DEC-ent Offer #2

Dear reader and ahoy to fellow DEC-hands,

In my article DEC-ent offer I spoke about the 105% of share price for a tender. A new tug of war ensued. Did the offer mean 69p or 5% more so 72.3p? Will the payout be $42m or $44m (assuming 100% tenders)?

Having pondered this I now believe my DEC-ent offer article could be incorrect.

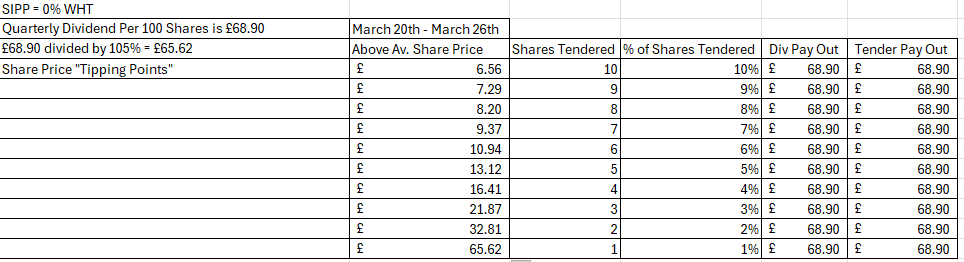

The 105% relates to what you give up not what you get.

For 100 shares £68.90 divided by 105% is £65.62. This is what you give up (in shares) to get £68.90.

In other words the “tipping points” for a 100 share shareholder between tendering 7 shares or 6 is actually £9.37. So in that scenario 7 x £9.37 is £65.59 and a shareholder who holds this in a SIPP, then you get £3.31 dividend 3.31p x 100) to receive £68.90. You now hold 93 shares.

The same SIPP person, if the average share price 20th-26th were £9.38 then 6 x £9.38 is £56.28 and then you get £12.62 dividend to receive £68.90. You now hold 94 shares.

The pay out is the same but the shares held decrease. No incentive.

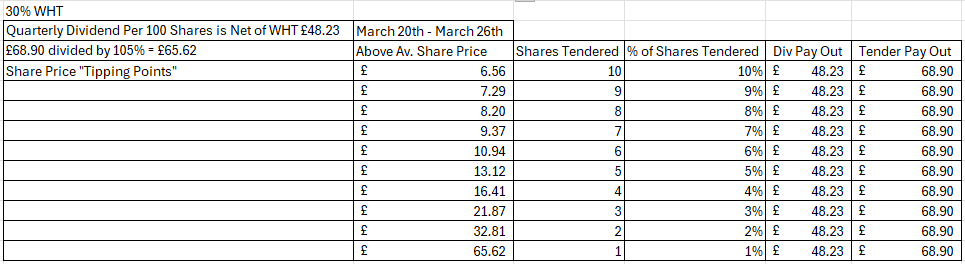

But if you aren’t a (UK) SIPP holder or haven’t - or can’t - register for a W-8 (which reduces the tax to 15%), or live in a country that doesn’t have such a tax treaty (that the UK has) or are an II (Institutional Investor) - they get lots of advantages but SIPPs are just for PIs! (Private Investors). For the tax payers the calculation is quite different. My web site visitor data suggests quite a number of DEC-hands come from across the rest of Europe for example.

In that scenario where you’re subject to 30% deduction, you are theoretically 20p a share better off or £20 over 100 shares taking the tender, which is a 42.8% higher return. (£68.9/48.23)

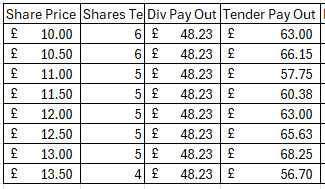

Now in practice the average price is unlikely to be perfectly any of these prices so let’s apply this model to a series of share price points in the grid below.

The first column is the theoretical average price 20th - 26th. If you’ve chosen 100% tender then on 100 shares this is the number of shares you sell. You don’t get a dividend for the remainder - you lose that.

But if you’ve chosen a partial tender, the Dividend Pay out is how much you’d have had via dividend (less 30%) also minus the amount tendered - so you get the full £68.90 minus 30% on the cash element payout.

So looking at row 1 Share Price £10 for example, we see 6 shares at 105% of £10 is £63. This is a £15.23 higher payout, but at the cost of losing 6 shares.

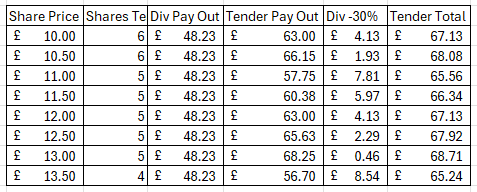

I originally thought the remainder was paid out but an eagle-eyed reader pointed out:

If the amount of Entitlement that has been waived does not result in an exact number of Shares at the Tender Price, such Entitlement amount will be correspondingly reduced to purchase the nearest whole number of Shares in the Tender Offer at the Tender Price and the remaining portion of such Entitlement shall be deemed to have been waived by the Qualifying Shareholder and will be retained by the Company.

So this offer is aimed at tax payers and those getting deductions. For shareholders in a SIPP should continue with dividends - because there’s no incentive to do otherwise.

And for UK ISA holders at 15% witheld even with a W-8, your gain is even more slight and will depend on the share price level, plus you forego the dividend and lose shares.

The model does point to - particularly - an incentive for IIs to get the price in the next few weeks to either £10.95 or £13.13, to take advantage of tipping points of tendering fewer shares.

And if this model is correct then it isn’t costing Dusty a cent over the $42m he was going to pay anyway. In fact due to rounding down it might cost a bit less.

“The aggregate amount of funds the Company will utilise in relation to the Return of Capital will be approximately US$42 million, which is the approximate amount of the Third Quarter Dividend announced on 15 November 2023.”

What Tender Offer would make sense to refuse dividends for a 30% taxpaying PI?

Mathematically receiving 105% of the market price is too low.

For each share the dividend foregone (68.9p) even reduced 30% by tax to 48.23p means surrendering shares doesn’t outweigh the loss of dividend.

On a £10 share, a tender price of £10.50, assuming 100 shares, tendering let’s me sell 6 shares per 100. So £68.90 dividend is 10 shares at £10.50 = £63.

I have £15.23 more cash. But have lost 6 x £10 shares. So net lost £60-£15.23 = £44.77

In fact as a 30% tax paying PI you'd need receive £63 + £44.77 = £107.77 to be properly compensated wouldn’t you?

So £107.77/6 tendered shares is £17.97 so your breakeven tender price (as a 30% tax payer) is 79.7% above £10, not 5% above.

What Tender Offer would make sense to refuse dividends for an II?

The mathematics are the same except perhaps the II is subject to further taxes such as Corporate tax so perhaps the dividends is reduced by a higher percentage.

Let’s assume 40% for the same of argument. So per 100 shares £68.90 reduces to £41.34.

So for a 10m shareholder (I know such an II doesn’t exist but it’s easier numbers to follow), the NET dividend would be £4.134m

At a tender price of £10.50, can tender 656,190 shares right? (£6.89m/10.5).

£6,889,995 received - so literally £5 below the GROSS. So receives £6,889,995 - £4,134,000 = £2,755,995 but surrendered 656,190 shares so received £4.20 per share. That’s a £10 - £4.2 = £5.8 x 656190 = £2,755,995 loss isn’t it?

But the difference for an II (assuming you hold many millions of shares) is that you cannot easily exit.

Selling 0.65m shares should probably crash the price. You have to issue an RNS that your percentage falls. In fact your £100m shareholding (10m x £10) only has to fall by anything over 2.755955% for that £2,755,995 loss on tendering to be cheaper overall.

So this is why the tender - as pointed out by others - is more suited to large IIs for this reason too.

Hope that helps!

Conclusion

DEC-ent on many levels - except perhaps for the US tax payer who’ll sting non-SIPP DEC-hands a bit less. Only 26 days and DEC-hands will be hauling in their March booty, and looking forward to another haul in June, and September and December.

And 17 days until a broadside is unleashed on Snowclaptap in the 2023 report.

This is not advice

Oak

Love what Rusty is doing but at the end of the day it appears to be small beer to PI’s and a lot of hassle if you’re a long term holder. Just take the divi. IMHO it’s designed for the II big boys. Some on the chat rooms don’t realise it’s just LSE. It would also appear from the tender offer these Buy Backs come under the current Buy Back programme and not over and above. Happier days but a long way to SP recovery

Hi O B.

In your DEC-imals and decibels' survey, 7% wanted buybacks. Presumably they'll all be waiving the dividend and tendering their shares. Time for another survey?