The BELL tolls

Dear reader

Q2 begins with news of delays at Belluscura.

Rather than a start of Q2 commercialisation we are now looking at end of Q2 with “full commercialisation” in Q3. We are further told that revenue and adj.EBITDA will be lower than Dowgate’s forecast:

Going with the lowest numbers to achieve $16m revenue in 2024 AND an EBITDA loss of $1.5m the sales must look something like this:

The consequential cash flow needs to lead to a -$1.5m adj EBITDA loss in 2024, plus we know cash as at 31/3/24 is $3m

So cash flow must look something like this.

The consequence of the news is that a further funds will also be required for commercialisation. It appears “a line of credit” is being discussed so we also await what dilution (if any) this will mean. The items highlighted above in red are the unknowns.

It is my understanding that Innomax would fund its own manufacturing operation, and would carry its own stock of raw materials, paying not only a royalty but also a profit share on consumables too. If that’s the case, then does BELL need to fund anything? The jury is out on that one, but if your partner is manufacturing something then you get a royalty and a profit share but you let them make it and sell it.

In more bad news, it would appear there will be inventory write offs too, making FY23 a stinker. The extent of this remains to be seen.

A key reason why I believe today’s sell off is overdone?

Why would the TMTA Directors have agreed the reverse takeover knowing the delay was going to happen? Because they would have known. There is absolutely no way that they would not have done due diligence and had full visibility of the books, the commercial progress… everything.

And because they knew, that gives me hope. They hold 3.4m of BELL’s 165m shares, which was worth about £0.6m when they did the deal (worth just £0.27m today)

It is fairly obviously that your £0.6m is going to be severely affected on today’s announcement - which they knew was coming. So in my opinion there already has to be a plan. I expect the Directors and large shareholders have already agreed terms for this “line of credit” - if it’s BELL’s responsibility rather than Innomax’s.

The TMTA people must also know that this blip is just that - a blip. That their £0.6m has a reasonable - if not better - chance to returning to £0.6m and to grow from there. Otherwise why the heck would they have agreed?

I’ve used my previous estimates for commercialisation of $8m and working capital of $3m therefore the fundraise is potentially $12m, but at this stage the numbers are unknown, and there would also appear to be a degree of optionality - for example a higher level of working capital enables a more rapid scale up.

In order to achieve an EBITDA loss of up to $1.5m the scale up, margin and overheads must be approximately along the lines of my model.

What I find encouraging, amidst a pretty discouraging RNS, is the fact that the run rate which even a “$1.5m loss” in 2024 establishes, along with growing royalties, an operating cashflow positive position Q1 25.

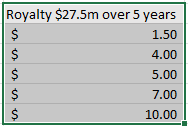

Royalties in 2025 provide a further boost ($4m):

Nothing’s changed - in terms of the opportunity

Overall 10,000 backlog of orders worth $30m

5 year royalty deal worth $27.5m - extendable to 10 years (+$27.5m)

Manufacturing by the folks who make iPhones (FoxConn owns Innomax)

125 distributors - some who ONLY want to sell BELL

Centers for Medicare and Medicaid Services ("CMS") codes making the device significantly more profitable for US Durable Medical Equipment providers

Key global distributor McKesson on board - 3rd largest in the USA

Approvals for the USA, Hong Kong, Singapore, China

Silver Award Winning at the US Home Medical Equipment Trade Show

This is a $34bn/year Oxygen Therapy market

A higher $3000 price point for Discov-R

A lower (estimated) $1,100 cost of sale for Discov-R

Previously estimated 18.46p NAV per share, putting today’s share price at 50% discount to NAV (the 18.46p will have reduced due to cash burn FY24 and the indicated Inventory write off, but should be well in excess of 10p/share)

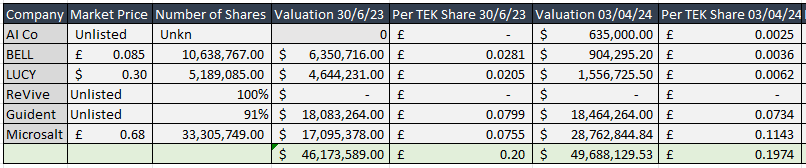

Meanwhile for TEK-kies

Some people hold BELL via holding TEK. The drop in BELL is unwelcome but it should be remembered that even at current bombed out prices the NAV is 0.26 pence less than last June (when the share price was 10.5p bid/11p ask. Today’s share price of 7.7p bid and 8.5p ask is a 57% discount to NAV - and that is assuming Guident hasn’t risen in valuation (despite its progress) and ReVive is worth zero (despite its progress), and that there’s zero cash or other assets to consider.

Conclusion

The question for BELL-ies is - what happens next?

Clarification on the line of credit is of course crucial. It’s a pity that this wasn’t clarified today.

Communication about progress on the Discov-R launch is crucial. BELL-ies should be rightly aggrieved at the lack of newsflow. An update on progress with X-plor would have been helpful too. It would appear these are being produced in both China and the US - and sold at least in the US.

But overall, does a 3 month delay make BELL worth half as much? For that to be logically the case either the risk has doubled or the return has halved.

Half seems excessive. Especially when you think of today’s news from the perspective of an ex-TMTA Director.

This is not advice

Oak