The whether EZJ...... ¡Scorchio!

Considering Easyjet's 1H26 results

Dear reader, bono istente, bono istente,

EZJ delivered a strong performance in 1H26 (to 31/3/26): They lost -£377m.

Wait, what?

Is that strong? Well, winter is tough for airlines. Brr. Go back 10 years and they typically lose money in the winter and make hay when the sun err shines in summer. Y’know when it’s Scorchio! More on that later.

The Case for easyJet (EZJ): A Structural Winner Flying Under the Radar

The market loves to panic over airlines—obsessing over short-term fuel spikes, inflation data, and whether cash-strapped consumers will cut back on travel. I’ve been buying on the sell off because if you look past the macro noise and look at the actual plumbing of the business, there is a serious structural growth story continuing here. A compounding machine disguised as a volatile airline stock.

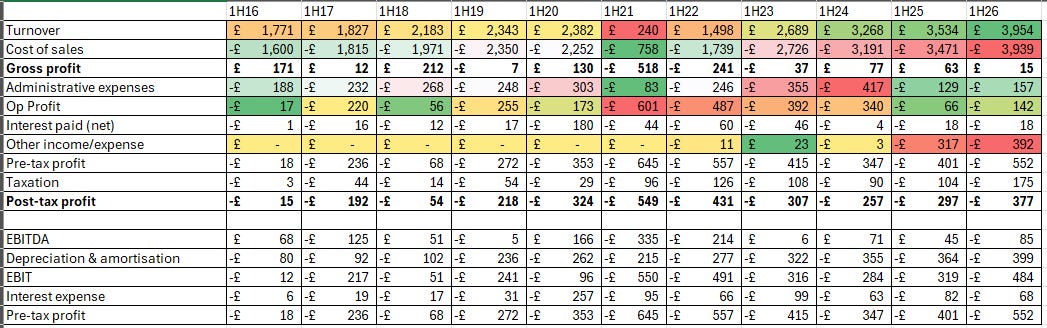

Here’s 10 years of EZJ first half results:

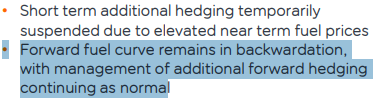

How much of that reduced profit year on year was Third Gulf War related? £25m. So 1 month of war and inflated jet fuel prices led to about 5% of the 1H losses. An interesting point was the “backwardation” they are seeing in fuel markets which means the price of jet fuel in the future is much lower and the comment that EZJ are aggressively adding Hedges 12-24 months ahead. Good to see and a smart move. That means you can offset the potential future higher cost of fuel.

EZJ report no physical shortage of jet fuel for Europe nor do they anticipate any. Increases from the US, West Africa and Europe itself have made up the middle east shortfall. Are competitors blaming fuel shortages for flight cancellations as a cover for their weakness? Seems so. Blue Leader O’Leary confirms the no fuel shortage in Europe on Squawk Box.

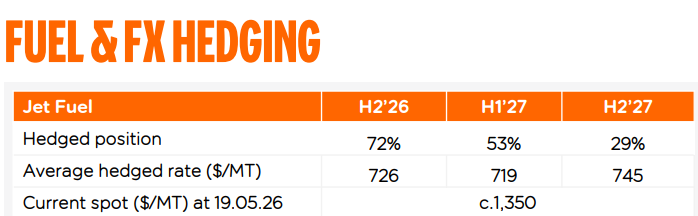

EZJ report plenty of half-price (to spot price) hedging out to September 2027 as well as £4.7 billion of liquidity and Net cash of £434m too.

Reduced profit was also due to Legal Provisions of £32m.

And expensed investment into two new Italian bases and a Moroccan one of £30m

So that’s £87m of arguably extraordinary costs pre tax and excluding those factors underlying profits were post tax around -£310m vs -£297m a year back - arguably. A modest 3% underlying difference y-o-y.

That was despite 11% crew wage inflation, and a 23% increase in overheads, which is particularly IT and marketing investments. More extraordinary cost? More on those later too.

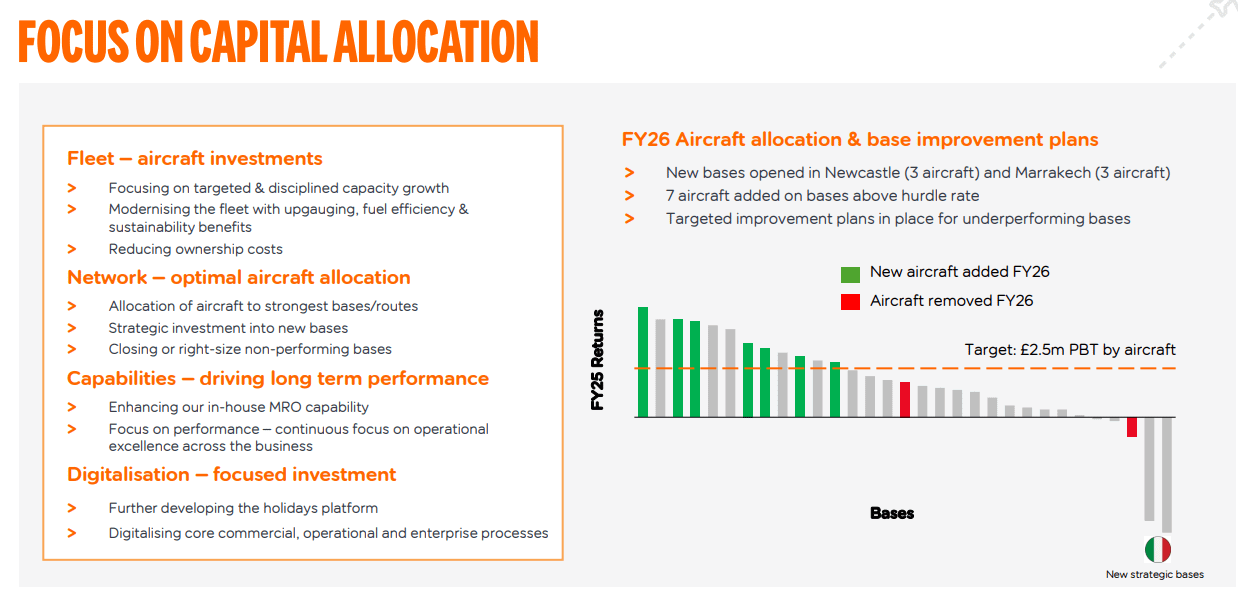

Route Maturity = Profit Harvesting

Building out an airline network is expensive, but easyJet has already done the heavy lifting. A significant portion of their newer routes are now entering the maturity phase.

When a route matures, brand loyalty locks in, marketing spend drops, and load factors stabilise. EZJ is moving out of the expensive “investment” phase of much of its network and into the highly lucrative “harvesting” phase, which is set to drive unit revenues steadily upward. New elements like in Italy are noticeable in the chart below.

As pictured above EZJ are culling specific routes and aircraft that are not performing. Retiring A319s in favour of cheaper per KM Neos. Look at the profitability building for new routes too. Will we see improved profits for EZJ as more competitors go to the wall? European flag carriers are not in a happy place in May 2026. If you watched Blue Leader’s interview he reckons several will go to the wall in 2026.

Improvement in the Airline Segment

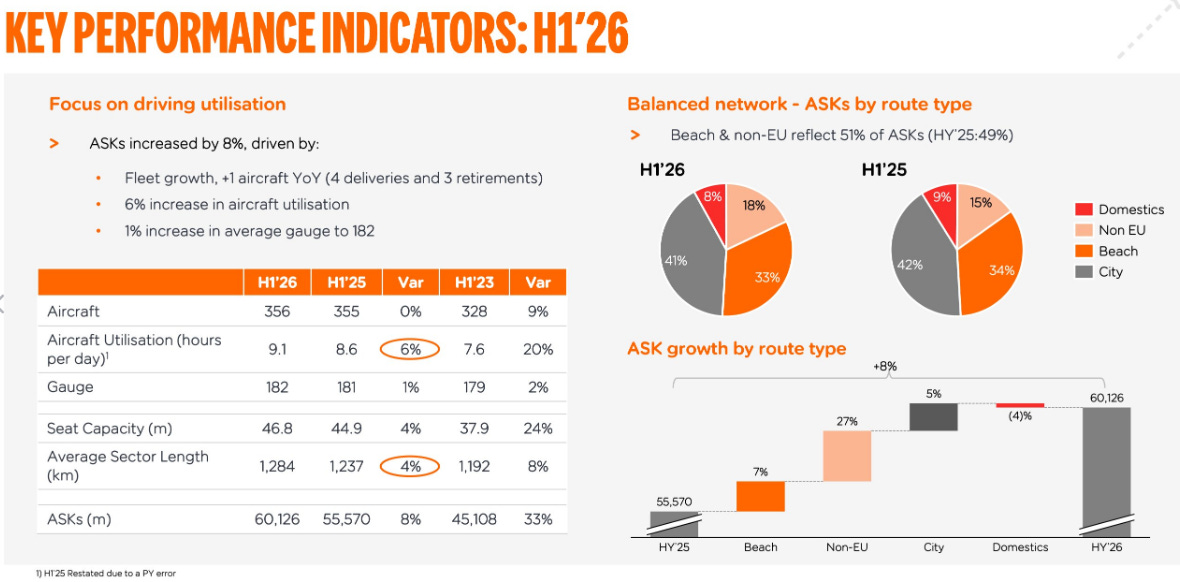

Geographic revenue growth for EZJ was impressive in 1H26: Nearly 30% revenue growth for Italy and Spain speaks to the improvements through those EZJ new bases in Milan and Rome while also achieving 10% growth for the UK.

EZJ delivered strong improvements to its own efficiency where utilisation is up 20% in three years for the winter half year. While capacity also increased by 9% over the same three years, but efficiency improvement meant seat capacity grew 24% and available seat kilometres grew by 33%.

Year on year non-EU grew substantially where Turkey, Tunisia, Morocco and Egypt particularly were part of that growth. Load factor grew nearly 2% to 89.8%. Going forwards certain destinations were stopped including Tel Aviv while some Cyprus, Egypt, Greek and Turkey flights have been modestly reduced.

Improvement in the Holiday Segment

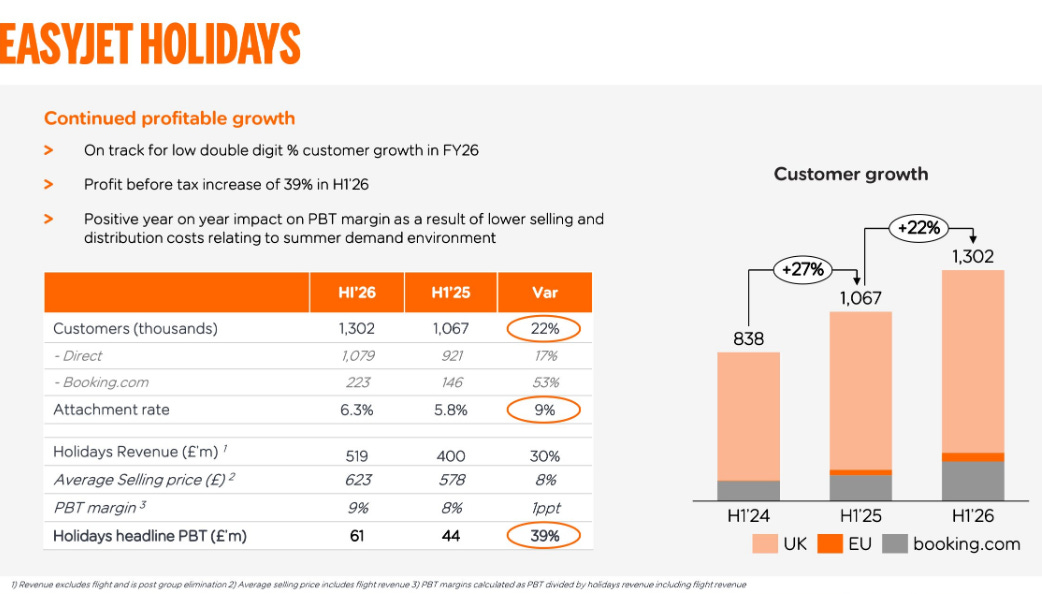

EZJ holidays revenue in 1H26 grew from £542m to £687m and over 1.3m customers flew EZJ for their Easyjet Holiday.

easyJet holidays delivered 22% more customers y-o-y and a growing number who buy a flight AND a holiday (aka the attachment rate).

Pre-tax Profits were up 39% at £61m and the margin grew to 9%.

The beauty of Easyjet holidays is that they are asset light and high margin yet come at a much lower price point than JET2. £623 average

EZJ launched of flight-plus-hotel deal to increase hotel inventory from c.8,000 to c.13,000 particularly to drive more city breaks. The EZJ app basically lets you add the hotel with a click.

But what if you don’t? Bizarrely, (least I think so) 70% of zee Germans buy their holiday via a physical Travel Agent (remember those?). Therefore EZJ is launching in 500 Hauptstraße (high street) retailers within the Berlin catchment area. Wunderbar!

EZJ delivered continuing improvements in satisfaction with customers, particularly to its Holidays customers. With a CSAT of 85% vs JET2 84.3% CSAT there’s not much - statistically speaking - between the pair except the price.

• On-time-performance 78%, +1ppt

• Airline CSAT 84%, +2ppts

• easyJet holidays CSAT 85%, +1ppt

Although Stats can be used selectively and JET2 themselves say “With customer satisfaction levels exceeding 90% and net promoter scores consistently in the mid-60s for both Jet2.com and Jet2holidays, coupled with our high customer retention rate of 59% across both brands……”

So is it 60%, 84.3%, >90% for JET2 - you decide. But the argument that JET2 offers a superior product and EZJ doesn’t? Is that true?

And at what price?

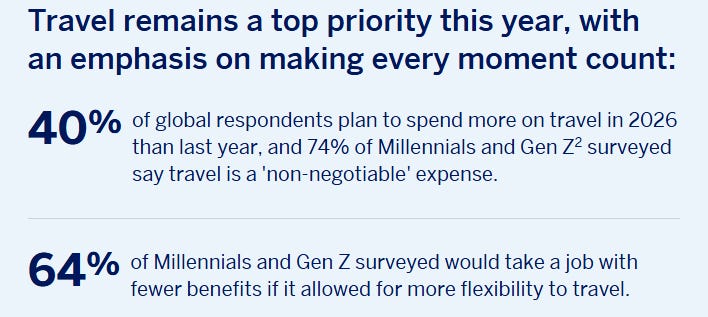

Whatever your view on this, travel remains an important priority for people, particularly for young ‘uns according to AMEX 2026 travel survey. In my prior article I spoke of how people were PRIORITISING holidays. More than that AMEX furthermore tells me it’s non-negotiable. That means DEFENSIVE.

Defensive. Not the usual thing you’d say about a cyclical airline is it? Military perhaps. Civil? Well non-negotiable means just that.

A customer who considers foregoing your product or service non-negotiable a useful place to be when faced with an extended peace negotiation between the USA and Iran both with their non-negotiable positions.

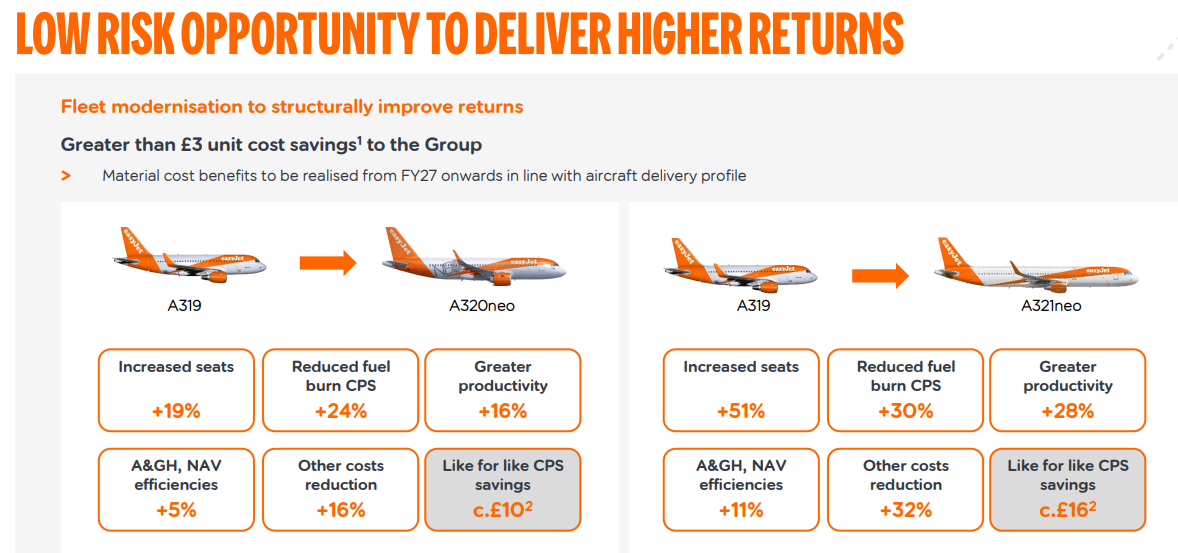

EFFICIENCY AND UPGRADING THE FLEET

New aircraft will mean £250m of savings equal to £10 to £16 cost per seat. The 1H26 equalled a -£13.09 loss per seat, so you can see how that profit boost is massive. It could make Winter profitable.

In an inflationary world, how do you beat rising costs? You scale up efficiently. easyJet is currently undergoing a massive “up-gauging” process, systematically replacing older, smaller aircraft with larger, hyper-efficient Airbus A321neo planes.

More seats per plane means the fixed costs of the pilots, fuel, and airport slots are spread over a larger number of paying passengers. This structurally drives down the unit cost per seat, giving them a massive competitive moat over smaller rivals who can’t afford to modernise, and flag carriers muddling on with their ageing A319 fleets.

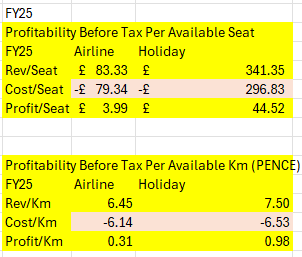

FY25 delivered an overall £3.99 profit per seat where the 2H makes up for the first half. Overall in FY25 the profit per KM flown was 31p. But for the 5.6% who were also an EZJ holiday customer that seat was not a 31p profit per KM. It was £1.29 because the holiday added 98p.

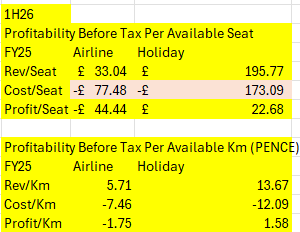

In 1H26 two things happen that make me very happy. First is the attachment rate went up from 5.6% to 6.3%. That means 15% more Airline seats were for EZJ holiday folks.

EZJ cross sold a holiday 6.3% of the time.

Second of all the profit per KM flown by a holiday person was £1.58. This did not fully offset the -£1.75 average loss per KM flown but it makes the 1H results a lot better. Winter people went on much cheaper holidays too, where £195.77 revenue is lower than the £341.35 average in FY25.

Clearly customers pay more for ¡Scorchio! in the summer.

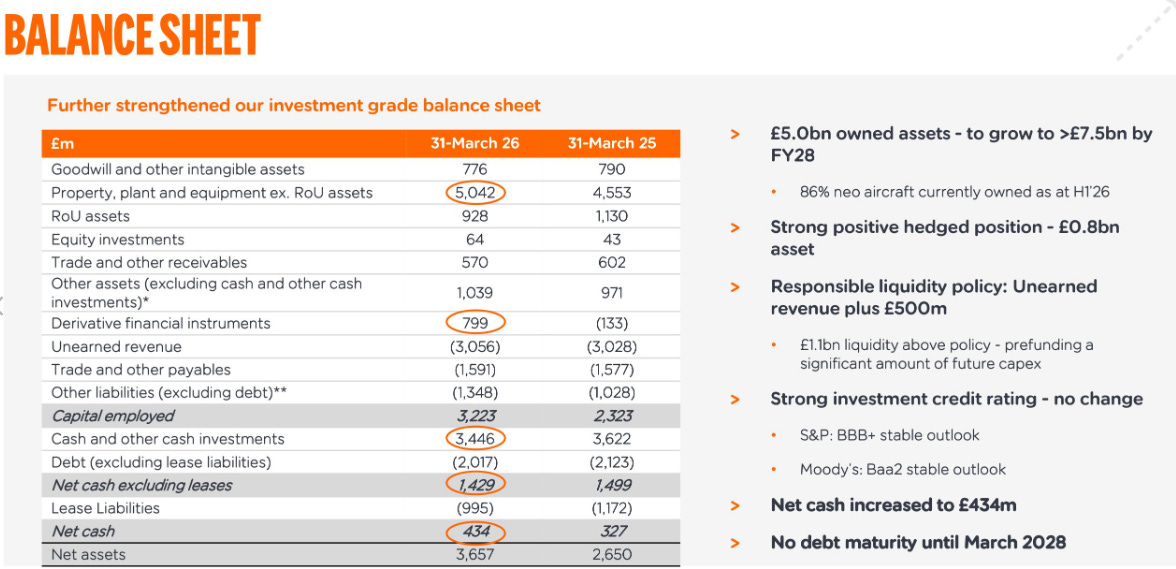

Fortress-Like Balance Sheet

Airlines go bust because they carry too much debt when a recession hits. Not easyJet. They boast an exceptionally strong, investment-grade balance sheet.

This financial cushion does two things: it protects the downside against any unexpected macroeconomic shocks, and it ensures they can comfortably fund their massive upcoming aircraft deliveries without diluting shareholders. When weaker, debt-laden rivals are forced to cut routes, a well-capitalised easyJet is perfectly positioned to step in and grab market share.

The EZJ remains strong with a near £1bn gain from fuel derivatives, and a fleet worth £5bn.

A NAV of £3.66bn vs a Market Cap of £2.77bn puts this at an incredible 24% discount. That £5.042bn of PP&E includes £4.92bn net book of actual aircraft it owns and there’s a further £0.9bn right of use offset by the lease liability.

And a holidays business thrown in for free!

Wait, what?

The Real Crown Jewel: easyJet Holidays

The market is completely missing the genius of the easyJet Holidays division. This isn’t just a side hustle; it’s an absolute cash engine.

By bolting a package holiday business onto their existing flight network, they’ve created an asset-light, high-margin monster. They don’t need to own the hotels to clip a massive ticket on the booking. It’s growing rapidly, printing high-margin revenue, and structurally transforming the profitability of the entire group. This shifts EZJ from a pure, cyclical airline to a highly profitable travel platform.

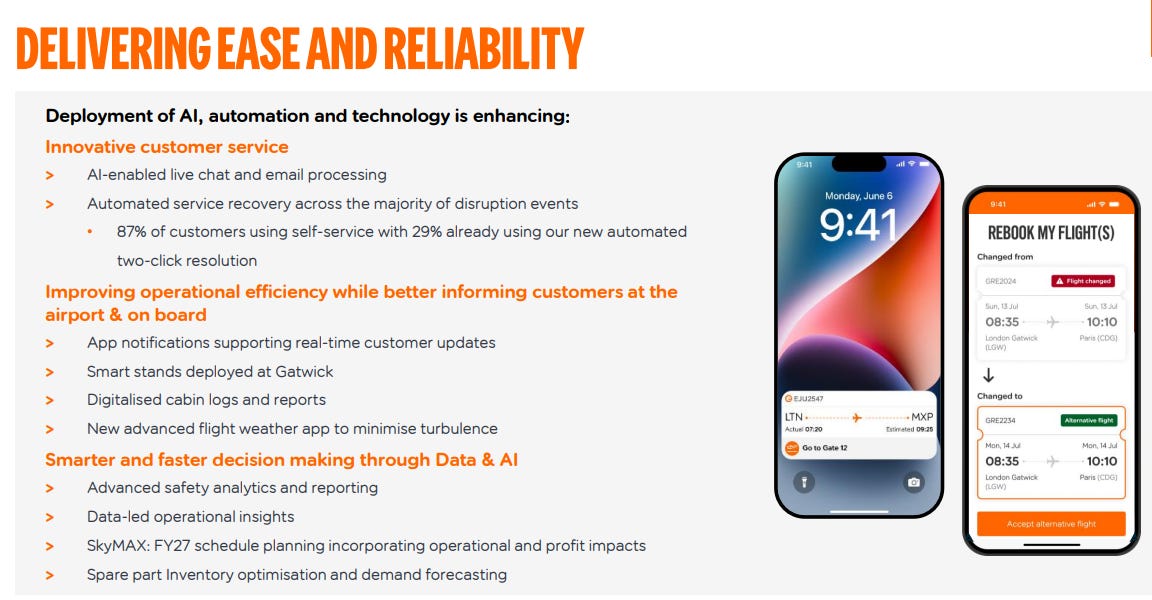

AI and Customer Service

EZJ continues to invest in frontline delivery. During the period, it launched the next phase of its enhanced training programme for ground operations colleagues, alongside the continued rollout of the internal colleague app.

The internal app provides real-time information to ground staff, customer service teams and crew, supporting more consistent service delivery and faster issue resolution. Seems to me the CSAT scores will go up for that one. Well done EZJ!

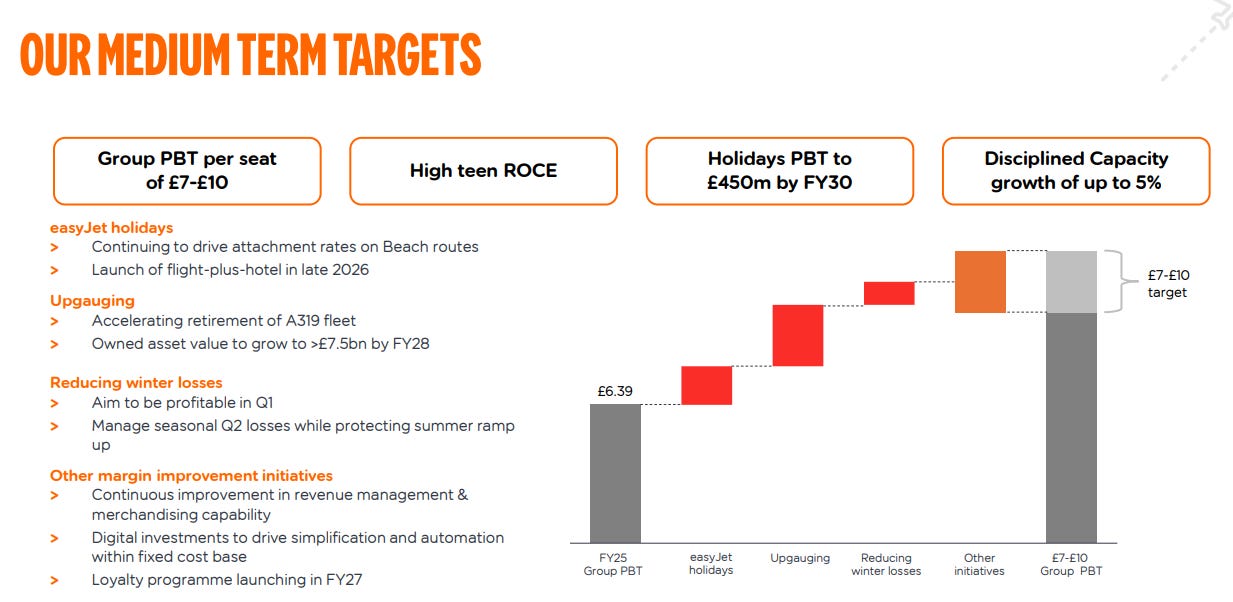

EZJ seems on track to hit its medium-term targets despite some serious headwinds.

CROSS CHECK!

What about the 2nd Half?

They think it’s all over? It isn’t now!

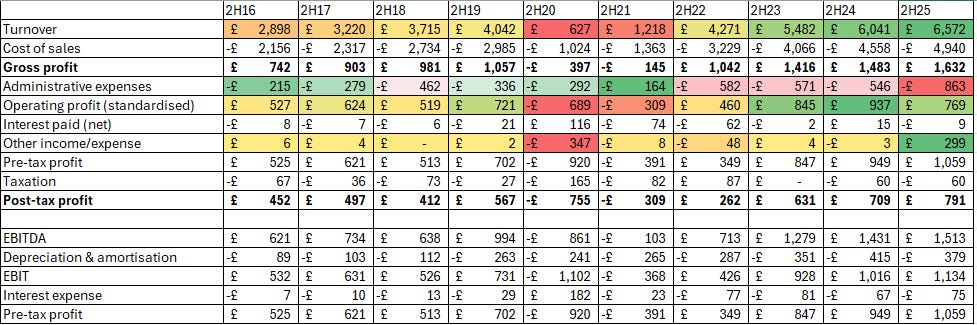

I showed the 1H results for 10 years. But consider the 2H results over 10 years.

The good stuff. The money making season.

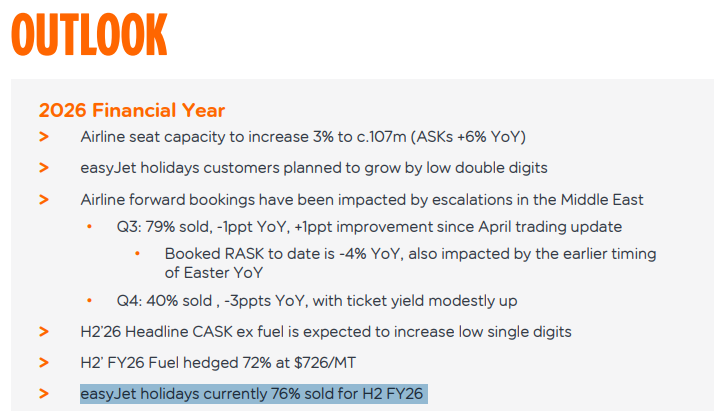

The outlook is for low double digit growth at EZJ Holidays and -4% revenue for the airline but impacted by an earlier Easter. That implies £6.5bn out turn so flat on 2H25.

With ticket yield modestly up and costs up too a flat 2H26 PAT of £0.8bn seems not unreasonable. If I’m right that’s a £400m FY26 net result.

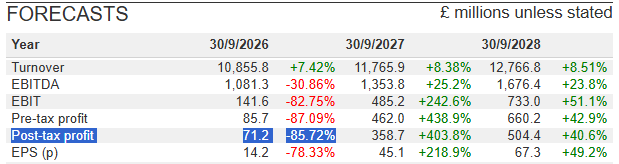

Much higher than the £71.2m PAT aggregate broker guesses.

Even if they are right and the OB is wrong (won’t be the first time mutter detractors), the brokers believe there’s a profit bounce in FY27 which starts on 1st October 2026 so is just over 4 months away.

At 370p a share the forecast is for a 8X P/E in FY27 dropping to 5.5X in FY28.

The Oak Bloke’s Conclusion

The market prices EZJ like it’s just another cyclical punt subject to the whims of the economy. But with the high-margin holiday business firing on all cylinders, with customers considering holidays “non-negotiable”, while EZJ implements cost efficiencies locking in from AI, clever IT as well as larger more efficient aircraft, and a fortress balance sheet, the reality is a business transitioning into a long-term, structural winner.

At a discounted valuation well below just the value of its aircraft, let alone the sum of the parts for its airline and holidays businesses, £3.70 a share looks….¡Scorchio!

…. and a compelling, mispriced opportunity.

Regards

The Oak Bloke

Disclaimers:

This is not advice - you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Hi OB! Excellent write-up, covering virtually all my musings, for which I haven't had the time to research comprehensively myself. However, we reached a very similar conclusion, which has resulted in EZJ becoming a significant percentage of my pf. Stay cool....

Nice writeup, thanks! If I look at JET2 and EZJ, I find JET2 better value - JET2 has net cash, very little intangibles compared to EZJ, higher return on capital and is (quite a bit) cheaper on EV/EBIT basis. How would you compare it?