The Venture Life full year view

Considering the VLG FY24 trading statement

Dear reader,

My estimate of £55m revenue for 2024 was an overshoot of ~£3m turnover to the actual £51.8m revenue performance VLG shared in its full year trading statement.

Even so, I’m feeling pretty pleased. Why might that be?

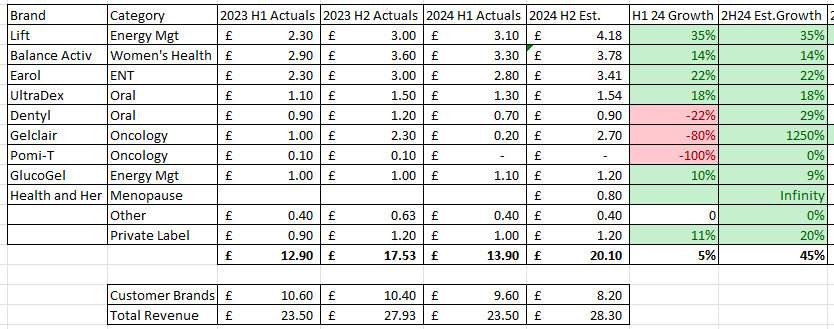

Well, the positive aspect is validation of the growth in sales of VLG brands that I foresaw. Significantly, the growth in margin also. A 45% overall margin implies a ~33% customer brands margin (up from 31%) and 50% VLG brands margin in 2H24 (up from 43%). That will be down to economies of scale, price rises, product mix, new products and formulations and other factors but the result implies an upside to 2024 net profit (vs 2023)

It’s true that the performance of its Customer Brands came in much lower than expected and totalled £17.8m revenue in 2024 - which means £9.6m in 1H24 dropped to just £8.2m in 2H24 - about 20% lower than 2023 due to customer destocking we are told.

But then we consider what must have been around a 45% growth in sales in VLG brands from 1H to 2H. Comparing 2023 to 2024 then we see a 9% growth instead from year to year.

We also see Health & Her contribute £0.8m revenue and £0.11m EBITDA from 8th November so based on 53 days of revenue. Annualised that implies £5.5m revenue. We don’t know precisely what margin Health & Her products generate but using a 50% margin that’s £2.75m gross margin and taking the EBITDA up to 30/09/24 of £0.8m implies about £2m of overheads. On the basis that at least £1m of cost can be stripped out of those overheads, and that 33% growth can be achieved in 2025 the prior estimates look to be pretty close too. The question is whether you believe 33% growth is justifiable in FY2025 via what VLG say are an “exciting pipeline of innovations…. across many channels”.

If that is true then you should see an out turn not similar to my prior numbers where I foresaw a FY25 performance of up to £9m with a PBT of up to £2m.

This growth and synergies would mean adding £1.5m net profit in 2025. If VLG achieved absolutely nothing else that would imply a £2.5m net profit in 2025. This is qualified by VLG telling us they expect H&H to contribute “at least £1m EBITDA” suggesting that the estimate could be lower.

£2.5m net profit also implies the rest of VLG is standing still in 2025. Outside of H&H, VLG of course are not standing still. They tell us the customer brands revenue is down due to de-stocking and that that is already reversing in 2025. That new customers and initiatives in its customer brands are adding revenue in 2025. Importantly while these are lower margin sales this also has the effect of spreading fixed costs more broadly, and utilising spare capacity.

adj.EBITDA growth in 2H24 is extremely pleasing too. A £7.7m performance in 2H24 is a more than doubling from 1H24 (£3.6m) and higher than 2H23 (£7.1m) and much higher than prior years. So an £11.3m full year performance. This suggests current debt excluding leases of around £18m at the end of January 2025.

However adj.EBIT is also worth considering. 1H24 D&A was -£3.4m so full year -£6.8m leaves an adjusted EBIT of £4.5m for 2024.

Future

Even assuming fairly modest growth, far below the momentum of 2024, then you can get to a FY2025 revenue of between £65m-£70m. In my model Health & Her generates £8.8m and Custom Brands + £0.7m revenue vs FY2024. The remainder achieve gentle growth with Gelclair the notable exception due to the Jaguar US distribution deal.

Under this scenario profits ratchet upwards in FY25 and beyond. Cavendish speak to a tripling from £0.9m in FY24 to £3.2m in FY25 before ascending to £5.8m in FY26 and £8.2m in FY27.

I see a stronger net profit in FY25 of over £4.5m.

Comparing my model and theirs I see they believe margins will fall in FY25 from what was achieved in 2H24, and operating expenses will rise by nearly -£5m year to year (they claim from -£10.5m in FY24e to -£15.3m in FY25), while I see a more modest increase of -£1m (due to Health & Her expenses). These differences mean my model forecasts a £4.6m net profit out turn while theirs predicts a smaller £3.2m.

Conclusion

2024 looks to be a decent-ish result but on the face of it nothing more. But underneath the apparent 0% growth the VLG Brands 1H24 to 2H24 growth and trajectory of its investment into its brands appears to be paying off. Evidence of this momentum continuing in FY25 should cause this share to rerate - rapidly. If this momentum detected in FY24 can and does continue in 2025 and perhaps even accelerate then this share at a £51m market cap will look incredibly cheap.

To an acquirer, brands that can generate £50m and growing sales with a £25m gross margin is worth far more than a £51m price tag (i.e. today’s share price). Paying 4X-5X the gross margin seems good value. After all, by the same logic consider that Health & Her was bought by VLG based on 5X earnings in FY2025 (with further growth ahead).

5X gross margin would be £125m and 100p per share.

That valuation ignores the contract manufacturing element which generates £5m annual margin and holds zero IP. I believe it would be of much less interest to a buyer although Cavendish believe someone would pay 1.5X revenue i.e. £30.8m. Good luck selling, and I am sceptical. Although it’s a useful adjunct to the main business to contribute towards fixed costs, it probably wouldn’t fetch anything like £30m.

Meanwhile we are about 6 weeks away from the final results (which should include a post period update), and 6 months away from a summer trading update. Either of those events could be the catalyst for a rerate to ~60p or more. (£75m market cap)

Regards

The Oak Bloke.

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

What are your views on the recent CDMO divestment announcement for 53m?

With the CDMO contributing 5.0m of adjusted EBITDA, that would leave around ~$6m of adjusted EBITDA on a ~$17m enterprise value, assuming no growth from 2024 Power Brands?

What is cash conversion rate on the remaining business? Surprised to see this news has not re-rated the stock significantly higher.