WJG's under the hammer

What happens if we take Watkins Jones (WJG) to the auction?

Dear reader

I couldn’t help myself today. I saw this.

Eagle-eyed readers who read my recent article “Does You Digs It” will spot what I spotted.

And mole-eyed readers are now curious.

Leaving aside that INCLUDING the horror of Grenfell and the subsequent fall out of rectification costs in tower blocks of over 11m high, that the average profit for the past 4 years at Watkin Jones (LON:WJG) is £6m per annum. (2H20 to 1H24). So today’s £53m market cap means you’re buying a company at less than 9 times average earnings - post exceptions.

That’s despite forking out £33.9m of exceptions, or £37m including other exceptions in those 4 years.

So that’s an additional +£9.25m underlying annual profit which means £15.25m underlying profit so less than 3.5X net earnings.

Wow.

But let’s imagine somehow those profits cease. Not sure quite how. Watkins Jones has successfully built 80 residential developments and 48,000 student beds across 143 sites over 25 years. But let’s assume the worst. Let’s assume suddenly it doesn’t. We also need to pretend 214 flats haven’t just completed in November 2024 at one of the developments in Leatherhead, nor the approval given to the new Leeds scheme for 230 flats in an office conversion. Those pieces of good news will only increase our numbers and value if we consider those.

Instead, let’s sell Watkins Jones. Yes reader. Right now. Roll up! Roll up! ‘oo wants a nice shiny digger? Everything must go!

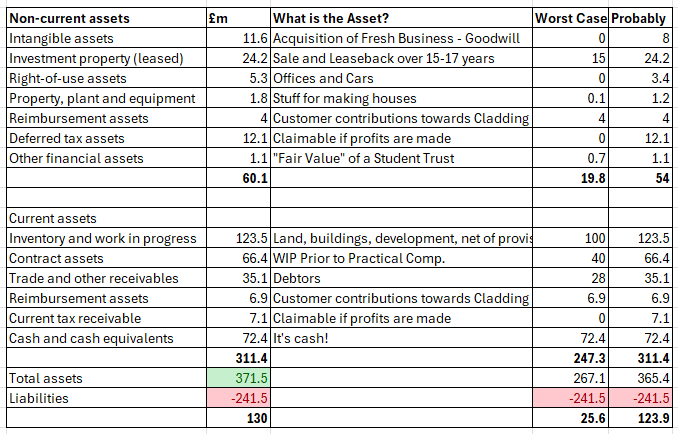

Here’s the Watkins Jones balance sheet (I used the one from the last annual result 2H23, rather than the interim 1H24 but they are largely the same - in fact there’s £2m additional equity I’ve diddled myself out of). But I don’t care.

The numbers are strong enough to not need it.

I worked through each asset and considered a worst case and a likely case. As you can see I tried to sell the highly profitable Fresh Business. This is an accommodation management service run for 20,000 student on behalf of Universities. It makes strong 56%-66% margins. Worst case? I can’t sell it. Bang. Gone. But reader. Let me tempt you, probably. Let’s assume you look at my accounts and see £2.5m of profits over several years. What’s that worth? Do I see 3.3X earnings from a bidder in the room? I think £8m for a business like that is achievable all day long.

On a good day 10X earnings because you know this is a growing segment where 294,000 more students demand accommodation compared to 10 years ago. But if I start achieving profits on disposal I’m going to be “too bullish”, so let’s shake on a bargain 3.3X.

Next my sale and leaseback are properties valued at fair value (IFRS15). They will earn an income stream over the next 15-17 years. Worst case? I’m going with a 40% haircut. But the likely outcome is they are in the balance sheet at book and housing has been going up so I reckon realising £24.2m is quite easy. I’m avoiding another gain on disposal.

Next right of use. Worst case - those leases don’t get used. Worth zero. Probably, yes take a hair cut and can sublet them at a 1/3 off.

Diggers and stuff next. 95% discount worst enough for you reader? A 1/3rd off is more likely. There are equipment auctions and dealers I can use I reckon. I can shift the equipment. It’s in demand. 300,000 more homes need to be built per year in the UK after all.

Money in the bank from customers. Is cash. Worst case is I lose none of it - it’s cash.

Deferred tax assets - worst case I can’t use those so they’re worth zero. But in the real world when I make profits I can use them. So 0% off and I just use them in a “probably” scenario.

Selling a trust? 40% off for a quick sale, but it’s valued at fair value. So probably I can get its fair value.

Land, buildings next of all - well again book value isn’t market value as you know. But let’s say 20% off for a quick sale on a land grab. Realistically book value is more likely. Profit on disposal possible here too.

WIP Assets next. These are properties, possibly half built. Worst case I down tools and sell it to another developer at 40% off. But realistically I’d complete them and turn them into debtors and get paid. So 0% off probably.

Finally we’ve got more customer cash, and more tax credits and finally cash. Lots of cash.

The results?

The outcome of the rather unrealistic scenario of never again turning a profit and selling everything would net somewhere between £25m and £124m. That’s a £100m continuum of possibilities.

Even if we end up more than a quarter way along that we are at breakeven to today’s share price. Halfway and there’s 40% upside to buying WJG at 20.95p today.

Even if WJG only perform as badly as the last 4 years (i.e. more exceptional costs) then the £53m market cap - £25m net “worst case” net assets, that’s a £28m net cost so 4.6X earnings based on those £6m worst case earnings.

Or less than 2X the underlying earnings.

The upside.

But if the business performs at my “reasonable forecast” level of £30m and even deducting £10m per year for the next 4 years for cladding costs i.e. £20m net plus you further assume that the “probably” scenario is fair then what does that make you?

Well reader, well done. You are an eagle-eyed reader. Because to my reckoning, that’s a 57% discount to fair value (based on “probably”) or a 60.5% discount based on book NAV. A heck of a lot more if I’m right about potential for gains on disposal (from a realisation of assets perspective).

Valuing as a going concern business generating an underlying £30m per annum i.e. 1.75X Price Earnings and a 2.65X forecast performance based on a reduced £20m per annum is cheap, cheap, cheap.

And I’m not even considering those £11m of unclaimed tax assets in those calculations. Plus am considering that every single penny of the money set aside for Cladding (which includes an unspecified contingency) will have to be paid over.

What does the Chattersphere think about the price drop?

“It was the steep increase in inflation (due to 10% increase in energy prices) that caused the sell off”

“More likely a fund reducing, or a short increasing”

“The Building Safety (Wales) Bill will be introduced before summer recess in 2025”

Conclusion

The reasons for the drop are moot. Don’t think it’s inflation (unless you’ve got a seller with incredibly slow reactions and has taken 18 months to push the sell button). The Wales bill is a red herring too. But it could be a seller in the market.

If it is, their loss is someone else’s gain as the fall seems completely overdone. I wrote this article to set out my rationale for my decision to average down here today.

Oh and if you did want to find out what two Estate Agents thought about your purchase later on in the show then you can apply, reader, to appear on HutH - here’s how. Not sure what Martin Roberts will make of those Diggers, Trusts and Halls of Residence you picked up at huge discounts. But a spruce up and a lick ‘o’ paint and I’m sure it’ll work out.

By the way, it transpires Martin Roberts and I share common cause in raising awareness for homelessness. 61 year old Martin - bless him - decided to sleep rough last week in Brizzle. He’s raising money for CEO Sleepout and you can support him here.

If you find this article to be of some benefit then please consider supporting Martin. He’s crazy enough to sleep out voluntarily, while you and I reader are not. Thank you!

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

In their last TU they said the 'board is undertaking a review of a range of options that may be available to enhance its medium and longer term funding position, thereby allowing the Group to capitalise on a market recovery.' This does not sound like a raise and at the current price would be somewhat ridiculous though it appears the market fears that. Wouldn't it be sensible to address the precipitous share price fall and explicitly rule out a raise?

You did mention in the comments the chair is buying shares often, I could only see the last time being in August after the profit warning, is that the last purchase you have also?

I also hold Watkin Jones. Best, Mike

I used to hold here, and did OK. But the clarion call to abandon ship for me was the founding family dumping shares a while back. They must know the business better than anyone!