Trainline ticker LON:TRN

Should you Choo-choo-choose to invest in TrainLine?

Dear reader

A commentator who says they only do desktop reviews recently looked at TRN and said they were “moderately positive” but worried about TFL’s project oval and GB Rail, then invited people to do much more detailed research to decide whether “other industry players” will chip away at TRN’s profits.

Another commentator worried that in 5 years time that AI will make brokers (aggregators) redundant, and you’ll just say “get me a ticket across Europe; get me the cheapest” and “bang, it does it for you.” The purchasing of tickets will be “thrown in the air - literally”. They conclude “You’ve got to be the dominant one”.

Let’s try to unpack these comments and do some detailed research to work out whether TRN is investable.

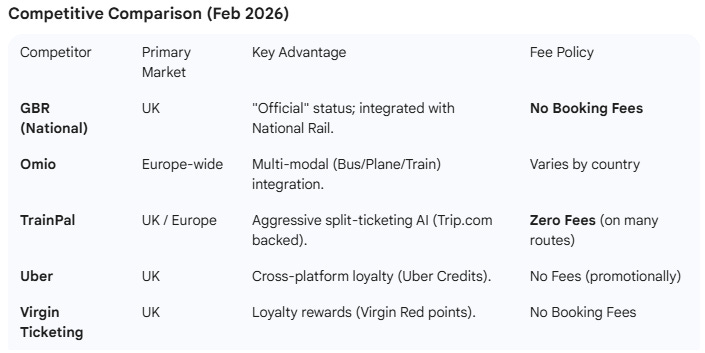

Trainline ticker LON.TRN is the dominant provider of railway tickets in the UK providing 60% of all tickets while the former Train Operating Companies (TOCs) now nationalised as Great British Rail or GBR accounts for 32% of tickets (including the dwindling number of paper tickets dispensed by thumb-twiddling members of staff in ticket offices who get to thumb twiddle more and more each day). Smaller players make up the other 8% of tickets.

A reasonable person might look at the options and say why would anyone pay fees when there are fee-free options?

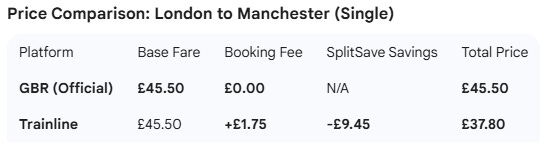

I tried an experiment. Over several popular journeys I tested Trainline which used its logic to save me substantial amounts of money compared with GBR. Never mind the £1.75 fee, I’m nearly £8 ahead in the example below. TRN will cycle through every combination of ticket combinations to find the cheapest for a route but will also consider single tickets, open tickets, even whether 1st class is cheaper than cattle class (baffling but true!). All in a fraction of a second.

I then tried Uber, but this only lets you pick a date for a train then forces you to scroll through all the trains from the first one of the day at 4am so by the time I’d scrolled several pages to 8am I’d given up. Uber launched 3 years ago and threw a lot of money at competing with Trainline yet three years on it’s rubbish. Utter utter utter rubbish.

TrainPal was a bit better but kept asking me to log in to Google. No thanks. No thanks and this time I really mean it… three times… are you serious? Goodbye.

UX is pretty important and in my personal life I’ve always found trainline to be the go to. Do they charge an extra tickle? I’ve not noticed and I’m a canny shopper but perhaps they’re sneaking an extra fee past me. But trying alternatives today did not convince me a better alternative exists, at a cheaper price.

But I now see why that commentator thought the purchasing of tickets would be thrown up in the air - first hand experience of using either TrainPal or Uber can cause that to happen…. along with your device as you propel it across the room in frustration. And I’m not even a rockstar.

GBR and the Railways Act

At this stage I should introduce the “Railways Act 2026”. This is a huge UK rail nationalisation programme introduced by Labour, and paid for through Rachel’s many new taxes. These taxes have paid for:

a/ Transition Costs (including GBR ticketing) £0.2bn has been spent so far.

b/ HS2, even curtailed, has cost UK taxpayers £7.1bn in 2025 alone.

c/ The CP7 5 Year Plan to improve the railways £44bn is being spent 2025-2029

d/ Northern Powerhouse Rail: £52bn is ear marked long term to improve east-west connectivity across the north.

All major train operators have had their franchises revoked. With a few exceptions:

1. The “Open Access” Survivors

Some private passenger trains will remain on the tracks because they do not operate a government franchise and operate at their own commercial risk, so are exempt from nationalisation.

Lumo & Hull Trains: Both survive driving competition on the East Coast Main Line.

Grand Central: Continues to operate private services to the North East and West Yorkshire.

Eurostar: Remains a private international entity outside GBR’s direct control.

Heathrow Express: Continues to operate as a private airport link.

2. Rail Freight (100% Private)

The government has explicitly stated that rail freight will not be nationalised.

Companies like DB Cargo, Freightliner, and GB Railfreight remain entirely private.

GBR has a “statutory duty” to promote rail freight, meaning the public body must actually help these private companies grow their market share to meet net-zero targets.

3. The “Shadow” Owners: ROSCOs (Private)

While the names on the trains are changing to GBR, the rolling stock will still be privately owned.

Rolling Stock Leasing Companies (ROSCOs) like Porterbrook and Eversholt will continue to own the carriages and locomotives, leasing them back to GBR.

The government decided against nationalising these because the upfront cost to buy the UK’s entire fleet of rolling stock would be tens of billions of pounds more money. What a black hole that would have been.

4. Devolved & Concession Operators (Private Management)

While DfT-contracted lines (like Avanti or GWR) are being nationalised, some regional networks still use private companies to manage the service on behalf of a local authority:

Elizabeth Line & London Overground: These are managed by private firms (like MTR and Arriva) under contract to Transport for London (TfL).

Merseyrail: Remains a private concession under the local combined authority

GBR’s Mandate and Objectives - and its WATCHDOG

GBR’s six objectives are reliability, affordability, efficiency, quality, accessibility and safety.

Its objective is not to be the best ticketing app. Its mandate is to run a lean IT operation.

Its six objectives are measured by a government watchdog the Office of Rail and Road (ORR). The legislation explicitly states that GBR will work “alongside a thriving independent retailer market”.

Read that word again reader. The legislation requires GBR to ensure that companies like Trainline are thriving, or face enforcement action from the ORR.

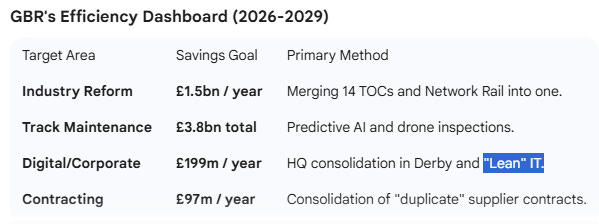

The idea of GBR is that it will help achieve various political objectives including Net Zero, and support the 1.5m new homes promised (remember those) and reduce the subsidy paid by taxpayers to the railway. It will achieve this through investment and consolidation thereby achieving these savings. Rachel’s taxes and Labour’s spending will deliver all manner of savings, apparently.

This is how:

Part of this plan is to grow journeys per year from 1.73bn to 1.76bn by 2029, so 30m more rail journeys per year by 2029. This doesn’t sound much of an increase but it’s actually quite a bit due to capacity constraints. The increase would need to be for offpeak and weekends.

Can Trainline survive the great UK nationalisation?

It’s true that GBR cut the commission to retailers from 5% to 4.5%. But even here the small print hides the facts. Revenue was cut by -0.5% but cost of sale per ticket was reduced by 0.25% so there’s actually only a net -0.25% cut of commission - so only half the cut. Given the price rises of rail fares of recent years, the reduced percentage is more than offset in absolute terms.

Could GBR cut the percentage further? I refer the reader to the Railway Act 2026 code of conduct and specifically to the REQUIREMENT that GBR will work “alongside a thriving independent retailer market”.

And if it doesn’t? Send in the ORR boys for Enforcement.

Speaking of codes GBR has no inhouse coding capability. It is mandated to run a “Lean” IT function. It is currently outsourcing major tech projects for the GBR Online Retail Framework to third party firms like Worldline, CGI, and Accenture.

£200m of spend later……. These third party firms are busy with a multitude of projects that does not bring GBR even equal to TRN in any way, let alone ahead.

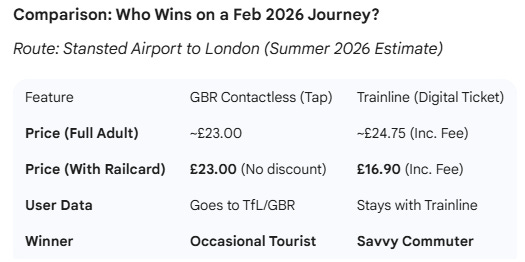

GBR through its third party Consultants is bringing together the systems of the 34 TOCs (train operating companies) into a single sign on for every train in Britain, plus building out what’s known as a “settlement engine” (no pun intended) to split the proceeds between the track maintenance dept and the train staff budget, and also working on Pay-As-You-Go (PAYG) integration extending the TFL network so that you can use your debit card to tap in and out including to Stansted and Southend airports. This is what’s known as Project Oval.

Project Oval

This extension to TFL is extending the system to commuter towns like Dorking and Chelmsford. The problem is tapping in can cost you more than a ticket previously did, so Trainline is actually exploiting Project Oval and the price differentials to SELL MORE TICKETS through clever targeted ads.

As Sun Tzu would teach: If you can’t join ‘em beat ‘em.

At what point will someone complain to the ORR about these GBR overcharges? Martin Lewis grab yer soapbox, you’ve got a job to do.

Just like tax avoidance with a complex tax code, the lack of simplicity to UK rail transportation creates an opportunity for an organisation like TRN. Even when there is only a dominant single rail operator for the majority of services. Ironic huh?

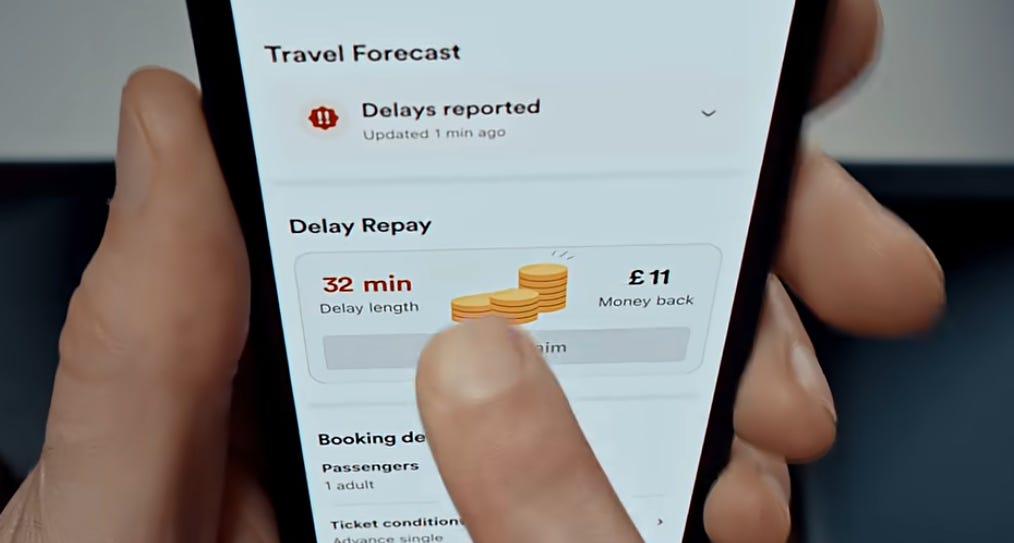

Trainline has also automated delay claims to become a click like this.

Can GBR, Uber or Trainpal do any of this? Nah.

Fill out an online form somewhere, if you can find it and be bothered. 99.9% aren’t bothered.

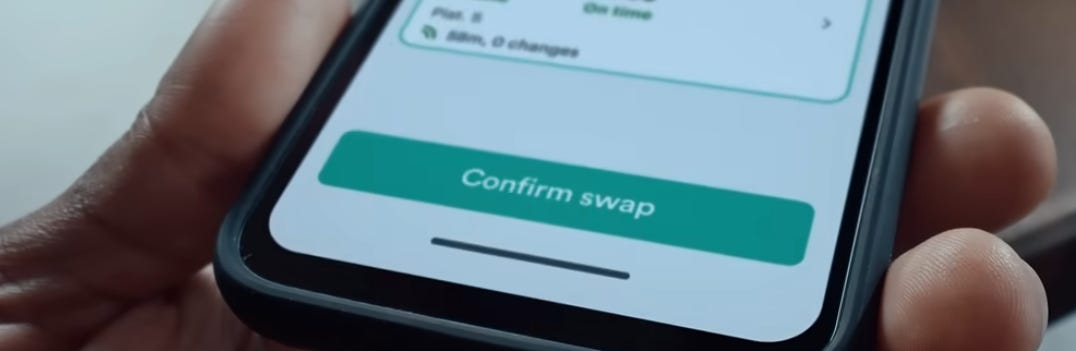

Need to move your ticket? Swap with two clicks, can the others do this?….. nah.

In fact Trainline advertise “we are the cheapest ticket or we’ll refund the difference”. Does anyone else advertise this? Nah.

Brokers are Dead, long live AI

AI might replace Trainline. Is that a fact? Or is that a hallucination? And I don’t mean an AI hallucination.

Let’s return to the facts of AI. Until (and if) we get AGI then it’s best to consider AI as a form of automation, and automation requires data and rules. The M of an LLM is a Model. That means data and rules, not some eye candy.

Seems to me that the only organisation with the skills, process-mapping, business processes and deep experience to build such an automation is Trainline. Consider that TRN have a full-time ARMY of over 500 of engineers, data and tech specialists. They live and breathe train/coach ticketing logic every working day. They carry out hundreds of tweaks to their systems each week. They’ve built out a global API of over over 270 rail and coach service providers covering most of Europe. They never rest.

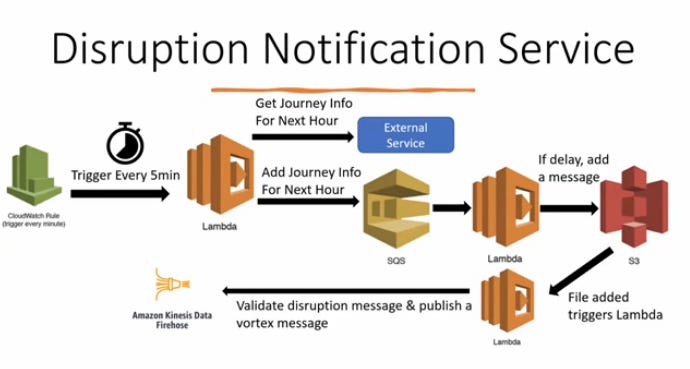

This is how Trainline talks through their Disruption Notification Service back in their Tech Summit 2022 for example.

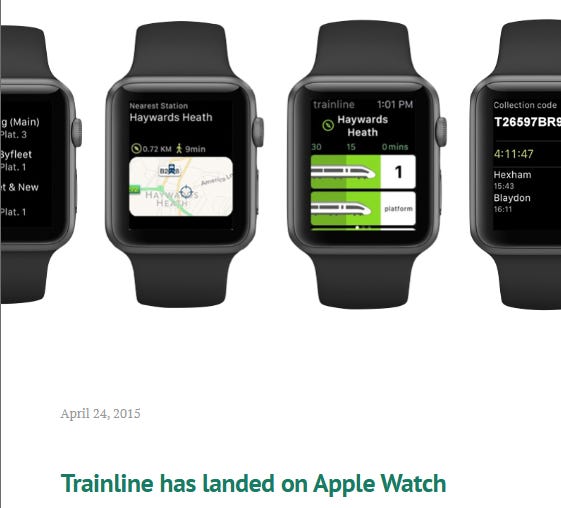

Might Trainline use new kinds of interface, perhaps with wearable tech? Absolutely. That already exists today. In fact it’s existed for the past 11 years actually!!!! Toot toot.

Meanwhile the chances of GBR introducing an effective AI with its lean IT mandate which can successfully navigate the complexities of its own ticketing are low. The public sector have NEVER successfully completed a major IT project except perhaps during wartime 80 years ago, and even then it was down to starvation, desperation and patriotic individuals like Turing who delivered results by breaking the chain of command and appealing to a maverick Prime Minister - Churchill. Will GBR unveal a Turing-style genius (perhaps portrayed one day by Benedink Cumblebatch) amongst GBR’s missed ranks of err zero developers…..

……and is Starmer another Churchill?

……

….

..

Ok, I’ve stopped hooting with laughter now.

No. I do not believe GBR will deliver an AI that renders Trainline redundant in five years.

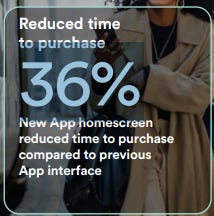

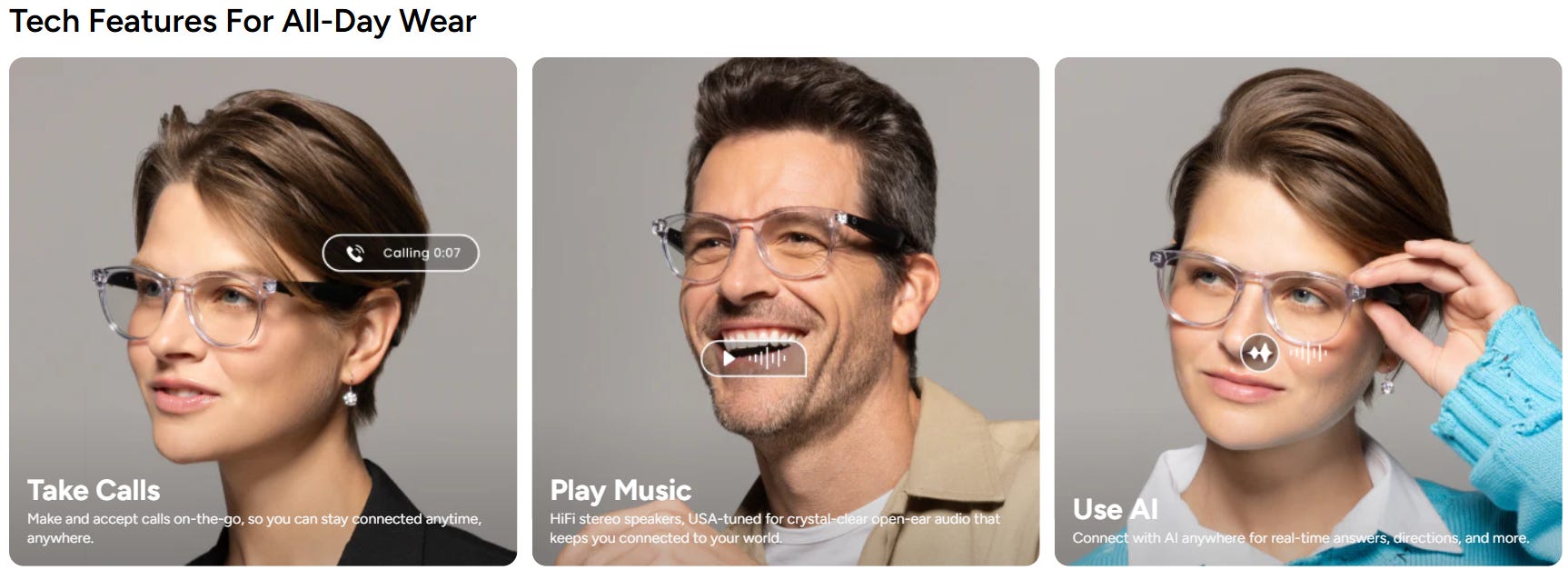

Avid Oak Bloke fans will know that I’ve owned a pair of Lucyd Smart Eyewear glasses for a number of years now. Have I ever bought a train ticket using my Lucyds? Nope. Would I one day? Perhaps. Today’s it’s far too slow and clunky to use voice to do anything much, and using an App on my phone is far easier. It just is. But TRN made the process 36% faster in the past year. If anyone creates an AI voice agent that renders apps the slowier and clunkier option then I’m convinced it will be TRN.

If I did one day have a voice-based AI sensible enough to buy train tickets I’d use my Lucyds to query tickets…. and it would query Trainline…. my AI agent would find which ticketing services offered an Agent Service for consumer Agents. Only TRN would have a host Agent ready to liaise with my AI consumer agent. That, folks, is the likely future of wearable tech. My agent talks to your agent.

You heard it here first from the Oak Bloke in Feb 2026.

Meanwhile back to the present and TRN in its latest accounts tell us:

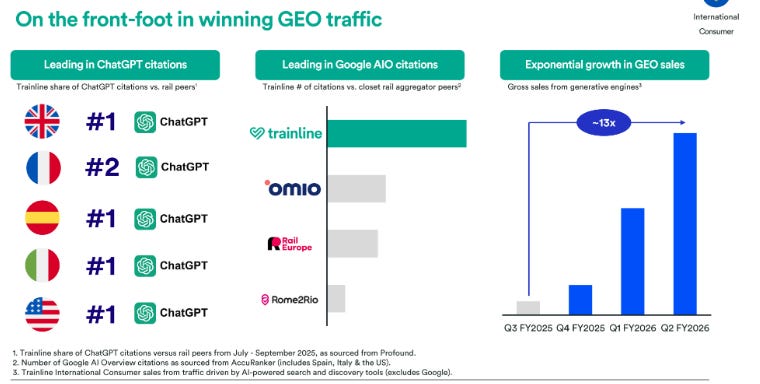

We are seeing encouraging early signs of traffic building from generative engines. We are the number one cited rail app in Chat GPT24 across almost all our core markets, and we are leading in citations from Google’s AI Overview module24, significantly ahead of other rail aggregators. As a result, sales from generative engines have grown exponentially – increasing 13-fold since Q3 last year - albeit from a low base.

What will AI do?

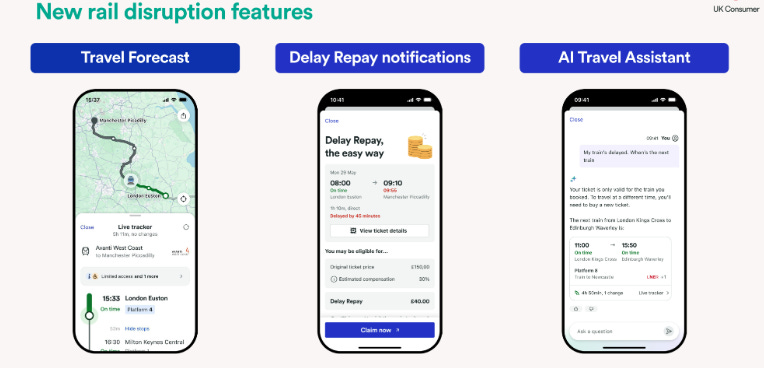

AI is not just about booking your ticket a bit quicker, or facilitating the purchase. The bit that matters just as much for customers is anticipating and advising on delays through TRN’s new feature its “AI-powered travel forecast” and its “AI-support on claiming delay repay” and an “AI Travel Assistant” too. TRN is the only one developing these journey enhancements.

Perhaps I’ll be using those with my Lucyd glasses some time soon too.

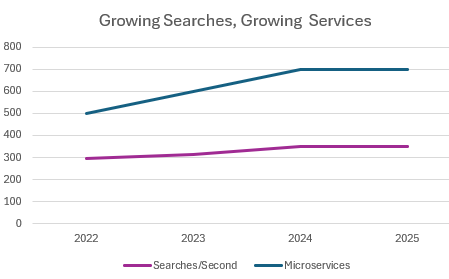

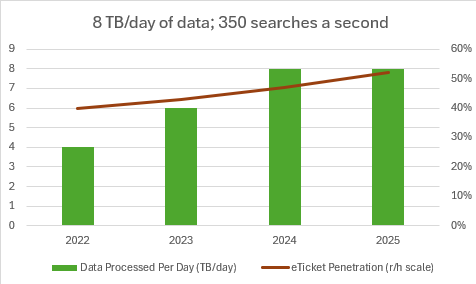

Over the past 4 years the searches per second at TRN have grown from 290 to 350 per second, the number of supporting microservices from 500 to 700, the TB of data processed per day has doubled to >8TB/day, as the penetration of etickets rose from 40% to over 52% of all sales.

Where in any of this justifies a more than halving of the TRN share price?

TRN Financials

£739.3m market cap at a 195.6p share price.

A further £150m share buyback program began 22/09/25 so that’s ~20% of remaining shares at the current share price.

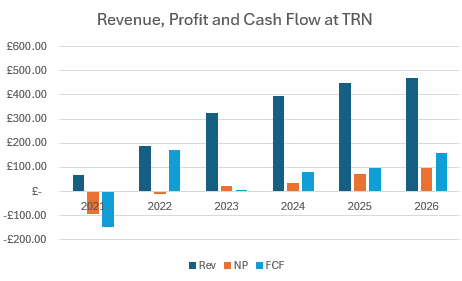

TRN have delivered a consistently growing Revenue, FCF and Net Profit

TRN is on a trailing PE of 7.5X!!!!

And a P/FCF of 4.7X!!!!

Where in the below chart of growing profits justifies a halving of the TRN share price?

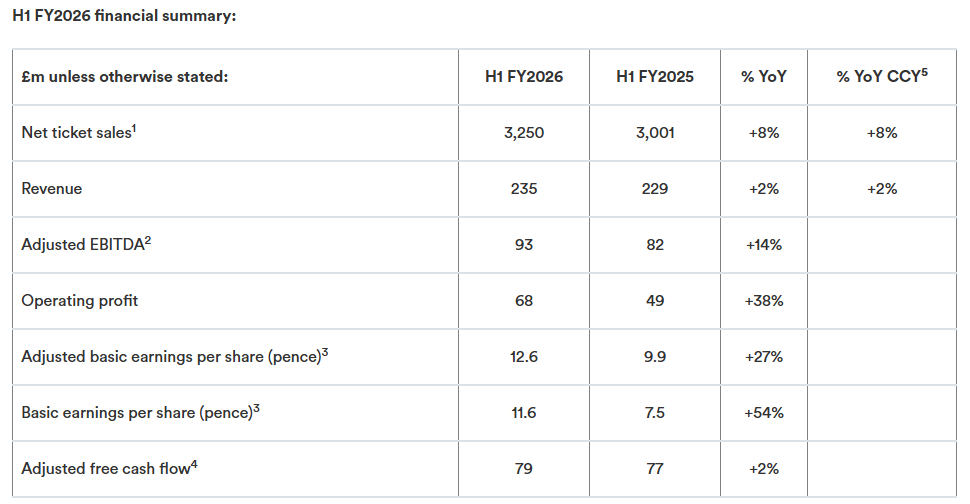

We see a further rise in profits in 1H26 to 31/08/25, mainly through TRN cost cut backs. Ticket revenue was up 2% and is pleasing considering that the introduction of Project Oval risked about 5% of ticket sales (£150m of ticket sales). So clearly Project Oval was less successful for GBR than anticipated. At what point does use of taxpayers money get questioned for such schemes, especially if passengers are being exploited with stealth price rises?

Beyond The UK and Beyond GBR

TRN is three businesses: UK Train/Coach Tickets, Continental Europe Train Tickets, and a B2B platform for travel companies and spend management systems.

It is #1 in each. It recently expanded its partnership with Amex (the world’s #1 Travel Management Co) and Trainline won Business Travel Partner of the year 2025 in the ground transport platform category at the prestigious Business Travel Awards Europe.

TRN Operational Achievements

TRN UK Digital Railcards - user base grew 12% YoY to 2.5m.

Digital Pay-as-you-go Trial in East Midlands - TFL-style tap in and out - but without all the infrastructure that TFL uses - just needs a Smart Phone - no hardware at the turnstiles etc.

11% ticket sales growth YoY in Spain and SE France where liberalisation of rail fares is underway.

Total TRN marketing spend for Spain/France/Italy totals £150m since FY23, driving significant brand recogntion. UK marketing is £90m over that period. If you consider that as an investment rather than a cost TRN is now the most recognised aggregator in Spain. That cumulative marketing spend equals about 70p per TRN share.

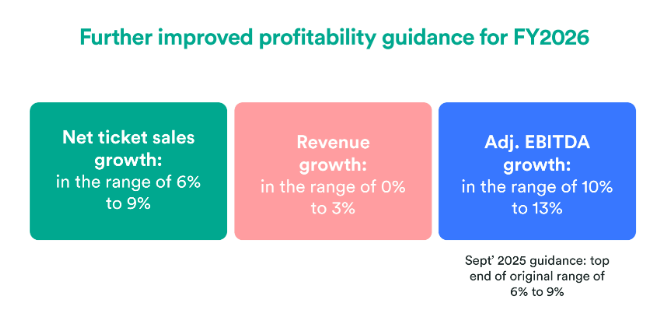

TRN guide 10%-13% profits growth for the rest of FY26 (to end of Feb 2026)… an acceleration of profits.

The Train in Spain price falls mainly versus the plane

If there is a spectacular statistic it is the growth of rail travel in continental Europe…… when rail privatisation is done right just look at the results. Avoiding the UK’s mistake of setting up local monopolies, and instead setting up competing services on the same routes. You see the same effect in the UK of Flix Coach vs National Express.

Domestic Spanish flights on certain routes are down 80% while rail is up by around the same.

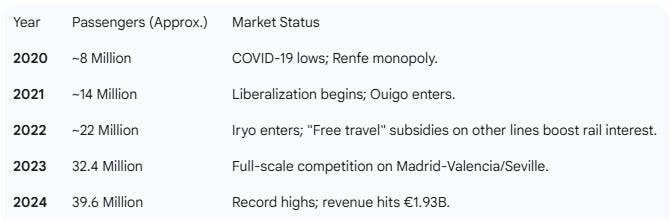

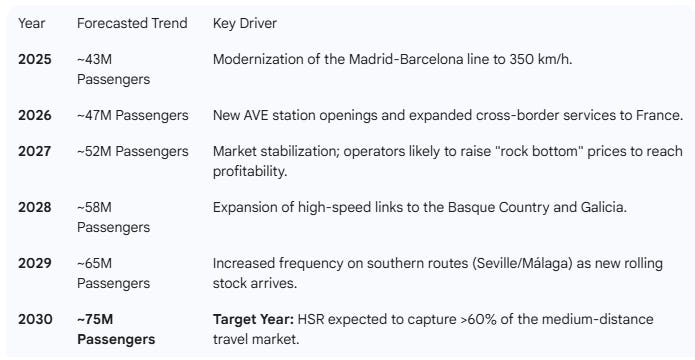

The complexity of comparing multiple services along these high-speed routes needs TRN. Consequently, TRN has become the #1 aggregator on any such routes in Spain. Consider the past growth of rail travel in Spain in just the past 6 years:

Passenger journeys have grown by 400% since 2020, dropping prices and introducing competition. Many routes now have four competing services Renfe, Ouigo, Avlo and Iryo, plus cross country competition too. Over the next four years competition across high-speed routes is set to grow enormously!

So a near doubling of passengers by 2030. At a price about six times less than the UK.

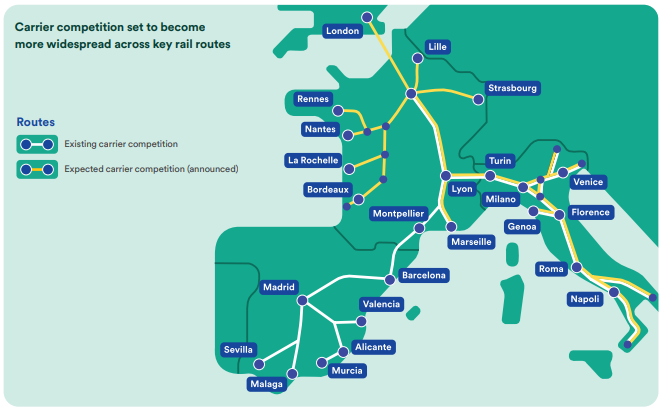

Italy’s high-speed rail market will be 153% larger by 2030 mainly due to a build out of high speed rail to Southern Italy, and where France’s market is forecast to shrink in Euro terms due to lower forecast fares due to competition, but the passenger numbers in the period to 2030 are forecast to double to 200m passenger journeys in France.

350m high-speed passenger journeys and a €12bn market size where Trainline today owns €0.7bn (~6%) and could appreciably grow that share especially where multiple operators begin to compete making a comparison tool more valuable. Market share jumped from 5% to 12% in Spain after multiple operators were introduced, and continues to build.

Conclusion

TRN is by far the #1 train ticketing platform in the UK, #1 on the continent within the liberalised areas of rail, and #1 as a B2B Travel Solution for European Rail.

That liberalisation of European rail and competing train operators will continue in the coming years, even while Labour reverses that process for the UK, and attempts to roll back privatisation, offering complex rail fares that TRN can help consumers navigate.

Despite this nationalisation, even in the UK, TRN helps passengers navigate complex ticket prices and plans to embrace new functionality, seeking to enforce a level playing field with GBR’s retail arm, and get enforcement action if necessary.

The rights and obligations of TRN and GBR mean it is not as exposed as some commentators have speculated. Is TRN really exposed at all? The legislation is clear on encouraging a THRIVING retail environment, and the enforcement action of the ORR watchdog.

Meanwhile with ~20% MORE TRN shares being bought back, and a growing market in liberalised areas of continental Europe, to buy TRN for 7.5X earnings seems fundamentally mispriced for a successful and growing business with a wide moat that will - in my opinion - widen that with the ongoing development of its platforms.

Regards

The Oak Bloke

Disclaimers:

This is not advice. Make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

OB..for some reason I am reading this at 3.00am despite TRN being well outside my normal area of investment interest...As I am enjoying it to much, am I becoming an investment "anorak" ? .... Fascinating, thought inspiring and amusing research!

Thank you for an interesting view on TRN.