THAR-is-a better future

THS 3Q25 results from the platinum miner and OB25 for 25 idea

Dear reader

Chrome and PGM miner Tharisa reported its 3Q25 results (ending 30/6/25). We see growth in PGM and Chrome compared with the 1H25 results although not enough to get much above the lower band of the FY25 forecast volumes.

THS meanwhile dropped their volume guidance by 5% even though they appear to be on track to overachieve that new lower limit by 5%. Better safe than sorry.

Harrumphers sold on the news of a 5% drop to guidance. Stocko was silent. And the OB eagerly added more THS. Why?

Volume is part of the equation to profits, to be sure, but what about price? The results gave the happy news that the 3Q25 basket was $1,574 so over $500 per PGM ounce of additional profit dropping to the bottom line vs FY2024.

The news gets better still. Based on prices today 14th July, a THS PGM basket is now $1,800 per ounce, if you believe Ru and Ir remain unmoved, more on that later. The equally important news is that the price rises favour Karo and the basket difference is only 6% (and likely Karo’s basket is above $1800 once you factor in Copper/Nickel credits). Of course Karo is a theoretical basket since it is a project under evaluation and seeking funding. THS are progressing it on a go slow basis.

Assuming that this $1,800 basket is the average in 4Q25 (to 30th September) that calculates to an FY2025 average basket revenue of $1545 per ounce, and a $1,688/ounce 2H25 average. A $1688 PGM/ounce average alongside an average $265 chrome/tonne price gets you to above $90m

In other words the 2H25 profit will exceed both the FY23 and FY24 full year profits. Profits double but the share drops. No wonder I added!

If $1,800 is also the PGM basket price for FY26, and we see an average $270 Chome, with 160KOz PGMs and 1.8Mt Chrome (i.e. the FY25 upper target volume) then we see profits forecast of £124m.

The THS market cap today is £254m and it was £228m post-harrumph after dropping on the 3Q25 news. No wonder I added!

The THS NAV at last results was $697m or £516.3m vs £254m is a 50.8% discount to NAV. No wonder I added!

Ruthenium and Iridium

Estimates vary for Ruthenium and Iridium and these aren’t publicly traded. We know both are currently in deep deficit (refer to the Johnson Matthey PGM report 2024). If the rumours are true (and there’s every reason to think so) then the 1/3rd increase of each PGM metal drives the actual PGM basket at Tharisa mine to be $1,859/ounce not $1,800 today.

Cash Rich

I did spot the Cash had dropped by quite a bit for THS in 3Q25. I put it down to investing in Karo but an update clarified that Cash was $164.6m and debt was -$121.5m so THS has US$43.1m in net cash.

Sylvanian Families

SLP generates 80Koz vs 160Koz at THS. What if THS get Karo producing? Let’s not even go there. SLP has increased by 63% in 2025. THS 35%.

SLP is getting on the chrome game. 0.0325MT in FY26 and 0.2Mt in FY27 (attributable) is dwarfed by THS’ 1.65Mt and longer track record. Besides THS is a refiner of Metallurgical Chrome, a transporter of Chrome and a purveyor of Iron-Chromium Batteries (BESS).

Edison and Panmure put SLP FY26 profits at $27m implying a P/E of 8.4X. Perhaps those broker guesses are now out of date, or just plain wrong. Perhaps SLP is on a tear and might achieve more than $27m in FY26. But how much more? 4.2X more? Compared with a forecast earnings of just 2X at THS, no wonder I bought!

Karo

Of course Karo’s basket at $1,720/ounce is getting VERY interesting. THS (who holds 65.59% of Karo) have been progressing Karo on a go slow for a few years, although studies, infrastructure and optimisations continue. What will the THS share price do if they announce an off take or funding for Karo?

After all Karo is a Tier 1 low-cost, open-pit PGM and Chrome asset located on the Great Dyke in Zimbabwe capable of 174 koz/year for 11 years LoM and NPV10 of $494m based on a $1,600 basket price. Karo would more than double Tharisa’s PGMs and take Tharisa above $1bn revenue a year. The capital cost is $391m and $154.8m has so far been committed and $98.1m spent with spending slowed while debt capital is considered.

The combined resource size for Tharisa Mine and Karo comes to 1 billion tonnes containing 52 Moz of 6E PGMs. Tharisa Mine has a potential 40yr life, of which the first 18 will be open pit, with a 20 year underground option. The I&I of Karo is 10Moz of 6E PGMs. This is based on 100m depth even though the resource goes to 1000m. In fact previous estimates of Karo by Zimplats, were 96Moz of 4E PGMs (so more inc. 6E) or c.10x the resource being currently measured in the Stage 1 production plan.

Other benefits to Karo is a supportive tax regime of 15% for 10 years and ability to export (rather than sell to a government monopsony), and no BEE (black empowerment) legislation where you effectively give away a share of ownership for nothing. There are other miners in the area like Zimplats and AngloPlat so an educated and (mining) experienced workforce too.

If we consider that Zimplats is ASX listed and valued at A$1.72bn today. That’s a £840m market cap or £1.3m per Koz produced per year, or £38,250 per Koz per year remaining (i.e. a 34 year life).

Using that logic for Karo that would equate to a £735m valuation for THS based on an 85% ownership (i.e. 100 years x 226 koz x £38,250 = £865m) once built. Karo’s $391m capex less $154.8m spent leaves $236m or £176m remaining to spend implying a large upside (of £558m) if Karo were completed on a read across. Appreciating that a half-built mine is worth not as much as a completed and producing mine!

Consider too that Zimplats 2024 profit was $8.2m vs $563m in 2021. Are we going to see higher PGM prices than what exists today? 2.4 Ounces of Platinum buys 1 Ounce of Gold. What if we see parity? Platinum is more scarce than gold after all.

If PGMs boom again like in 2021, see below a Karo basket was $3,000 an ounce then the market would - or at least should - value Karo at £1.66bn - again on a read across basis on the basis the mine is in operation. Its build out and completion would require 15 months lead time, we are told. All the long lead items are complete.

Will all of these read across benefits accrue to THS? No, not 100% of them. The idea is to finance via debt and project finance, and potentially via an offtake and a strategic investment. This slide explains the progress made in finalising a deal for Karo. Some aspects are in advanced talks or are “progressing” but have taken a lot of time.

It is my sense that news will break in 2025 on Karo. It’s too large a prize to be ignored.

Conclusion

There’s lots to like at THS at £254m market cap. There was even more to like at £228m.

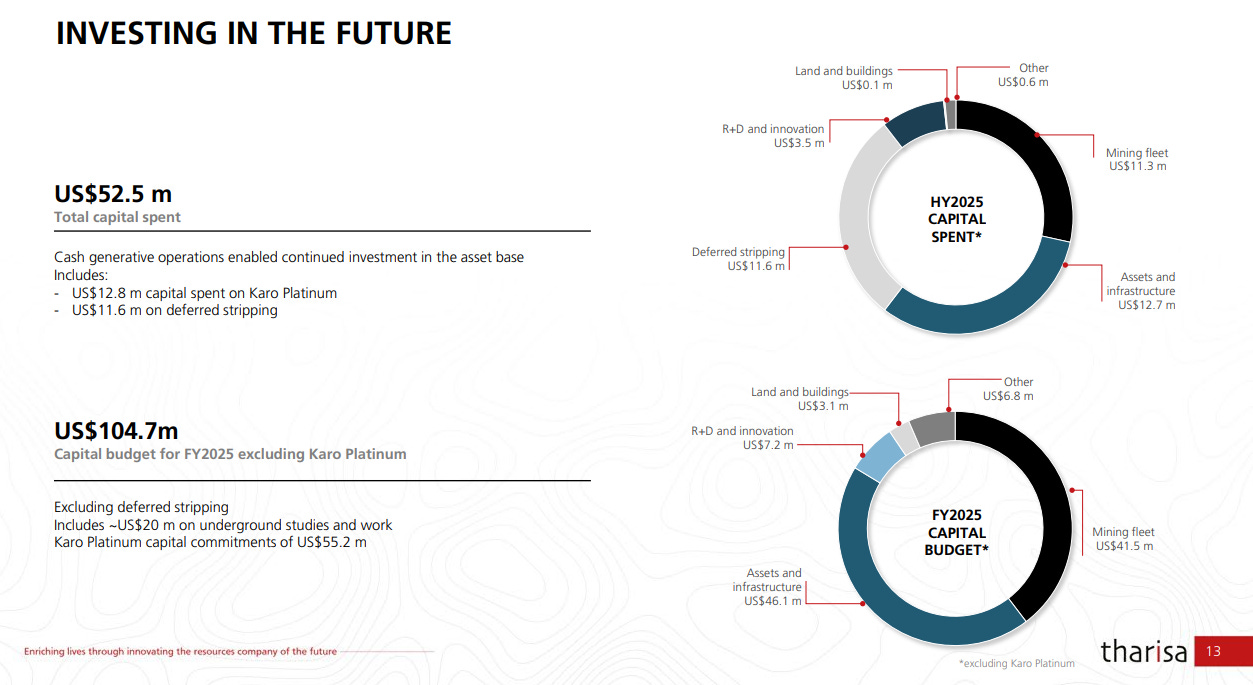

The 3Q25 results weren’t spectacular in volume terms but I’m relaxed that they can get to a decent full year result and that improvement to volume is coming $104.7m of capex spend (excluding Karo) makes me think so.

My analysis suggests FY26 is looking spectacular. With further upsides from Karo, from its various Chrome-related businesses, and the relaunch of the buy back programme.

Regards

The Oak Bloke

Disclaimers:

This is not advice, you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"