AUGM-mmm are we missing some millions?

AUGM-mmm are we missing some millions?

Progress at AUGM isn't in the price - Part of the OB Top 20

Dear reader,

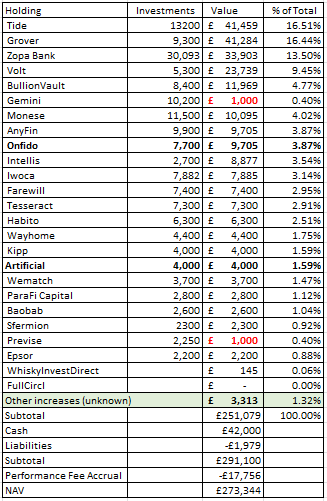

In my last AUGM article an augm-onth we spoke about Onfido. Onfido is up for sale with US leader Entrust. $650m is the valuation an insider said in confidence according to Reuters.

Now that’s interesting. AUGM invested £4m in Onfido and subsequent a Series D funding round raised that to £9.7m that was on a $242m valuation.

A $650m valuation puts the holding in Onfido worth £26m so a £16.3m increase.

Eagle-eyed readers will spot too a couple of other things. First that cash according to AUGM’s December newsletter is £42m and post period (i.e. in FY2024) shares in issue have dropped by 1.7m… due to buy backs - that’s 1% of all shares.

This means if Onfido goes through, and based on the newsletter, and the buybacks the portfolio picture changes…. from this:

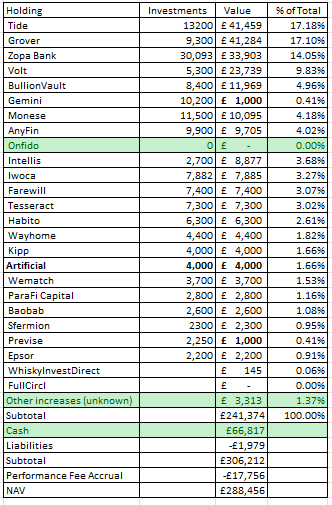

To this:

The effect is quite dramatic:

This shows that the pre-Onfido discount is 38% based on today’s £1.02 price. On assets like Onfido which may sell for a 168% premium. (Bearing in mind too other AUGM assets also sold at a premium)

Also that post period considering buy backs, and the Onfido deal that discount rises to 41% and NAV/share increases to £1.70 per share.

Of course let buy backs continue if the share price meanders on at about £1 a share. Long may it continue. Should it do so until £66.8m cash has been used for buy backs we see NAV per share rises to £2.15 (assuming 66.8m shares bought back leaving 103.2m)

Somehow I think that’s wishful thinking and the hidden value will be sussed out before.

This is not advice.

Oak.