Feb Brew Wary Musing by the Oak Bloke

Gold and Silver - and a Tun of it

(I recorded a two part YouTube video on this Sunday 8th Feb 26)

Dear reader

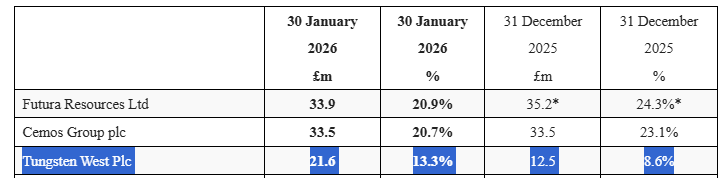

4th place 2024 and 2025 Fun Run Runner up Mr Thompson released his 2026 Bargain Shares last week, leaning heavily on successful ideas from his fellow fun runners it would seem…... You might spot some familiar names among the picks!

The usual bounce occurred on day one since Mr Thompson has hundreds of thousands of readers. 400,000 readers says the IC blurb. So about 100X the number of readers that the Oak Bloke now has.

BSRT

I say the usual boost. Not so for BSRT. I was surprised to see BSRT only increase by 10% on last Friday to 103p bid, considering it had the Bargain Shares boost…..

Considering, too, the same day it announced an 11.9% increase to its NAV per share at 30 January 2026 increase of 16.2p to 152.2p.

More to come? You can be sure of that. There was some vague numbers from Thompson and the brokers copy and paste of the RNS. I meanwhile rolled up my sleeves.

Tungsten West (TUN) updated its Definitive Feasibility Study based on $32.5k/t Tin and $40k/t Tungsten. This ignores actual prices are $48k/t Tin and $131k/t Tungsten. Eagle-eyed readers will remember the lesson from history (and a past OB article) where Tungsten prices shot up in world war one as tungsten supplies were torpedoed by submarines in the Atlantic and potentially a major reason why World War Two ended was a deal done with Spain’s Franco to block the Nazis to deny tungsten meant Tiger tanks were not as tough as they should have been through the restriction of tungsten supply.

Even at the $32.5k/$40k DFS prices of metals rate TUN is compelling:

o The Project’s forecast Net Present Value 7.5% (”NPV”) increases from US$190 million to US$1.7 billion

o The Project’s Internal Rate of Return (”IRR”) increases from 29% to 197%

o Near term EBITDA estimates increase over fourfold

It’s true that the value of TUN shot up as at 31/1/25 but is that the whole story? No.

TUN was 20p at 31/1/26 and 28.5p bid as at 6/2/26. So there’s a post period gain of 42.5% worth +£9.2m (worth +9p per BSRT share)….. Is THAT the whole story? No.

Let’s get into the numbers:

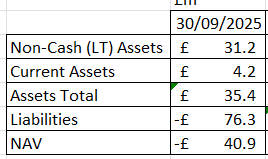

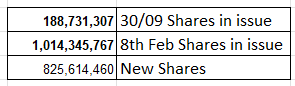

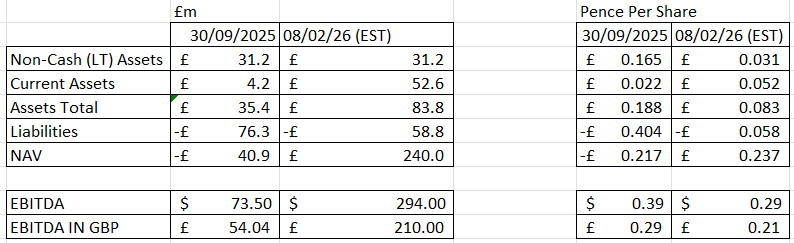

As at 30/09/25 BSRT’s interest in TUN was: 28,846,515 ordinary shares (was 15.4% of the shares in issue). It then had valued at £3.3 million a £1,200,000 convertible loan valued at £6.0 million, also 1,657,195 second options valued at £0.1 million and 1,657,195 third options valued at £0.06 million.

As I previously set out, those options and convertibles were worth a great deal.

But how much more? Thompson won’t tell you. Seems the broker doesn’t either. Nor would the balance sheet. A net liability value of minus £40.9m as at 30/09/25. Ouch.

But what of Historical Infrastructure?: Tungsten West acquired roughly $300 million worth of historical assets from the previous operator (Wolf Minerals) for just £5.4 million. However, for accounting purposes, these are depreciated based on their "Fair Value" at the time of acquisition plus any refurbishment costs.

There are $93m of refurbishment capex costs which will be met by a further up to $75m of debt. This is to provide a front-end crushing circuit and add five Tomra ore sorters. The Life of Mine is 40 years so depreciation is spread over a long life too.

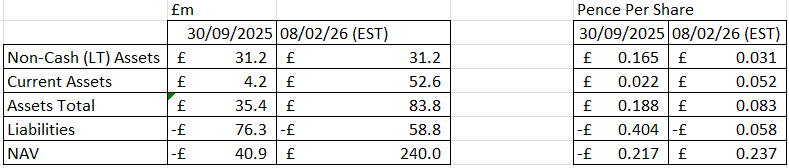

TUN has raised £48.4m of equity diluting the orange squash out of existing shareholders. Crucially, though the balance sheet has been substantially strengthened.

Each share has moved from being worth minus 21.7p are now worth 2.5p.

Why pay 29.5p for 2.5p?

Of course the $300m of equipment for £5m comment means there’s £215m hidden on the balance sheet. This means you’re paying 29.5p for a true book of 23.7p.

But the key point here is to also consider the ability of the assets to deliver income.

Now this is where it gets VERY exciting. A quadrupling of EBITDA was reported but no one seemed to twig what that meant. The Oak Bloke meanwhile had fallen off his chair…..

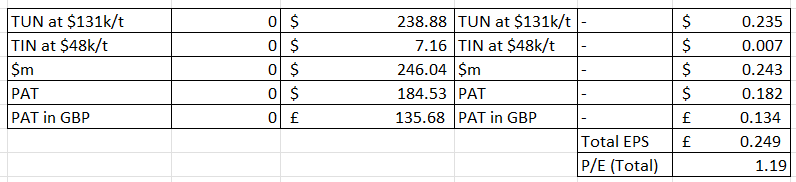

$294m was based on conservative prices and based on 50-trucks/day (more on that later), and equates to an EBITDA of 21p per share per year.

Bear in mind this is a refurb, with an EIA (environmental impact assessment), a DFS, an estimated ~£50m+ of cash and advanced options for debt funding.

Based on my estimates the DFS has “shrunk” from 13.9p per share per year of NET INCOME down to 11.5p per share per year but have a think for a moment.

Could a business with <£1m cash, and over £76m of debt actually get into production? Not without a BIT of dilution. The net effect of the dilution is ONLY 17%. That’s why I fell off my chair. 11.5p on a share that you can buy for 29.5p (and yes I totally appreciate that the share price has risen) but that’s a P/E of just over 2X.

But even that is not the end of it. I probably need a tiered floor right now as I’ve been floored by the ROI to then realise I need to factor in today’s prices. I had nowhere else to fall as I’d fallen once already.

Once I do factor today’s prices in (and I’ve assumed zero for last September when prices were lower) that at today’s prices TUN will be generating over double the forecast profit. The higher prices drop down to the bottom line (assuming 25% corporation tax and no write offs of capital allowances etc).

That puts this on a PE of 1.2X.

The 50 trucks a day - are they transporting truck loads of Tin and Tungsten. Barely. No, they are trucking aggregates. The final upside is the sale of aggregate which to be fair might not be making much more profit. But it is REDUCING COST. The trucked rock does not need to be stored in a tailings dam and thus saves cost. It would also provide some helpful early cashflow too.

There is an application to increase that to 300 trucks a day and Plympton’s Protestor community are objecting to that. But contrary to what some other commentators are saying TUN can NOT be shut down by protests. Increases to trucking movements curtailed possibly yes - thus increasing costs (but only to the costs set out in the DFS mind you). But shut down. NO. That ship has sailed.

TUN has even offered a “bribe” (or more formally, the Section 106 mitigation package) to secure those 300 truck movements is a central part of the current standoff.

TUN is essentially offering to rebuild and “future-proof” the local infrastructure in exchange for the extra traffic allowance. Here is the specific breakdown of the “Highway Improvement Package” they have put on the table:

1. Widening the “Loughter Mill Link”

Although the previous owner (Wolf Minerals) spent £7.5m on a new link road that opened in 2017, it has a major flaw: it’s too narrow.

The Problem: There are five “pinch points” where two 44-tonne HGVs cannot safely pass each other without hitting the verges.

The Offer: TUN has proposed to widen five specific stretches of the B3417 between Colebrook and the mine entrance. They claim they can achieve the required 6.5m width by utilising the existing verges, avoiding the need to tear down historic hedgerows—a major “olive branch” to the environmental objectors.

2. The “Active Travel” Sweeteners

To win over the Plympton Chaddlewood residents, TUN has added several “community” infrastructure items to the planning variation:

The New Bridleway: A commitment to provide a new, safe bridlepath between Stoggy Lane and Hemerdon Lane, specifically designed to separate horses and pedestrians from the increased HGV traffic.

B3417 Speed Reduction: In response to safety concerns, they have proposed a physical realignment of the West Park Hill junction to naturally “calm” traffic speeds as vehicles enter the residential zones of Plympton.

3. Operational “Self-Regulation”

TUN is also offering a strict “Code of Conduct” as part of the legal agreement:

“Left Turn Only” Rule: All HGVs exiting the mine would be legally required to turn left (away from the narrowest village lanes) with CCTV monitoring at the gate to ensure compliance.

Curfew: No aggregate movements on Sundays or Bank Holidays, and restricted hours (7am to 6pm) during the week to avoid waking residents.

Goldplat - GDP

I still think my Augustus Gloop picture exceeds the other pulication’s artwork of a weird picture of two blokes in flourescent jackets walking down a tunnel. Does Goldplat even have any tunnels?! I seriously doubt it. But hey I’m biased. I can’t really comment on the quality of the article as it’s behind a paywall, but I’d likely be biased on who wrote the better article too. I achieved nearly 100% share price result today laying down the gauntlet and future yardstick for my Fun Run ex-compadre.

Goldplat ticker GDP is up nearly 100% since I could see it was ripe in “Rising GDP” last June. Will it rise further now? Mr Thompson clearly believes so, drawing upon some broker guesses and speaking of the tailing dam without warning of the fact that GDP have to pay off the landowners involved, so I am told. I remain mildly positive about GDP but think much of the upside is already in the price and it pays no dividends (for now), so I’m going to call time at today’s 13p bid price. Let’s see if Mr Thompson achieves any upside from the ask price people will have been paying today from 8am of 13.5p. Mr Thompson only has a nearly 100% increase to beat. Let’s see how that goes.

ANIC

Mr T’s 2025 ideas contained ANIC, an OB 2024 idea, and that’s staged a recovery in the past week or so to arrive at 1.6% up in 2026. Gattaca has done well in 2026 too, but other 2025 ideas have failed to grow much or at all.

ANIC is at 6.5p ask and its biggest holding Liberation Bioindustries is worth 3.4p per share, so over 50% of today’s share price.

Lib has reached several major milestones in its mission to solve the global “fermentation gap.”:

1. Flagship Facility (Richmond, Indiana)

The company’s primary focus is completing its first commercial-scale, purpose-built precision fermentation plant.

Timeline: The facility is in the final stages of construction and is expected to begin production in early 2026.

Capacity: It features a 600,000-liter capacity with dedicated downstream processing (DSP), designed to produce bio-based proteins and ingredients for the food, pharma, and chemical industries.

Commercial Interest: The site is already a commercial success before opening; over 50% of its capacity was pre-sold or under late-stage contract as of Jan 2026.

2. Strategic Partnerships & Expansion

Liberation Bioindustries is expanding its footprint well beyond the U.S. Midwest:

Middle East Expansion: They have partnered with Topian (NEOM’s food company) to co-develop a major fermentation facility in Saudi Arabia. Planning for this site began in late 2025.

Anchor Customers: They signed a multi-year deal with the Dutch startup Vivici to produce Vivitein™ BLG, a nature-equivalent whey protein, at commercial volumes in the Indiana plant.

Government Backing: The company was selected for the U.S. Department of Defense’s DBIMP program, which may open doors for up to $100 million in additional funding for future facility expansions.

Financials: They successfully closed a Series A1 equity round in December 2025, led by Agronomics, bringing their total deployable capital to over $100 million.

ANIC recently kitchen sinked a lot of holdings in its year end report to 30/06/25 taking the NAV from 15.58p 20% down to 12.34p. Ouch!

But its holdings continue to progress and consolidation of companies is healthy. The NAV is a historical marker rather than a fair value and meanwhile the macro only grows stronger. The price (in £ and in opportunity cost) of growing animals continues to rise and the demand for protein outstrips supply. Then there’s the holdings that focus on ingredients too.

In today’s competitive world where availability of resources trump price then Agronomics holdings could easily become the next strategic. Could you bring a competitor to their knees through restricting rare earth metals - you could mess with their production a bit. But cut off their food supply?

Surrender within a few weeks. In today’s complex food chains could this become a future battleground? For Europe certainly it’s a yes. Fading memories of the Battle of the Atlantic, but it’s still within a lifetime that the UK faced that threat.

Today’s NAV update already shows a partial recovery of the NAV back to 13.78p per share (compared with the last statutory result to 30/06/25).

SILVER and SilverCorp

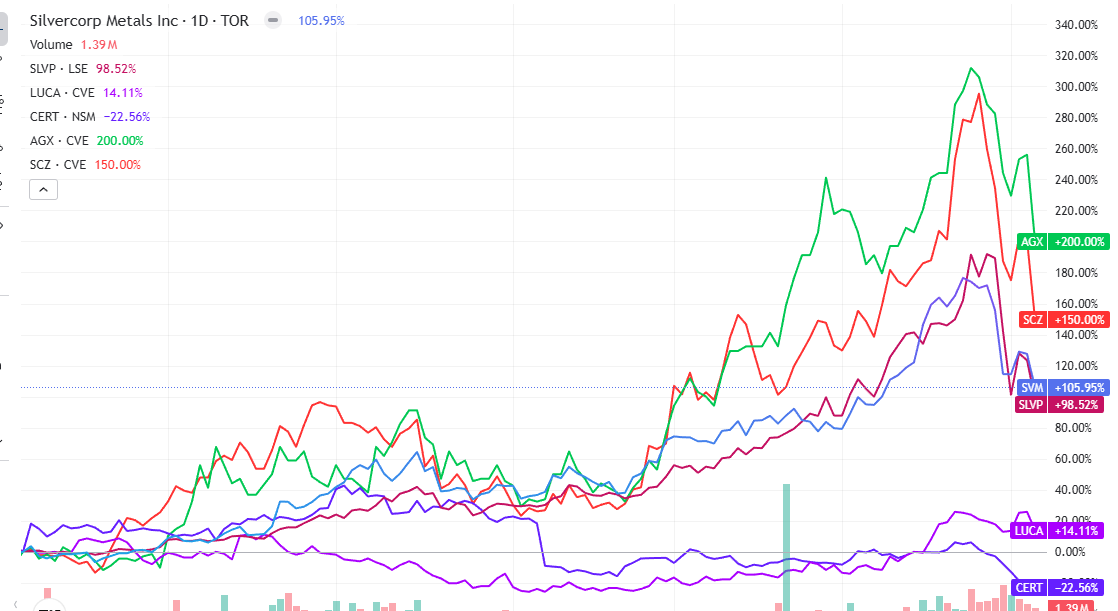

While the topique du semaine has been the volatile price of silver (and gold) this week, it is clear the market has not understood the degree of leverage the current silver price represents. Over 6 months since last August 2025, Silver has moved from $35 to $77.16 per ounce at the time of writing.

At roughly a -$22 to -$25 AISC, silver miner profits have grown from $10 per ounce to $52 per ounce correspondingly. That’s a 500% increase. Yet the most silver miners in my coverage universe have only increased by +200% (for Silver X). Even Silver X remains at a 40% discount to its NAV (0.6X NAV) since it has had quite a lot of operational struggles but a high silver price, high prices delivers profits even to the least profitable and struggles ease.

What is shocking is to see LUCA mining only up 14% in that period. Wait what?

LUCA produced 26,144 ounces of gold for 2025, within the guidance of 25,500 - 29,000 ounces. It produced 1.33-million ounces of silver, meeting the revised guidance of 1.18 million to 1.4 million ounces. Yet is only up 14% in 6 months. Really? I’ve added LUCA especially since it also has a decent amount of Copper, Zinc and Lead so is polymetallic as well as Gold/Silver.

OB pick for 26 Silver Corp (ticker SVM) meanwhile appears to be moving in lockstep with the price of silver. Moving at 100%. Not at 500%. For how long? What about the leverage effect of profits?

Perhaps next Monday evening (the 9th Feb) when the 3Q26 accounts are revealed although we already know revenue was $126.1m for the period to 31/12/25 which is an increase of 51% from 2Q26. Gross Profits will therefore double perhaps to ~$80m for the quarter meaning net income of perhaps $55m (so $220m annualised so a PE of ~10X). That’s well ahead of the forecast PE of 15X. Forecast earnings shall grow even further in the next two years.

SVM’s new mine El Condor, is on track timewise for late 2026, albeit with cost rises due to VAT changes in Ecuador and inflation. (-$40m impact)

SVM meanwhile has spent $162m this week (as you do) for two new projects in Kyrgzstan bought from Chaarat for fast tracking. Charaat has already spent $174M developing, drilling, metallurgy, technical studies and on site infrastructure. The Kyrgz govt get a 30% free carry - so they’re happy.

Meanwhile SVM shareholders will be happy too:

Tulkubash: permitted for construction and production. ~100-110 koz/yr gold for 3-4 years ($700m NPV 5% at $4,500 gold)

Kyzyltash: has a clear path for full permitting. ~ 190-230 koz/yr gold for 18 years ($2.5bn NPV 5% at $4,500 gold)

The payback will be a matter of months, and are forecast to come online late next year (2027).

Software

I wrote about HG Capital last week and it was interesting to see the range of responses. Some agreed, some disagreed with my view.

Does a world with AI mean more or less software? Is AI not software too? More or less human involvement? That is the thin end of the wedge. Does AI not mean faster and cheaper development? Does AI not mean software companies can deliver systems far faster than ever before, delivering increased value faster, and therefore more profits. I really think the marketing message from Anthropic is a storm in a tea cup. But in the interests of scientific discovery I have resolved to pay for an Antropic subscription and shall undertake an experiment to prove or disprove my theory.

I shall write more about this soon.

AI suffers hallucination. Can you trust it for mission-critical systems? Hallucination, contractual liability and mission-critical systems. Are we really saying those three aspects all in the same sentence?!

Recent Court judgments are that you implement AI in your business at your own risk.

The liability of AI actually reminds me of the 1992 Hoover US round trip flights give-a-way promo.

Let alone the reputational damage as the recent case of Deloitte and the Australian Government illustrated.

TURKEY TEETH

My Turkey ETF pick for 26 was met with quite a lot of disapproval by some readers. Yet the pick appears is proving to deliver exactly what I anticipated: An improving economy. Defence holdings at incredibly cheap valuation (half the price of Bae), an Airline stocks that is world class.

It’s delivering an 18% return so far in just over 1 month.

The Works

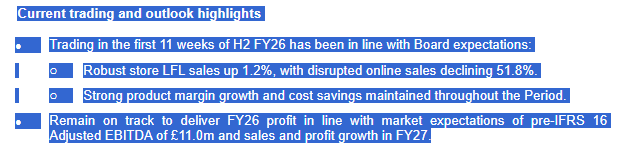

It was interesting to see Mr Rebel interviewed this week, including his view on the works. Crazy cheap. A PE of 3X. Market Cap of £18m so a net profit of £6m.

Yeah, no one believes the “E” (of the P/E) exclaimed Mr Hill.

Do you have to believe the E? Or do you just need to read their accounts?!

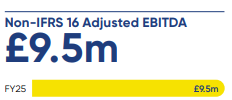

Last year the adjusted EBITDA was £9.5m. The net profit (excluding adjustments) was £4.4m

This year the Works remains on track to deliver £11m adjusted EBITDA. So £1.5m more.

We know finance costs are -£0.44m higher (in 1H26) but we also know the Operating loss was £1.85m less in 1H26 vs what it was in 1H25…. so that’s ALREADY £1.4m more overall net profit as at 1H26.

So you can disbelieve the E all you like, but when the result to mid January 2026 was on track (including the busy Christmas period) and the remaining 3.5 months to end of April are perhaps 10% of the remaining revenue, common sense should tell you it is now pretty difficult for this not to report a PE of 3X.

So this is a fish in the barrel opportunity, in my opinion, even if some “disbelieve the E”

Or at least that’s true on an underlying profit basis, where perhaps adjustments and exceptions could ruin the profit number. That’s the risk I’m taking but where I can still argue the underlying performance is what matters.

Meanwhile I notice there are a growing number of glowing positive reviews of people’s online experiences lending further hope that the disruption in online has settled down and improved post Christmas too.

Mr Hill spoke of WRKS a second time last week and after a call with the CEO Peck, appeared to have had a change of heart. So perhaps he is starting to disbelieve the people who disbelieve the E.

Although Mr Scott remains demure about WRKS speaking of it only achieving a one, two, three percent net margin and disbelieving it can ever achieve six percent (although no reason is offered for why it can’t). Mr Scott previously said he prefers MKS which has a …. 2.1% net margin in 2025 and in the past 10 years has never achieved a 4% or greater net margin. So I was left unclear of the logic of criticising WRKS because of its Net Margin percent.

MARS bars

Ongoing coverage of Marstons by Mr Rebel led me to buy a little bit of MARS last week. I’d been vowing to simplify and reduce my portfolio so adding another holding is a step backwards on that resolution. Oops.

It was purely opportunistic. I read Mr Rebel’s excellent review of MARS, and on its t/u saw the market dropped MARS by about 12%. I wanted in on the Bagnificent Seven, well at least in one of them.

Why? Well paying 60p for 125p of assets where those assets grew by 22p a share in 2025 might be one reason.

The packed sports calendar including the Winter Olympics, the Football World Cup and other events another. A P/E of 6.5x and a ex-Camelot “magician” running things another.

I failed thrice in simplifying actually: That’s beuse I also added HG Trust but also a third name added which is a…..

New PGM Idea

I’ve been adding into a new PGM idea too. I continue to like THS but felt I wanted to diversify to a 2nd PGM idea.

I didn’t pick Sylvania SLP, didn’t pick something dreadful like Eurasia Mining but it is UK listed and involves PGM mining, and isn’t Physical Platinum or similar. See if you can guess what it is. Bet you can’t.

I’ll cover it in a new article soon. I’m very excited because essentially it’s an overlooked area.

Ed Milli

With all the political stuff going on who knows how the chips will fall, but I’m soon revealing an idea that is my ultimate Ed Milli play.

Whoops that’s a 4th new stock added. Energy continues to be an important theme and preoccupation.

This idea is already in the money up over 60%. It seems like a no brainer given its strategic importance.

UK doom and boom

A few readers were deeply sceptical of my assertion made (for example in GRG) that the UK could see a further rebound in 2026.

Everywhere I look I see growing reasons to believe that narrative strengthens. My 2026 partial positioning out of the UK and into emerging markets was a sensible one but OB picks for 26 ideas like GRG that remains shorted at around 12% of stock appear ripe for a rebound as the doom gives way to boom, or at least to something less than doom. Office provider Regional REIT RGL should benefit too.

Plus new ideas covered today MARS (Marstons), WRKS (The Works), EZJ (EasyJet), WJG (Watkins Jones).

Then there are UK bank plays in the OB universe via AUGM (Augmentum), INOV (Schroder Innovation), CHRY (Chrysalis), MERC (Mercia), LINV (Lend Invest).

UK shop inflation is even a positive perhaps, since GRG increased its prices it appears others have also increased theirs.

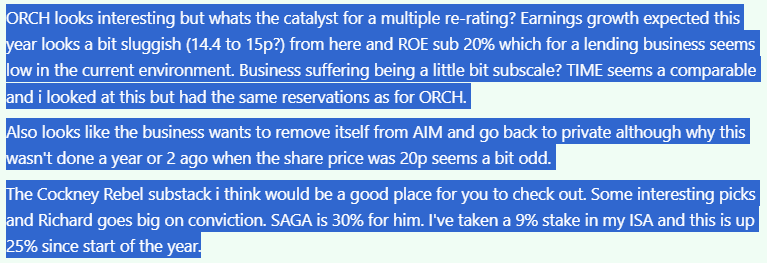

ORCH

It seems everywhere I look (including in my own comments section in the article Bubble’n’Squeak) I see Orchard Finance. It was one of Mr Jon’s 2025 ideas and an idea that he decided to keep open in 2026. So that alone makes me think I should take a closer look.

One reader’s comments:

Oil Be the Judge…..

US Crude inventories remain 3% below five year averages, and the US Strategic Petroleum Reserve remains at 58% of capacity.

Worldwide inventories are at 7.9bn barrels - a record - but this record amount is an accumulation by China. (1.5bn barrels + 0.17bn planned to be added in 2026). A further 0.3bn barrels sits in storage in Shadow Fleet vessels with Russian, Iranian or Venezualan crude.

If you strip out those two factors then the 6.1bn remaining worldwide is BELOW the 5 year average, and the OECD is in line.

Didn’t stop the IEA describing the level of stocks as SURGING though.

Wouldn’t the word SURGING better describe Oil demand? 700kb/d demand was forecast for 2025 and 2026 just 4 months ago. Two months later the outcome for 2025 was 850kb/d so over 20% more. The IEA 2026 forecast of demand has grown by over 30% in just three months from 700kb/d to 930kb/d. Just quietly included.

These monthly snapshot reports show a lack of even handedness - which creates an opportunity. Meanwhile certain commentators doggedly follow the headlines regurgitated from IEA headlines, even though those headlines are written by those who appear to have an agenda.

The IEA got supply wrong by -2.15mb/d in 2025. Oil Supply didn’t rise by 1.8mb/d as set out in Jan 2025 it fell -0.35mb/d instead, the the Jan 2026 report.

DEC

I’m excited to hear about the 4Q25 results at DEC. Forecast to deliver over $6 of EPS 2025-2027 for a share you can bought this week at ~$12.60.

That is forecast by aggregate broker guesses to deliver $5.87 FCF per share this year, $6.63 FCF/share in 2026 and $4.67 in 2027.

Yet again it’s under attack for its ARO. Yet again. Only DEC, just DEC. No other Oil or Gas producer has an ARO problem.

I believe the ARO liability is extremely well covered. Let’s roll out the maths. Again.

DEC has ~70,000 wells.

DEC has an agreement with the state of WV for ~23,000 wells at a cost of $70m plus the additional commitment to decommission at least 75 wells/year for the next 20 years = $3.5m + $2m of plugging costs = $5.5m/year for 20 years so $110m).

If the remaining states followed the same terms that implies a cost of $17.5m for 20 years or $350m.

Meanwhile DEC actually has far more set aside.... a $642m ARO liability set aside on the balance sheet for the net 47,000 wells it remains responsible for (which is a liability of $2.5bn discounted by 50 years)

Meanwhile in its latest accounts dated 30/06/25 DEC had $728m Equity + $642m ARO = $1.37bn of net assets to cover plugging, plus have PV-10 reserves valued at $5.8bn. (and that calculation takes no consideration that the future value of Oil & Gas is very likely to be much higher than today even after inflation).

Plus DEC has mineral rights over 2.3m acres of undeveloped leasehold acreage - which aren’t in the BS.

The PV-10 plus today’s net assets equates to $131,276 of assets discounted at 10% PER WELL. Perhaps you should deduct the PP&E element out of those assets but it doesn’t change the maths by all that much.

So undiscounted over 50 years discounted at NPV10 $131,276 equates to $662,019 PER WELL. This calculation ignores the value of any undeveloped leasehold.

The above calculation also ignores the fact that DEC has a plugging/decommissioning business. In the latest accounts its net costs per DEC well were -$14,371 per well NET.

For that calculation see the article: "DEC to June"

So $662k vs -$14.4k is a 4600% margin of safety. 46X ignoring land sales.

The issue is not a DEC-specific issue, and onshore the issue is 100X larger than DEC. It is very unfortunate that DEC continues to be targeted when it has its house in order.

Then for offshore O&G firms e.g. operating in the Gulf of Mexico the issue is larger again. DEC is well ahead of most of its peers e.g. that it has an inhouse plugging operation.

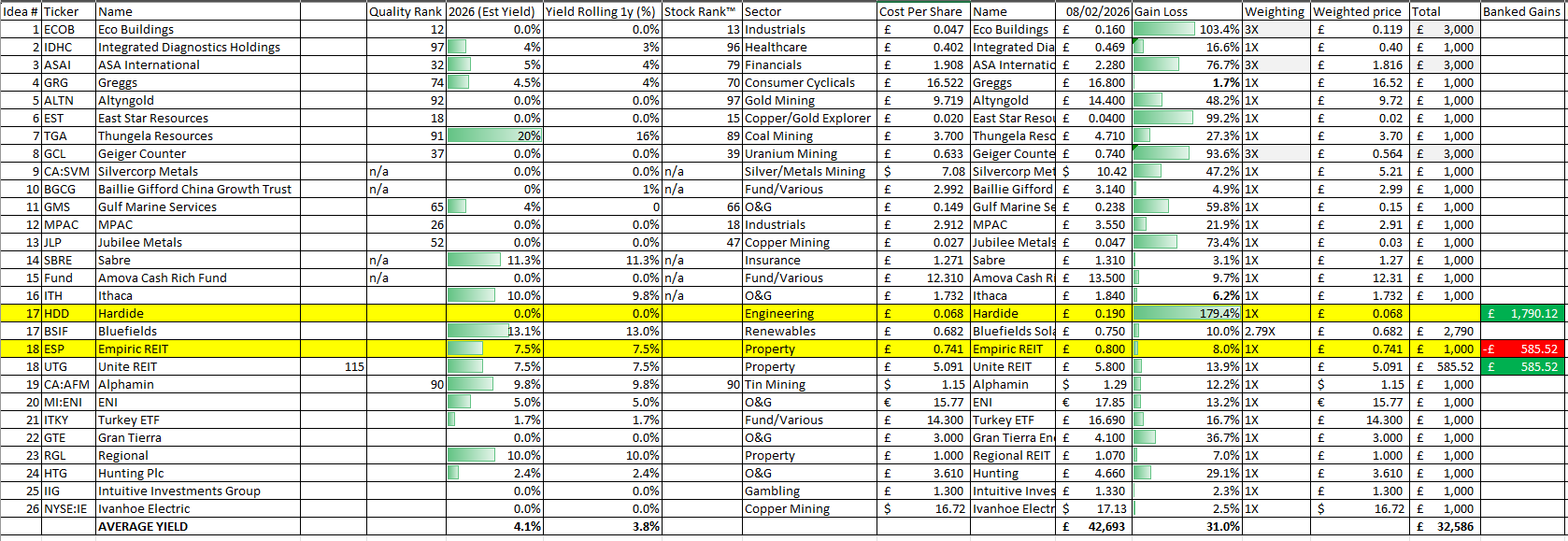

Unite and progress at the OB picks for 26

I closed my Empiric position due to the merger, banking an 8% gain, and expecting an imaginary £414.48 cash from Unite as well as 0.085 UTG shares. The 1,349 Empiric shares convert to 115 UTG shares which carry an imputed cost of £585.52 therefore a £5.09 per share cost price. This leaves me with a 13.9% gain.

I’ve not recorded the dividend but that’s on top.

Overall my picks for 26 are now at +31% which is an overall gain and considering the turbulence over the past week I feel that’s a stunning result.

Bitcoin

My concern about crypto in “Don’t Clown” and “Crypto Assets… and Liabilities” has played out pretty much as I forecast.

Do I still dislike Crypto?

Yes, yes and yes.

But I do respect Cathie Wood and this is her counter view.

1. The “Crypto Reset” and Volatility

Wood addresses the recent price swings in Bitcoin, framing them not as a failure of the asset, but as a “healthy reset” of the institutional landscape. She argues that the volatility is a byproduct of Bitcoin transitioning from a speculative retail asset to a core institutional “risk-off” reserve.

2. Bitcoin vs. Gold

A major theme in the video is her comparison of Bitcoin to gold. She notes that while gold has historically been the “flight to safety,” Bitcoin is increasingly acting as a digital alternative during periods of fiat currency debasement or regional banking instability. She views Bitcoin as a “hedge against monetary policy errors.”

3. The Institutional Angle

Wood highlights that the “narrative of anxiety” in the markets (driven by AI bubble fears and shifting software models) is actually driving institutional interest toward Bitcoin. She suggests that institutional allocators are looking for assets with “low correlation” to the traditional AI-heavy tech stack, and Bitcoin currently fits that profile better than many equity sectors.

4. Signal vs. Noise

She encourages investors to ignore the short-term price noise and focus on the on-chain metrics, which she claims remain robust. She cites the continued growth in long-term holder addresses as evidence that the “conviction layer” of the Bitcoin network is at an all-time high despite the headline volatility.

Of interest are the surprising allies Wood has. Both JP Morgan and Larry Fink of Black Rock are supportive of this narrative too.

One can’t help feel that this could be Turkeys voting for Christmas and their support might be due to having skin in the game. Mr Arby’s ETF choice IBIT has over 800,000 BTC in assets under management (worth $52bn) which is 3.8% of the 21m Bitcoins and receive a 0.25% per annum fee.

JPMorgan analysts made headlines last week by calling Bitcoin "more attractive than gold" with a long-term target of $266,000.

JPMorgan makes money by selling structured notes and derivatives linked to Bitcoin (often using BlackRock’s IBIT as the reference asset). For example, they recently launched a “leverage note” that gives investors 1.5x returns if Bitcoin hits targets by 2028. They collect high fees for “wrapping” Bitcoin into these complex products.

The Incentive: Their bullish research notes encourage trading. Since they run a massive trading desk and provide “clearing services” for institutional futures, they profit regardless of whether Bitcoin goes up or down, as long as there is volatility and volume.

Conclusion

So to conclude a very long article, there remains lots of opportunities in the market. Lots to feel excited about, as you make your own investment decisions.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Hi OB - sorry to clarify Mr Rebel hadn't commented on ORCH...i was just using his substack as a reference for share ideas.

In the interim the IC has also included ORCH in their recent small caps review "double your money"

Enjoyed the deep dive on Baker Steel. Now a buy back - absolutely flying.

Had a meeting with MARS late last year. Doing a lot of sensible things to segment the estate and improve margins, but it is generally in an area which depends on U.K. consumer spending, which I prefer not to rely on.

Does anyone believe that the shares are worth anywhere near NAV of 125p. The sellside seems not to - Panmure who have strong analytical experience in pubs give it 80p. There is of course a gigantic debt pile here £1.5bn (IFRS included) (from memory) and 5.5x debt/ebitda. So, it’s all about debt reduction for a good while ahead, and no divs anytime soon.

On the debt, a lot of it is securitised, running to 2035. I didn’t look at the detailed terms but it is normally extremely difficult to refi securitised except at high cost.

So it seems to me that it’s a well managed company operating within a tight debt straitjacket, and shareholder returns not a priority. Can’t see a reason to hold something like this.