In my article Introducing Augmentum Fintech we dug into 4 of the 24 holdings, Tide Bank, Grover, Zopa Bank and Volt. The top 4. It made sense to start there. They represent 57% of the NAV. And if after reading about those holdings you don’t get just a little bit excited, especially by Volt, well I don’t know what to say.

In fact, following this week’s news about Onfido, one share of AUGM at today’s price of 96.8p buys you Tide/Grover/Volt worth 62p and 33.6p of cash (including Onfido at an assumed £10m sale price).

So you’re short by 1.2p but you are getting 63.7p worth of 21 other holdings including Zopa, Whisky Direct, Bullion Vault…. or if you bought the lot it’d cost a net £2m for £109.4m worth of holdings. That’s not bad!

So this week comes 2 items of news from AUGM:

1.Artificial

First is the investment into a new holding called “Artificial Labs”.

Artificial is active in the large market of commercial insurance, with a focus on specialty risk — insurance made for businesses that need bespoke coverage. These policies may involve high-risk holdings that are not usually covered under standard business insurance policies due to their size, complexity, or risk profile. Like sailing up or down the Red Sea perhaps?

Specialty risks are placed in hubs with global coverage and expertise. Sourcing more than $91B in insurance premiums annually — of which $60B is within none other than Lloyd’s of London — the London Insurance Market (“LIM”) is the largest international hub for specialty insurance.

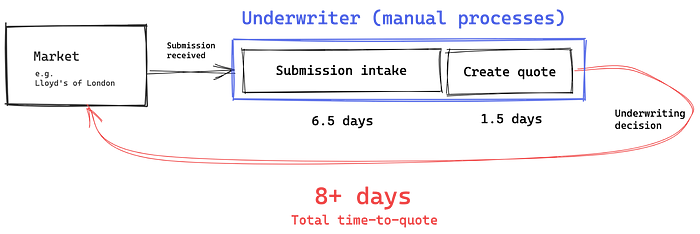

There is inherent complexity and the intermediated nature of commercial insurance has caused technology investment to lag behind other sectors, leading to higher costs and a negative impact on margin across the value chain.

“… the technology landscape in many commercial insurers remains hindered by legacy systems. Based on McKinsey’s observations, anywhere from 30 to 40 percent of underwriting’s time is spent on administrative tasks, such as rekeying data or manually executing analyses.”

Via McKinsey — read the full article here

Ouch!

Brokers and underwriters in the London Market continue to rely on manual assessment of risk, engaging in lengthy multi-party negotiation processes. As a result, it can take 8+ days for a broker to receive an underwriting decision.

Double Ouch!

Putting this into perspective versus the size of the market, infrastructure software in this space has great potential to improve efficiencies and optimise cost.

Within the London Market, instead of having one insurer carry the risk, complex policies tend to be distributed amongst multiple insurers with one lead insurer who sets the price, and multiple follower insurers who participate at the same terms.

This allows insurers to underwrite large, unusual risks without facing over-exposure on a single risk in the event of default.

The opportunity for digitisation is strikingly apparent in this “follow” market, where follow underwriters do not set the price, but instead “follow” into the risk. The nature of these dynamics lend themselves to a more streamlined process that should take minutes rather than days.

This is where algorithmic underwriting for smart follow comes in; underwriters program algorithms powered by multiple data sources to determine if a risk fits within the parameters of their risk appetite and responding in a matter of minutes when solicited. This compresses the time to quote significantly — a step change in the underwriting process.

Artificial is making waves in the Lloyd’s of London market

Enter Artificial, who are redefining how the insurance industry intelligently and efficiently deploys capital into the market. Over the past years, the team has built a core infrastructure software, making the entire process from data ingestion through to underwriting more efficient. Their software sits at the core of the insurance stack of the future, allowing parties across the value chain to benefit from their solution in two key ways:

1. Artificial works with brokers streamlining the creation and processing of insurance contracts with their Contract Builder product.e.g. Lockton partners with Artificial in the UK to implement new digital contract builder — via Artificial here

2. Artificial also enables any insurer to set up an algorithmic underwriting program; rather than brokers going through the time-consuming process of searching for follow capacity and speaking to multiple individual underwriters, they send details of a specific risk to syndicates using the Artificial platform and receive instantaneous offers to follow the risk if it fits the underwriters’ predetermined appetite. e.g. Apollo and Artificial Labs announce Smart Follow collaboration — via Artificial here

With established partnerships throughout the value chain, Artificial’s system enables end-to-end data flows, limitless integrations, policy management and contract building tools — all within one automated underwriting platform. These act as the central cog in the value chain, connecting data between brokers, underwriters and the marketplace.

Digitisation is top of mind for the C-suite of all insurers, driven by a combination of the following four areas:

pressure on costs

increasing number of disparate data sources

toughening regulation mandating new standards around digitisation (Market Reform Contract and Core Data Record)

the advent of new market entrants

AUGM believe that the era of algorithmic underwriting will redefine market dynamics in the insurance space. I think they may be on to something.

As more sophisticated ‘smart follow’ underwriters enter the London Market, we will see a significant transformation in the process of underwriting risk. The most adept lead underwriters, equipped with substantial auto-follow capacity, are poised to become highly sought-after by brokers seeking to place business.

“As this unfolds, carriers may have to weigh up whether not adopting certain tools in the underwriting process leaves them at risk of being outperformed, particularly on expense ratios, which would seem the likely area where benefits will be made.”

Via Insurance Insider — read the full article here

Artificial’s momentum is impressive working with some of the largest insurance organisations in the world to capitalise on the tailwinds behind algorithmic underwriting and the broader digitisation of the insurance industry.

In Artificial AUGM see a company that has innovation and tech at its very core — a company that has the potential to become a hyper scalable business with a truly unique proposition.

2. Onfido - prospective sale

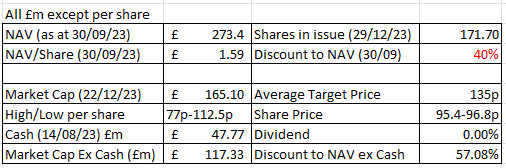

Second is the prospective sale of Onfido “at or slightly above its last fair value”. Now that might not sound very attractive but is that a question of perspective? Onfido is sitting on a nearly 2.5X ROIC (in 6 years), bought at £4m and fair value of £9.7m. What would £10m of cash mean to AUGM?

Well, AUGM is pretty prudent and cash rich already. What I mean by that is nearly 1/3 of the market cap is covered by cash. As can be seen once you strip out cash then the assets are at an astonishing 57% discount - even though this is the 6th time there is a profitable exit at or above that discount level! In fact with an extra £10m cash that discount grows to 60%!

Onfido provides identity verification services to enterprise clients in financial services. These clients have proven to be a resilient base, although rates of customer onboarding have reduced since peaks seen in 2021, with some verticals hit harder than others. Onfido has a leading position in the US and Europe through diversification across the financial services sector, and entry into new areas including healthcare.

3.Bullion

BullionVault has enjoyed a strong year of trading and is on track to deliver record profits. Performance follows from investor demand for gold and other precious metals as an inflationary hedge, and net interest income earned on fiat balances held by users on exchange. BullionVault is a mature position in the portfolio and serves a hedging function within the Augmentum portfolio during times of heightened market uncertainty.

4.Monese

Banking-as-a-service remains an interesting proposition and Monese’s B2B coreless banking platform ‘XYB’ has proven competitive amongst a strong peer set. The opportunity is clear; having tried and failed to launch internally-built digital propositions, incumbent financial services firms are seeking partnership with fintech players. Monese’s client list, includes HSBC and Investec. As Monese ’s revenue mix is increasingly built on long-term licensing revenues from XYB, the valuation comparables of the company will adjust. Our downward adjustment to the fair value of our holding by £1.6 million reflects the basket of public market comparators we have used.

5.Iwoca

Iwoca is an SME lender.

Three items of note. For all the negative news you constantly hear it’s good to hear 436,000 UK businesses were created in the first 6 months of 2023!

Second that in October Iwoca has secured a new debt facility with initial commitments of £200 million (and total commitments of £850m) from Barclays Bank plc and Värde Partners to meet the growing SME demand for working capital.

Third, Iwoca has been net profitable for the fourth consecutive quarter.

6.Penultimate Thought

One factor I believe that’s affecting PE and VC generally is the pension industry.

This recent article from Bloomberg suggests we will see a splurge of PE holdings being dumped on the market in 2024 at whatever price in the coming months since pension providers have met their objectives for their DB pensions. Although it seems this isn’t actually new news. The same story has been circulating going back in last year e.g. here.

Fantastic, I say bring it on. Why? I know a holding called AUGM which will gladly and selectively buy those assets at a haircut. It holds £50m maybe soon £60m cash. AUGM can afford to bide its time, grow its holdings, and it can also be highly selective in what it buys - and at what price.

The value of the sales of a business is ultimately the value to the acquirer, or in the case of an IPO the value the market assigns. Disruptive businesses that use technology to reinvent business models - as Interactive Investor did for private investors - are worth a great deal to lumbering incumbents - ABRDN for ii and Natwest for Cushon.

7. Conclusion

With holdings growing strongly, funded to profitability and an average 29 months runway, AUGM is in a far stronger position than its share price suggests. Let alone that AUGM holds nearly £50m cash.

Digging into more of AUGM’s holdings, we find more disruptive fintechs able to grow and grow. Potentially worth a great deal to the right buyer. Others ripe for an IPO in 2024. As Onfido demonstrates.

AUGM is part of the Oak Bloke Top 20 provided for your entertainment and interest.

This is not advice.

Oak.

Nice update