AVCT - Avacta Avacta cash burn factor

AVCT - Avacta Avacta cash burn factor

The investment case for AVCT March 2024

Dear reader

I read with interest this week an “absolutely sickened” Twitter post from the de facto champion of Avacta, Miles of Aim Chaos - whose Avacta thesis is at this link. He spoke to his dismay and disappointment. His followers were speaking of betrayal. Off with the head (of Avacta). Sack ‘im! The natives are restless, and the natives get to vote on March 17th. Why?

Avacta has raised £25.7m at 50p, after Avacta was “comfortably above £1” in recent times. Ouch. This, on top, of existing cash resources of £16.6m as the start of the year.

Quite a bit of collateral damage. Ironic, when the very purpose of Avacta’s pre|CISION platform is to limit collateral damage (of nasty chemotherapy). The bull case here, reader, if you aren’t aware, is that Avacta have a potential blockbuster (I’ll have an A please Bob, then a V,A,C,T,A for a gold run). Meanwhile the bear case - cash burner - led the pagan Shorters to dance with glee, chortle, hoot and holler “told you so”. And the bulls wept, and blamed the CEO.

Let’s go back a step.

Cancer.

Kills lots of people. Ancient Oaks in the Oak Bloke’s forest among them. A great oak still living is currently terminal. Sad. Angry. Cancer makes most people pretty angry, this writer included. So what fights cancer? Lots of things actually, but there’s two problems. Number one the strength of those things vs cancer. (T Cells, Immune Response). See my article on NSCI for a way to play method 1 - whose NASDAQ holding in PDS has shot up 50% in a month… is that significant? (I don’t know which is why I ask).

Number two collateral damage. That’s where Avacta comes in. Chemo drugs like Doxorubicin have been around for donkeys, but you can’t give too much. Heart damage, alopecia (yes it’s not the cancer that makes cancer patients lose their hair), tissue damage all kick in. You destroy the hamas but take out more and more civilians, so at some point you have to stop. The hope is you kill enough hamas that they don’t return or that you at least delay the next terror attack for a good few years.

But imagine you could shield the civilians. Precision strike the hamas bogey but leave the civvies intact. Avacta appears to substantially do that. Dozens of (very ill) Phase 1 trial participants have had the equivalent of a Big Boy bomb drop on their cancer and only one had a Grade 4 (i.e. dangerous) reaction. Many were Grade 1 and 2, so the equivalent of grazed and bruised perhaps lots of dust in their hair, but largely unharmed.

That is massive.

Apart from the part of me which wants to invest “to do good”, the other part says is it worth the risk? Is this time different?

As the share price dropped towards a tempting 50p is that an overreaction? If Avacta has over 2 years runway, can it take off in 2026? Read on reader, read on!

I do not attempt to replicate the original business case here - go and read something like Aim Chaos for that. But I hope to provide a 2024 fresh eyes perspective today.

Perhaps what should an investor consider to do next.

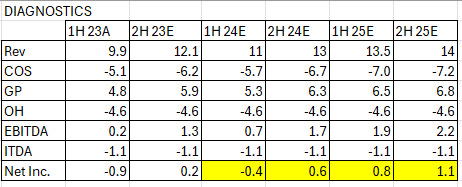

Diagnostics

Avacta has 2 divisions diagnostics and therapeutics. So for Diagnostics we learn forecast revenue FY23 of £22m and FY24 of £24m. We know H1’s numbers so I’ve pieced together the rest. I use a constant COS percentage, static overheads (OH), and depreciation/amortisation. We know in 2H 24 it’s forecast to turn EBITDA positive and cash generative in FY25. Assuming a gentle increase of revenue in FY25

From a cash burn point of view we see a net neutral cash position to 2026 (remember DA in EBITDA are non cash and I is around -£0.3m). That’s a positive start isn’t it?

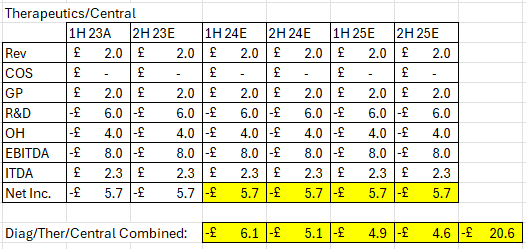

Therapeutics

Avacta, in 2018, secured the global exclusive license to a patented technology invented at Tufts University School of Medicine, Massachusetts, US. Reranded pre|CISION it is a way to keep chemotherapy inert until it encounters “a high expression of fibroblast activation protein”.

So reduces their side effects. This means higher doses can be given. In Phase 1a higher and higher and higher doses were given. After the 6th dose escalation it didn’t appear to have a maximum tolerable limit. It’s early days but the somewhat circumstantial evidence is compelling. Make the bombs as big as you like.

Compelling enough that Oncologists like Dr Christina Coughlin joined Avacta.

Let’s proceed to the numbers….

We know that Cash was £26m 30/06/23 and £16.6m 31/12/23. We know that Convertible Bonds were £44.6m 30/06/23 and £40.8m 31/12/23. We do not know the full year end results. So my NAV takes June plus/minus these known changes to arrive at £63.9m.

So shareholders now have 20.2p NAV/share so 11.5p a share more cash than before (NAV prior was 8.7p).

Cash Burn

The convertible bond issued in October 2022 is repayable in 20 quarterly amortisation repayments, of principal and interest over the five-year term, in either cash or in new ordinary shares at AVCT's option. On the basis further share issues would make natives even more restless and in keeping with the RNS which says “enough cash until the end of 2025” I assume AVCT pays the debt/interest down by £11m a year.

So half the cash gets ear marked there straight away, leaving a projected £20m cash. Projected cash burn of £20.6m in my forecast below more or less gets us to the end of 2025 - per the RNS.

I’m holding numbers static from prior periods projecting forwards. The ITDA component is £2.9m tax rebate and £0.6m depreciation which of course is non cash but I’m assuming replacement capital expenditure equals this.

Upside?

Half of cash burn is paying down debt. So a NAV of £43m remains at the end of 2025 plus the value from the Phase 2 and the Value of the diagnostics business. On a PE of 15 of forecast FY25 earnings the diagnostics business could be worth £30m+. Selling that would get Avacta to debt free and a further 1-2 years runway to 2027.

An investor has to consider the chances of a “take out” event in the next 21 months. I spoke recently about how biotech is heating up in my article IPO for IPO and in IP and Arix how $150bn of acquirable Biotechs have been taken out and Bristol and Merck face patent cliffs.

Negotiating with Phase 2 results is completely different to Phase 1a.

Raising a further bond with Phase 2 results is completely different too. Another £55m debt raise (if that’s possible) probably takes the business through to cash profitability.

Or issue shares in place of cash repayment. Further dilution but a longer runway.

Is £2m therapeutics revenue per half-year period too low? If the revenue were £5m+ (like in 1H22) then that extends the runway by 1 year.

Diagnostics revenue growing just £0.5m per period in FY25 may be too low?

What about revenue streams from Point by the end of 2025 when there’s been over 4 years development since 2021?

What’s the POINT?

Avacta have licenced Point Bio, who is now part of Eli Lilly, specifically for the microenvironment targeting of radionucleotides. Avacta will receive development milestone payments for the first radiopharmaceutical FAP-activated drug totalling US$9.5 million. Avacta will also receive milestone payments for subsequent radiopharmaceutical FAP-activated drugs of up to US$8 million each.

The problem is we don’t know the timing - and the timing is confidential.

But royalties and milestone payments could potentially extend the runway by 6-9 months, maybe more.

It also make Eli Lilly a prime candidate to buy out Avacta because they’ll be able to see 1st hand how well it works.

Market Opportunity

If pre|CISION™ technology is proven with Doxorubicin next gen precision therapies are estimated at $98bn by 2030. Meanwhile according to Statista Oncology drug sales were $176bn in 2021 and forecast to grow to $320bn by 2026.

AVA6000 is one form of treatment for one form of cancer. Another candidate AVA3396 treats multiple myeloma and mantle cell lymphoma which I read is $2.8bn opportunity.

What is AVCT, a $0.2bn company, worth if it could take a good chunk of that $400bn+ market? 100 times? With 20% dilution for existing s/h’s it’s now “only” 80 times? 80 times of something and not 100 times of nothing.

Conclusion

Should the natives be restless? The natives should have realised that cash levels meant this HAD to happen. Cash is cash. Burn is burn. 20% dilution is painful but the runway is essential. This investor realises there might be another burn in 21 months when another fund raise is done. But the prospective upside meanwhile, and the reasons for optimism made me jump to buy at 51.9p. I like the odds.

And I’d love for AVCT to make a step change in treating cancer. I sincerely hope it does. And I hope the natives come to realise talk of sacking the CEO is counter productive and as pointless as Canute commanding the tide. How can you remain the share price remain “Comfortably above £1” without cash and with cash burn?

On Thursday I said for every harrumph there is a hooray. This is just another example.

This is not advice

Oak

Interesting write up. I very much liked the Hamas analogy .. a very good way of describing what is trying to be achieved