Dear reader

I suspect the Oak Bloke might have flummoxed the Ecora BoD with questions on this morning’s presentation. The shaded area on the 2024 strip is the 1H24 mining area at Kestrel (their Met Coal project) and the 1H25 area looks bigger so I asked whether they knew approximately by how much.

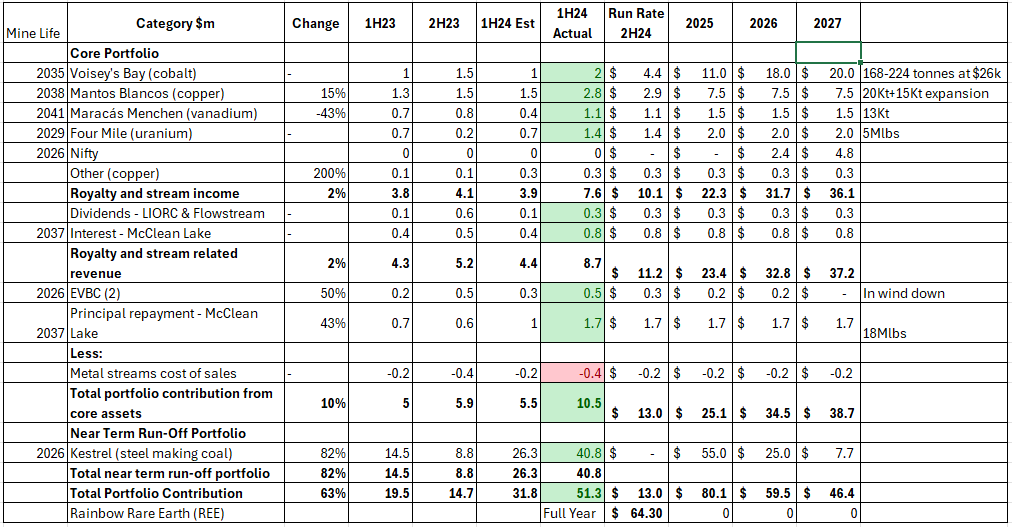

You see there’s a $51.4m asset on their books discounted at 10.5% based on future price assumptions. It was interesting to note that there was a $23.9m loss in 1H24 (which is a depletion loss) while the royalty itself was $40.8m - 70.7% higher.

If we applied the same 70.7% uplift to the $51.4m remaining that’s an $87.7m future revenue stream, and if I had to guess I’d say based on the diagram below we are looking at $55m, $25m and $7.7m in 2025-2027. (i.e. the 2025 strip is at least 30% bigger than the 2024 strip but met coal prices could probably be a bit lower)

Let’s talk about the results themselves compared to my forecast. A larger tax charge (Kestrel’s income is taxed at 30% I learned) and an adverse revaluation of Kestrel meant the out turn was lower than I’d expected, but the net profit of $11.5m equals 3.4p for 6 months performance - so not bad!

Ecora speak to a number of “near term catalysts”. Personally, Voisey’s and Nifty feel near term and everything else on this list feels “medium term”, so let’s focus on those.

We know that Voisey’s Bay is ramping up its underground operation.

Four deliveries of cobalt were received in H1 under the Voisey’s Bay stream (each delivery is 20 tonnes of which 70% is attributable to the Group). With the Voisey’s Bay Mine Expansion Project construction phase nearing completion, production volumes are expected to ramp-up with between 8-12 cobalt lot deliveries expected in the second half of 2024 and 20-28 in 2025, 36-38 in 2026 and 40 from 2027.

Ecora is entitled to receive 22.82% of all cobalt production from Voisey's Bay up until 7 600t of finished cobalt has been delivered, which then reduces the stream to an 11.41% entitlement thereafter. At the current $15.25 price per Lb of alloy grade cobalt that’s $255.4m and future higher prices of cobalt could make that much higher.

Nifty

Meanwhile Nifty is a brownfield copper project in Australia so a “restart” is a recommissioning, and a 36Kt at 1.5% realised value so could equate to $4.8m a year.

What emerges assuming steady state metals prices is a far less bleak picture, than people might suppose. I am making the assumption a brownfield copper project can restart in a 12 months timeframe at Nifty and that Voisey’s continue to expand their operation. But assuming zero production growth elsewhere, zero price increases on copper, uranium, cobalt, coal (or reductions in coal’s price to be fair).

After 2027, we know other projects begin to come on stream, and the picture brightens further for ECOR.

Cobalt

Taking Cobalt at $15.25 Lb for example, this is nearly half its 2021 price. This report from the Cobalt Institute is very interesting reading. Demand for Cobalt is rapidly growing but supply has rapidly grown also, particularly from the DRC and Indonesia the latter who are rapidly building out battery supply as a “pet project” industry to capture the value chain. Both Indonesia and the DRC have poor environmental credentials so Cobalt from places like Voisey’s bay could attract a premium in the future.

Debt

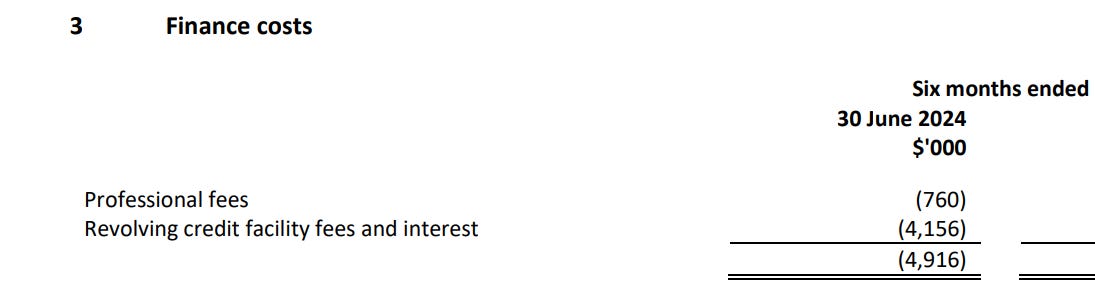

Debt headroom was extended from $150m to $225m, versus $86m net debt. ($99m gross debt). This is on terms of SOFR +2.25%-4% and given SOFR is currently at 5.35% and interest paid was $4.9m in H1, so debt is costing ~9.4%+. Plus a $2.25m arrangement fee which added $0.76m costs in 1H24, and will cost $1.5m more over the next 30 months ($0.3m per 6 months) on top of borrowing costs.

ECOR speak to paying this down but also acquiring royalties over producing assets (plenty of opps in the UK junior mining space at knock down prices) so its 4 priorities pull it in different directions.

It’s certainly possible we might see further royalty acquisitions, certainly we should also see deleveraging, along with “steady dividends” as well as buybacks. At a 60% discount to NAV buybacks feel a great way to boost returns for shareholders.

A 1.7c dividend each half equates to a 2.6p per share or 4.1% yield at today’s 60p share price. (Of course eagle-eyed readers who topped up yesterday morning at 54p just after 8am that’s a 4.8% per annum). That dividend costs the business around $8.4m a year.

Conclusion

I think once you do the maths and work through the prospective what ECOR could deliver over the next few years a couple of things become apparent.

First that while “the cliff edge of Kestrel” is there yesterday’s update showed there is also a bumper 2025 ahead, a reasonable 2026 and by 2027/2028 other holdings like Voisey will have picked up the shortfall. Past 2028 it gets pretty exciting. So at what point will the market forward price that excitement?

Second that while the dividend has been cut and I think it highly unlikely they will splurge more than a 4% yield, the dividend is decent, it’s ok.

Third that paying down debt would boost returns by quite a bit. PBT by about 40% based on the current 1H24 numbers. Less debt also gives optionality and breathing space, although to be fair there is plenty of headroom (nearly $140m).

Fourth the value of the assets is not reflected in the price, and this share remains out of favour. 60% discount seems exceptionally high for what is a dividend paying and growing share. The key thing to think about here is the growth will be at no cost to ECOR. The miner pays to develop the mine, ECOR collects a share of revenue.

Fifth this is focused on a range of metals targeting energy transition is continuing apace and demand is growing. At some point increased demand will translate into higher prices. Cobalt prices appears to be at a nadir (a low point). Vanadium too. Iron Ore too. Readers will know I’ll bullish about Uranium. I also see Copper moving upwards. Nickel remains low and is forecast to continue (again through Indonesia’s pet project expansion) but we know projects (including West Musgrave are getting mothballed) even though it has superior economics to the average Indonesian project.

So my view remains this could be an interesting way to profit from the energy transition as metal prices move to what the forecasts say they “should” be, with some comfort - and plenty of discount to intrinsic value too.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".