A net of 0p for 21.2p of cash and 188.4p of holdings

ESO is EPIC!

Dear reader,

Noting today’s trading update from LUCE and how it has breezed past its target price of 170p (187.2p/189.8p bid/ask as at 06/06/24) I re-ran my slide rule across ESO and promptly topped up.

ESO is at a more than 100% discount to NAV after deducting its listed holding (Luceco) and last reported Cash.

Anyone who read and followed this idea just 9 weeks ago on the 29th March would have already made 15% but you’d be certifiable to sell out today, in my opinion.

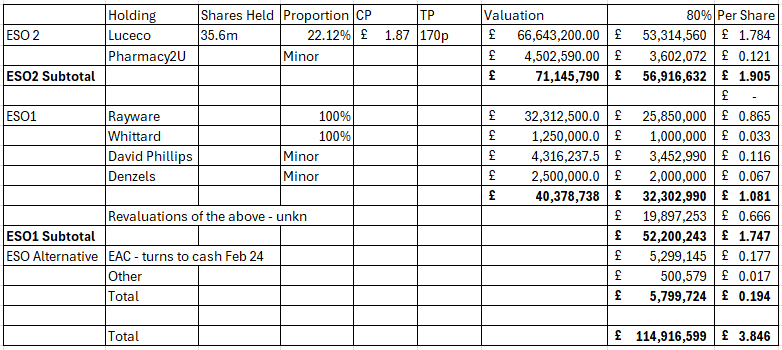

I’d refer you back to my article below - but the quick version is the free stuff comprises a share in a Repeat Prescriptions business which just swallowed up Lloyds Pharmacy Direct, classic Whittards of Chelsea with strong overseas sales, Rayware (including the iconic Viners Cutlery) the same, construction business David Phillips, and Denzel’s Dog Food make up a free £1.87 per share plus 5p cash per share for your trouble.

Growing businesses and holdings that I estimate are generating something like £4m - £8m a year profits which means 7.5p - 15p a share income and potentially dividends. (Course those are “free” also)

Incredible really.

Is it ESE to find hidden value?

Dear reader EPIC or EPE or ticker ESO is the Oak Bloke latest idea in hidden value.Thanks for reading The Oak Bloke’s Substack! Subscribe for free to receive new posts and support my work. A £1.50 buy and a NAV of £3.24 as at 31/1/24. But how real is that NAV?

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings even those held in Investment Trusts might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

ESO has risen since I wrote this article 5 days ago, but its Luceco holding has risen too and is now worth £1.74 per ESO share so that plus ESO cash (19p) is £1.93, versus a £1.87 buy price. So it's now 6p back not 19p + £1.87 of stuff but still mispriced!