Worth the AAZ-ard?

Re-considering Anglo Asian Mining

Bid/ask 130p/135p

Dear reader

I last covered Anglo Asian last May in my article “Copper! Part Two”. That was very nearly one year ago. “Lots to like”, I said, and then there was a however:

Given that this is a top-voted reader idea and given AAZ is the stand-out performer up 805 since that article 1 year back. Did I simply get it wrong?

A contrary thought is what would make Phoenix Copper PXC drop 75% and what are its forward prospects? Readers will also spot that CAML, ECOR and JLP are within my coverage universe. PXC remains pre-revenue and is seeking finance. Given its US location on private (patented) land that’s a high-risk/very high reward option.

Looking at these copper ideas you’d imagine Copper price to have crashed over the past year. No. Forecast to increase too.

For those forecasting doom and gloom there have been a number of data points that do not make sense to me. Dr Copper being one of them. Copper is highly sensitive as a measure of economic contraction and expansion. Dr Copper has been telling us worldwide depression isn’t imminent. Yes there was a sharp sell off on Lib Day. A sharp recovery since. The strength of the rebound is telling. Yesterday’s US jobs report further evidence that the “recession” is one of the mind where we risk talking ourselves into one but there isn’t one. A bit like someone persuading you to put a gun to your head to prevent someone putting a gun to your head. Isn’t that the plot at the end of Fight Club?

The cheapest copper cost of production in the world is $0.95/lb AISC (incredibly) so there’s a 70%-80% margin possible. Even gold doesn’t deliver that! (for now)

ANGLO ASIAN:

My beef was with their political risk and disclosures.

Political Risk

This has reduced. Progress was made towards regional peace in March 2025. A draft peace agreement to normalise relations, marking a historic step after nearly four decades of conflict. Armenia accepted Azerbaijan’s proposals on two key unresolved articles: one concerning the non-deployment of third-country forces along the border, and another on mutual withdrawal of claims from international courts. Nagorno-Karabakh Resolution: The region is now under Azerbaijan’s control, with efforts focused on reconstruction and resettling displaced Azeris.

That’s exciting to hear that’s improved… onto the other concern disclosures.

Disclosures

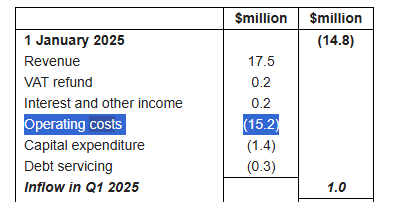

Frustratingly the latest information does not contain an AISC. AAZ lost $5.5m PBT in 1H24. They didn’t disclose an AISC in 1H24 either.

The 1Q25 trading update also doesn’t give us a clear disclosure on costs, other than we see -$15.2m opex and -$1.4m (presumably?) sustaining capex? -$16.6m total.

That’s a -$2,053 per Gold Oz Eq’t AISC.

Why not just say that?! Why be coy?

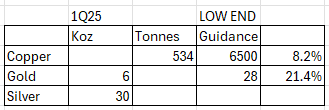

A Feb 2025 broker guess claims an average -$1,332 per ounce is achievable in 2025 based on the production 6.7Kt of copper. Yet copper production is 0.53Kt in 1Q25, suggesting production would have to quadruple in 2Q25 and beyond to hit 6.7Kt in 2025.

The Company's strategic plan for growth is to transition to a multi-asset, mid-tier, copper and gold producer by 2029, by which time copper will be the principal product of the Company, with forecast production of around 50,000 to 55,000 copper equivalent tonnes.

AAZ plans to achieve growth by bringing into production four new mines during the period 2025 to 2029 at Zafar, Gilar, Xarxar and Garadag. The first of these new mines, Gilar started production in March 2025.

Once again I find I’m frustrated trying to make sense of their production plans. We learn that Gilar adds a large gold component to production given its reserves equate to +250% existing M&I of Gold and +66% to Copper.

Assuming 10% depletion from 2024 then 25koz production is added via Gilar. This is based on a target given in the 2023 annual report. However that report assumed production at Gilar by the end of 2024. It’s now this month so optimistically Gilar might deliver 18Koz in 2025?

AAZ also provide guidance in a different format split into Gold and Copper. Back in 2023 the Copper/Gold ratio was 4.9X, today it is about 3X ($9600 vs $3200)

So that translates to 47.5Koz- 50.4Koz (although AAZ use a $2800 gold price in the Feb guidance to give a 49Koz-55Koz).

Even being generous and allowing their lowball gold price that’s 20% down on what they said a year previous. I’m not feeling the love for AAZ and finding their opaque reporting a bit irritating. Although I remain intrigued why this has broken ahead of the pack of the other Copper-Copper companies in my prior article.

Their 1Q25 results give me further reason to shrug: A quarter through the year and only 8.2% of guidance achieved. They say there’s no guidance for silver because it’s immaterial. 30Koz per quarter is still $4m a year. Is $4m immaterial? The irritation continues.

Checking back to 2024’s results AAZ hit gold and copper guidance with 15,251 ounces/gold and 534 tonnes of copper both over midway - that at least is encouraging. It is now the 3rd May 2025 and 2024’s Financial Results have not been published. That’s very slow and a black mark against it.

We know AAZ made $17.5m revenue in 1Q25 and incurred -$16.6m Opex and (Sustaining?) Capex. So made a $0.9m cash operating profit. I play “Mastermind” to work out price per unit of gold, copper and silver and am shocked. Copper is sold for the equivalent of $7,500/tonne, Gold just $2,110/ounce and Silver $28/ounce. The mix of revenue might be slightly different but this mix agrees back to the $17.5m revenue.

Why so low?

The answer is a series of royalties and kickbacks to the government. On top of this in 2022 $7.5m PBT was taxed at >50% to net at $3.66m

The presentation deck is accessible here and looks the part. Very positive.

The broker (Feb 2025) reckons AAZ can achieve $45m profit after tax in 2025, and $101m net profit in 2026. It reckons tax is just -33%, not -50% so perhaps 2022 was a one-off? Looking back to 2021 tax was -41.2% and 2020 it was -35%.

That tax doesn’t include royalties or production shares of 51% to the government.

AAZ would have to improve their production cost dramatically - and perhaps they can. Of course we are seeing legacy mines and Gilar should be cheaper. But the current numbers are simply horrendous.

Again playing Mastermind to get the production costs to agree back to -$16.6m (where silver is a credit) then you find AAZ are making $9 an ounce on Gold and zero on copper. Profit is that “immaterial” silver!

Profit is little more than the “immaterial” silver

The problem I now have is no matter how good Gilar is and it might be amazing although there’s no proof to that yet. Gilar’s MRE is 1.22g/t Gold and Copper 0.62% so those numbers are good but not spectacular.

Meanwhile the legacy mines are horrendous. There’s no other way to describe them. You would close them down at those kind of costs if you had common sense.

The same broker forecasting squillions profit in 2025 also forecast a $10m profit after tax for 2023 during 2023, and the outcome was -$24.2m. A different broker guessed a profit after tax 2023 of $1.6m growing to $13.9m in 2024. Of course the counter argument might be, ah hah, but that’s because the government closed down much production due to a problem with the tailings dam and besides the conflict with Armenia affected things. And that is true. But it does introduce a doubt to the accuracy and reliability of blindly relying on forecasts which at best have been obsoleted by subsequent facts and at worst were overly optimistic to begin with.

If I check the chattersphere at recent posts people are excited by a shareholder who visited the mines and shared photos. Excited by the momentum. Excited by current gold, silver and copper prices and the impact that will have on AAZ. Commentators speak to “the future expansion”. They “guess 20p-30p dividends YOY if it goes to plan, which supports a £4 to £6 share price.”

Excitement. It’s not a word I’d use to describe very many of my shares. That’s probably because I’d sell out of “excited” shares. My shares are leper colonies, lowest of the low. Despised. And instead of excited I keep coming back to the mathematics of the legacy mines, and the word horrendous. Of course if you blindly rely on broker guesses and the AISC numbers they quote you might get giddy and excited here. As someone writes “$3300 and an AISC of -$1500 why that’s $63m from gold alone. A P/E of less than 2…. 2!!!”.

Yes, it is if you can get to AISC of -$1,500 for 2025. And indeed a sell price of $3,300 per gold equivalent ounce.

Can they? They certainly didn’t in 1Q25 and they ain’t shutting up the horrendous mines. Besides -$2,053/oz AISC in 1Q25 means ($6000-$2053)/3 you need to achieve an average -$1315/oz AISC in 2Q25 to 4Q25 to achieve an average -$1,500/oz in 2025.

Perhaps 2026 and beyond could be better. But AAZ haven’t managed to stick to their plan in 2023, 2024 and 2025 and achieve their forecasts so far. At best I’d wait on the sidelines rather than join the giddy momentum I see in the chattersphere.

Conclusion

My conclusion is unequivocal: SELL SELL SELL SELL

Regards,

The Oak Bloke.

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

You have this completely wrong. The last AGM was all about Demirli, a 20kTpa copper mine with $200m of plant in situ that AAZ has been given. For zero cost. It is likely to come into operation very soon, but the company is unlikely to announce anything until it is in production. It will have production costs of around $2k/T according to the last AGM.

As for Gilar...average grade from the gold there is 1.6 g/T. Last quarter the company made a profit producing from the dregs at Gedabek at 0.2g/T.

AAZ don't do investor relations. The board own over 40% of the shares. But there is a very clear path to Gilar being in full production, likely this month, and Demirli very soon after. But unless you went to the last AGM, you won't know about Demirli

Thank goodness I'd never heard of this.