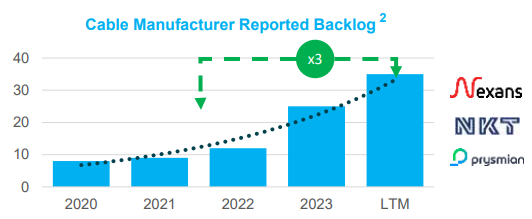

Consider the large Cable manufacturers, some of TGP’s customers and their reported order books (and profitability). Vast and growing backlogs.

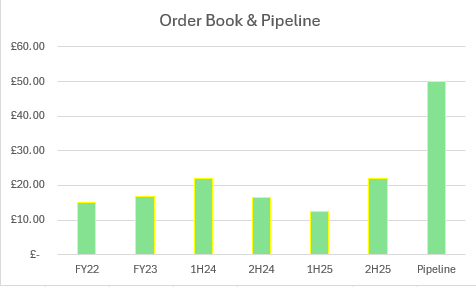

TGP suffered from a lack of order book. A telling statistic was that in FY24 there was 70% spare capacity.

If we consider that a £50m+ pipeline exists and that “strong” equals the previous best order book of £21.9m then £58.8m is over 400% of the position in 1H25. Mere months before. Is all that £50m in the bag? No. But it is a substantial improvement to affairs.

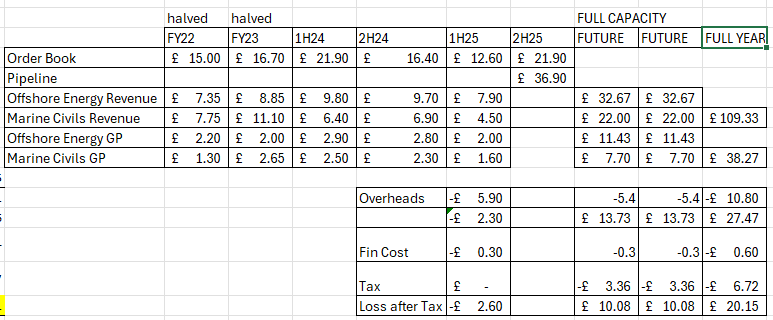

What does capacity look like?

If we, for a moment, can assume infinite demand and furthermore assume 35% gross margin and thirdly assume that Overheads are reducing by £1m per year then we get to a net profit of £20m.

Wait, what?

£20m net profit at even 10X earnings gets you to a £200m valuation. Such a lofty valuation would be 26X today’s £7.5m market cap.

However it’s not that simple.

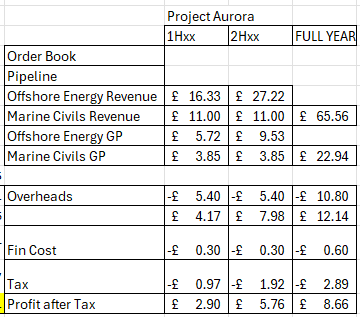

We don’t have infinite demand, and perfect supply of capacity and even Tekmar themselves don’t claim that they can achieve £109m revenue in the next few years. But they do claim they can double revenue in that time. Their plan to do so is called Project Aurora. This would be achieved through a mixture of product development, market growth, growing market share and acquisitions.

That doubling of revenue, assuming the same 35% gross margin and overheads equal to those of today implies a FY2028 P/E of below 0.9X today’s share price. Even if there is some slippage on margin and/or cost growth there appears a strong margin of safety.

What about competition?

When it comes to Cable Protection Tekmar has supplied 5X the volume of its next largest competitor. Stockholm-listed Trelleborg is said to be one competitor but its website is a morass of medical, automotive and aerospace where subsea is barely mentioned.

Legacy TGP issues

Legacy contracts were lower margin and these are now largely complete and in the rear-view mirror. There was also a legacy warranty issue relating to abrasion claims by a customer. TGP explain that they have worked with the customer to achieve a positive outcome for them and TGP’s own insurance has largely offset the claim amount. Again, this is now settled and in TGP’s favour - Tekmar products were not to blame. While the market looked at this as a potential negative TGP saw it as a learning experience and a positive.

There was also a legacy project where the Chinese customer got into a bad debt situation (presumably caught up in the China housing crisis) which again has agreed a payment plan to pay its overdue £2.1m balance by 31/12/25.

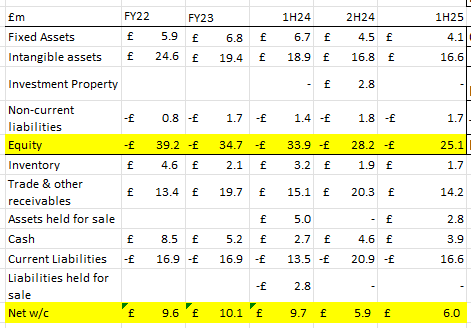

TGP Debt

Net working capital is £6m (as at last results) if you are happy to include an asset held for sale, or £3.2m if not. Ignoring inventory that number is £1.5m. Overdue receivables are a problem but reflects dealing with large customers. One overdue balance is being cleared and the business has £6m headroom in borrowing facilities and a £0.45m lease liability.

Conclusion

A 40 year old company with an enviable client list, a growing market, and leadership in offshore asset protection. A focus on margin, tight cost control and leaning into the growth via electrification are all reasons why TGP offers a unique opportunity to profit from a bombed out company on the cusp of a rebound - focused by Project Aurora.

There are 14,000 Wind Turbines across the world and Tekmar has supplied the CPS for over 2/3rds.

So this is not just an offshore wind story either. It is the marine civils that support offshore. It is interconnectors supporting electrification and the fact that the wind is always blowing somewhere and the sun never sets on the British Empire (or what was), but also the growing business of offshore O&G.

The other point to make here is the rapidly growing potential value of a growing base of assets which require maintenance, improvement, end-of-life services - some of which will be recurring revenue. None of that opportunity is priced in to this company either.

Tekmar supplies vital products and services to all of these growing sectors - and is a leader too - but not priced as such.

Regards

The Oak Bloke.

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

"a shareholder who bought 7 years ago has lost 97% of their money."

That would be me, more or less. Bought 26/11/21 for 48.5p. Down 88%. Gonna be a while before I break even I think!

Excellent 👍🏼