You can't HEIT me, no matter how hard you try

Dodging bullets while ducking below its NAV - can Harmony head to former HEITs later in 2024?

Dear reader

One of the “near miss” ideas from readers contributed to the OB19 (remember I picked 10 out of all the ideas submitted and added 10 of my own), which I didn’t choose last December was HEIT (although I was tempted). “An attractive dividend but too little upside.” said the Oak Bloke (I knew UK BESS revenues had been substantially falling - see the BESS index below and had read the National Grid had begun to accommodate BESS but still had 18 months more work to go.

To dodge was the right move given the negative price movement across the sector in 2024.

It’s also true that BESS (Battery Energy Storage system) trusts had had a very prosperous 2021 and 2022 pushing share prices to premiums to NAV. BESS replaced assets which basically ran on a “just in case” basis as well as “extreme measure” assets like Diesel-powered “peaker plants” which were very popular 7 or 8 years ago.

I knew the days of peaker plants were numbered because I’d followed their fortunes. First via Jack o’three trades, nanocap Corcel (CRCL) which was a Papua New Guinea Nickel explorer, which reinvented itself as a UK Peaker Plant developer and is today instead an Angola O&G explorer. Despite having ideal peak peaker plant locations and grid connections they couldn’t develop the assets. Why? Angolan oil? Or was it that fossil fuel peaker plants were past their peak?

Second, I knew my local Peaker Plant which made a quite distinct noise when operational…..

…..and had been pretty quiet during pretty much all of 2022 and 2023 (except some winter days and evenings). But I also knew there was a saturation in ancillary services in 2023 caused by an influx of supply, while the easy money Peaker Plants had been supplanted, but growth into other services had been constrained by the National Grid (the 18 month ESO plan).

More supply and less demand was perfect for a collapse in prices. And some Jan 2024 National Grid software glitches was another body blow for the BESS sector. The collapse happened for HEIT on February 2nd 2024, when its Trading Update bad news was announced along with a paused dividend. People harrumphed, and sold HEIT.

Then HEIT’s 2023 results on Feb 28th led to a 9.8% NAV reduction and a fall in HEIT’s share price to a 33p low. A fall from lofty HEITs and all that.

Since that sell off which took HEIT to a ~70% discount HEIT has recovered back up nearly 50% to 48p/share.

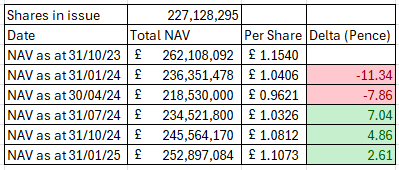

Noticeably on the 30th May, a further pause to the dividend was announced until 2025, and a further NAV reduction of 7.5% took the NAV down to 96.2p a share (not sure why the pink line in the chart below indicates a NAV reduction sone time ago…. it was last Thursday!). The noticeable bit was the market barely flinched. No one sold. No one harrumphed. No bullets flew. Why is that?

The NAV fell again, and the market barely flinched. Why is that?

Read on reader, read on.

Also, if you still hold HEIT, should you keep? If you don’t, should you buy? A discount to NAV of 49.7% beckons apparently.

Here are the reasons why I think the answer is yes and yes.

1.Capacity revenue and NAV growth

The first point is HEIT’s capacity (and revenue) is about to grow by about 50% to 395.4MW/790.8MWh. “About” being 3Q24.

It’s not just about the revenue. You probably already know this reader, but accounting rules force companies like HEIT to understate the value of assets under construction but also through applying a higher discount rate (more on that later).

….So 167.9MW is being added to 227.5MW assets operational in 2Q24…. the NAV is about to grow, reader. A lot.

The operational and soon to be operational projects:

2. Two hour Batteries

Second is that HEIT holds 100% 2-hour storage which is of course a longer duration. The average is 1.3 so most of HEIT’s competitors are 1 hour storage. HEIT holds attractive assets.

While two hour has a slightly higher pro rata capital cost the savings and benefits are substantial. The revenue per hour is higher. But also damage to batteries (reduction in longevity) occur when deep discharge (>70%-80%) occurs. 42-48 minutes if you are a 1-hour battery or 84-96 minutes for a 2-hour. The point is if there’s an opportunity to sell power at elevated prices HEIT’s competitors can only do so for 42 minutes without damage (in fact they calculate whether the elevation of price justifies the deep discharge beyond 42 mins). But it’s also the same for buying electricity from the grid at low or negative prices you can only buy cheap or free power for 42 minutes.

This is only part of the revenue story. You can “buy” energy at negative rates but also get paid via the BM which is regulating the frequency of electricity at 50hz (it can’t go above or below 0.1hz variance). I’m writing this from memory so if I’m incorrect on the specifics here, please be kind.

This is yesterday’s UK Price Per MWH (2nd June)

PS: On Kate Morley’s web site (where I got the above graphs) is a very interesting puzzle. From GCHQ itself.

Can you solve the GCHQ Christmas Card 2023 Challenge?

If the answer is no, then here are the answers

Anyway, back to HEIT!

Volatility is good - why? Go and watch this TikTok where the boy cuts his price so his competitor cuts his even more - so the boy buys his competitor’s watermelons and then doubles his prices. His competitor can’t believe his eyes! But what a great entrepreneurship lesson! - I think they should show this video in every school. And to harrumphing shareholders who sell things at low prices then watch their shares revert.

The theory is fossils are expensive but offer base load. Nuclear is also expensive but offers further base load. Then renewables (except hydro) offer intermittent but cheap power (crucially a cheap marginal cost since there is no fuel) and less maintenance. Batteries, interconnectors and potentially hydrogen can help absorb the peaks and troughs. The recent reality is wholesale gas prices have been extremely low which limits the value of the peaks but also the cost of peaker plants peeking back in.

3. Bullish trend - Gas Prices

Will low gas prices continue reader? I am very sceptical that they can. Our forthcoming new government plans to put a knife to our North Sea operations which will leave the UK more dependent on LNG. All of that is positive for BESS.

UK Gas is 83p/therm which is $61/BOE - nearly 3/4 the price of oil. Henry Hub is $15.42/BOE. LNG is $66/BOE.

Over 18p/share of the reduction of NAV is down to LOW GAS PRICES

It is assumed by HEIT’s independent experts that £72/MW is all that’s achievable in 2024 rising to £73/MW next year. The dotted line reductions are seen later on as positive and negative adjustments to revenue assumptions “REV ASS” in my chart.

Notice too, that the £72 per MW assumption is £8 a MW below what HEIT say could have been achieved April (NB they actually achieved £68.70/MW for the quarter).

Let’s go back to the “Price Per MWH” chart for yesterday. HEIT could have sold electricity above £72/MW yesterday from 8pm until about midnight and then after about 7pm yesterday evening. In fact 8pm-10pm they would have earned well over £100/MW…. that’s on a warm, sunny, and breezy Sunday when there was plenty of renewable supply (less volatility).

I believe the “experts” are looking at 12 month charts like the one below and saying ah yes the average price per MWh is £72. But doesn’t that mask the variation within each 24 hour period? (the 2nd of June wasn’t unusual). BESS aren’t supplying 24 hours a day. They supply when it suits for 1 or 2 hours max. They buy/refill when it suits too.

The change to UK Zonal pricing announced by Ofgem is bullish for HEIT also. Most of HEIT’s assets lie in zone 2,3,4 and 6. It indicates a NPV increase of £12.1bn to wholesale costs, but major reductions of revenue in those zones for the cost of constraint management. Overall, that new pricing will feed into the future revenue assumptions in due course.

4.Long Term Demand for BESS

Regardless of current and indeed future gas prices, long term demand for electricity storage is there. Current installed base is 5199MWH (or 5.2GWH). The long-term demand for generation capacity is due to grow 2.8X to 3.7X between now and 2050 according to National Grid (3.7X is if we achieve net zero and 2.8X is the “fall short” scenario (which accompanying catastrophic rising CO2 levels, sea levels, and forecast temperature rises - yikes).

Correspondingly:

By 2030 National Grid forecast storage demand grows to 15GWH-36GWH (fall short vs on track) so triples or septuples.

By 2050 National Grid forecast storage demand grows to 33GWh-63GWh (fall short vs on track) so double again.

How will the UK grow its BESS if the profit model simply doesn’t work and BESS shareholders harrumph their money away? Any kind of long run revenue assumption carries an element of government intervention to ensure incentives for more BESS exist.

5.Energy Transition

Do you think the next government will push more for “on track”, reader? Or will it repeat the performance of the current one - to aim for “on track” (as the grim reality of climate impacts are felt, and its political will is tested) but then deliver a “fall short” policy (as the grim reality of cost and its political will is tested).

We also know Starmer plans to punish oil & gas with taxes. Will that help lower prices? Do increased costs generally lower prices?

£30bn of taxes per year is approximately what Labour’s National Energy plans could equate to according to the Cockney Rebel. We consume 45b litres of petrol and diesel each year. Further taxes on O&G which of course gets passed on to consumers, works out at 67p per litre extra if applied to Oil. Or on Gas about £1,250 per houshold (assuming we share that cost equally along UK households).

6.Divestment Strategy

I probably should have said this bit far sooner and this certainly isn’t the 6th largest factor influencing HEIT’s fortunes.

HEIT are actively exploring asset sales at prices well above 49.7% discount to NAV. This will be used to reduce gearing and initiate buy backs.

If history is anything to go by, assets are sold at a premium not a discount. For example HEIT divested the Rye Common shovel-ready project at a 1.5% premium to carrying value in 2023 (£13.65m received). It reports multiple indications of interest.

7. Reduce gearing

Whilst TopCo has no gearing at project level there was £95m at year end (31/10/23) and this grew to £130m in the 1Q24 update.

6.85% is the aggregate cost of debt 2024-2026. So on £130m is £8.9m or £2.225m a quarter. Each £10m of debt paid down reduces costs by £175k or 0.077p

8.Crazy Discount Rates

I consider the 10% DCF discount rate on assets operational for over 3 months quite harsh. You may feel it to be justified. It’s higher than its peers NESF 7%, JLEN 9.4% and double the National Grid’s own 5% rate. Either way, if you believe interest rates will fall in time then this discount will reduce.

9.Future Opportunities

I’ve not found any evidence that the forecast National Grid Energy System Operator ("National Grid ESO") planned process improvements and how NG intends to increase the utilisation of BESS in the Balancing Mechanism is factored into future pricing assumptions.

This is taken from the HEIT Q2 commentary:

independent market experts expect trading conditions to improve over the course of 2024. In particular, the continued enhancement of new systems and processes by National Grid ESO are expected to improve access to revenues via the BM. Indeed, positive results from this new system are already starting to be seen, although not yet on a consistent basis.

Longer-duration 2- hour batteries have continued to outperform shorter-duration BESS and the Company is very well placed to benefit from the expected increase in demand and supply on the power network, balancing challenges, widening wholesale market spreads, and greater BM volumes. Going forward, the key will be to continue with a strong focus on best-in-class equipment, highly skilled asset management and regular, active scrutiny of revenue optimisation performance.

10. HEIT’s claim for Damages - not in the price

This refers to 83.2MW of assets delayed by at least 3 months. At £80k/MW/Year rates 3 months equates to £1.6m of compensation.

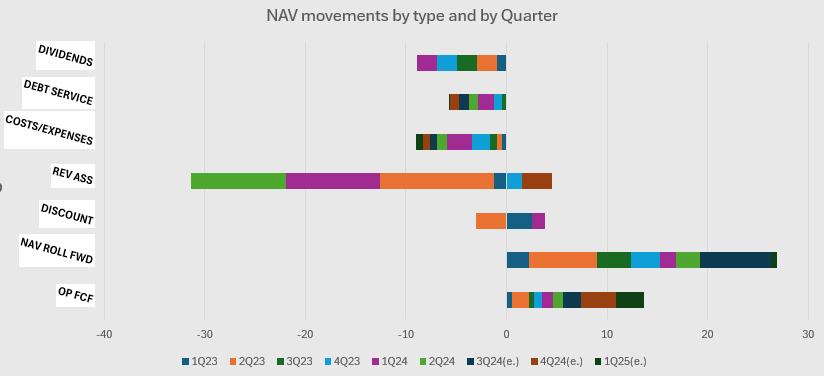

The Oak Bloke HEIT Financial Model

Everything in the chart below until 2Q24 is fact. I’ve simplified the headings a bit to lump stuff together.

3Q24 - 1Q25 is based on the following (I think) conservative assumptions.

An average £80k/MW is achieved for Op FCF going forwards. It’s already been proven to be achieveable. There are reasons why this is conservative and further upside is likely to the rate.

That Op free cash flow is used to pay down debt.

167MW of capacity becoming operational equates to 7p/share in the 3Q24 NAV roll fwd. We saw 6.83p rise in 2Q23 so again I think this is conservative.

That 3p/share Revenue Assumptions (again hugely conservative) to partially reverse the -18.7p reduction from earlier in FY24.

I assume the 98MW Pillswood asset sells post year end in 1Q25 (i.e in 4-6 months time). I assume it achieves a 1.5% premium to NAV. This would be £99.4m. This has the effect to reduce Op FCF by 20% (395.4MW reduces to 297.4MW) but £99.4m plus Op FCF 3Q24 to 1Q25 completely pays down 90% of project-level debt. The 1.5% premium I record to NAV as roll fwd and is £1.47m /0.65p.

Conclusion:

Even selling off 20% of the portfolio deleverages and paves the way for buy backs. A deeper than 20% sale, would hasten that. I know there’s talk of potentially someone bidding for the whole of its assets. I can certainly see why they would!!

80% of today’s operational assets deliver £4.46m/qtr less fund costs so deliver a baseline £11.5m earnings a year. Applying a (I think) conservative 15X gets you to £170m. Today’s market cap is just £110m reader.

Within a year the model sees NAV recovering to £1.11/share (£253m) and that assumes zero buy backs. So if HEIT gets taken out at NAV plus 10%, a £278m sale would be 2.5X today’s share price.

Whether HEIT continues forward as is or gets sold off at some sort of premium to today, or even at a discount to NAV, its current 48.8p is simply too cheap based on my analysis. I only wish I’d spotted its fall to 33p in Mid Feb. Well done if you did, reader. You’ve already made 50% and I reckon there’s more to come.

Regards,

The Oak Bloke.

Disclaimers:

This is not advice

In general, Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".

Re the frequency its 50Hz if it was MHz it would be a microwave!

Two years back it was ESO ancillary mkt that was driving up the sp as the ESO initially provided a high incentive to attract players into the mkt but once they moved the services onto an auction basis prices plummeted. So in some respects a false mkt was created by the ESO and we now have far too much BESS for amount of support ESO require (this changes daily/hourly and is largely linked to how high renewable penetration is so potentially in the future it could come back into its own). The ESO have also altered the algorithms that guide the system engineers to take least cost most effective actions to keep the grid balanced and that has certainly helped the balancing mechanism income stream. Latterly they have also allowed BESS to participate in balancing reserve and those with 2hr systems have benefitted from that although you can already see prices dropping away as more participants come on line (there are a lot of new assets being commissioned over next two years that will double installed capacity and much of it is 1.5-2hr rated). Finally the real money spinner now looks to trading in the wholesale mkt and yesterday it was certainly possibly to be paid to charge up in the afternoon and then sell it back higher mid evening (remember though round trip efficiency is c85-90% here). To do this means you have to find a seller then a buyer later on though (HEIT did this with Pillswood 1 yesterday looking at Elexon) but more BESS are adopting this trading strategy so this may lower spreads long term i suspect. What HEIT don't do, unlike GRID, is have some of their assets on PPA (power purchase agreement) which may give better long run income certainty looking at what they have reported.

Onto the income it certainly improved for Q1 but according to bessanalytics its fallen back a fair bit in May though so I would say 70k/MW/yr should be the stress test. Also you have to factor in this includes capacity mkt payments some of which are single year so will drop out from October although others also kick in. Still even at this level they are only just breaking even but as the new assets come on line later in the year is when they ought to move into having free cash flow to reinstate divi but not sure we will see north of 2p vice the 8p they were paying out. Thus sp still feels full to me and held up by a green premium but with so many new assets coming into this space the market is going to remain saturated for sometime to come.

Looks like there’s good demand at close to NAV prices for renewable assets.

https://www.proactiveinvestors.co.uk/companies/news/1067974/harmony-energy-income-trust-flags-191m-foresight-bid-approach-1067974.html

Harmony Energy Investment Trust just disclosed a firm offer price for their portfolio and shares jumped 22%. They already said they were negotiating the sale at prices close. to NAV in November 2024 when I bought in at 54p, and I was surprised that buyers let the stock hang around the 60-65p level while buyers were lined up.

Bit disappointed that the offer from Foresight is about 10% below the recent NAV from the end of February. If the board had faith in their valuation why would they sell at a discount?