Calling time on ECOB

Dear reader

It is with some sadness to call time on Eco Buildings. The full year results are out and the numbers have spoken.

Revenue is up, but only by €1m. Operating profit for GFRG drops to 25%. No reason given why, and the thesis was this delivers 40%. But then didn’t.

The marble segment meanwhile continues to make losses. Also the Head Office segment is really 90% GFRG and 10% marble (based on revenue). Once you include that we are no longer speaking of any operating profit really are we?

Could 2026 deliver a turnaround performance for ECOB? Well improvement certainly, based on newsflow but will it be enough?

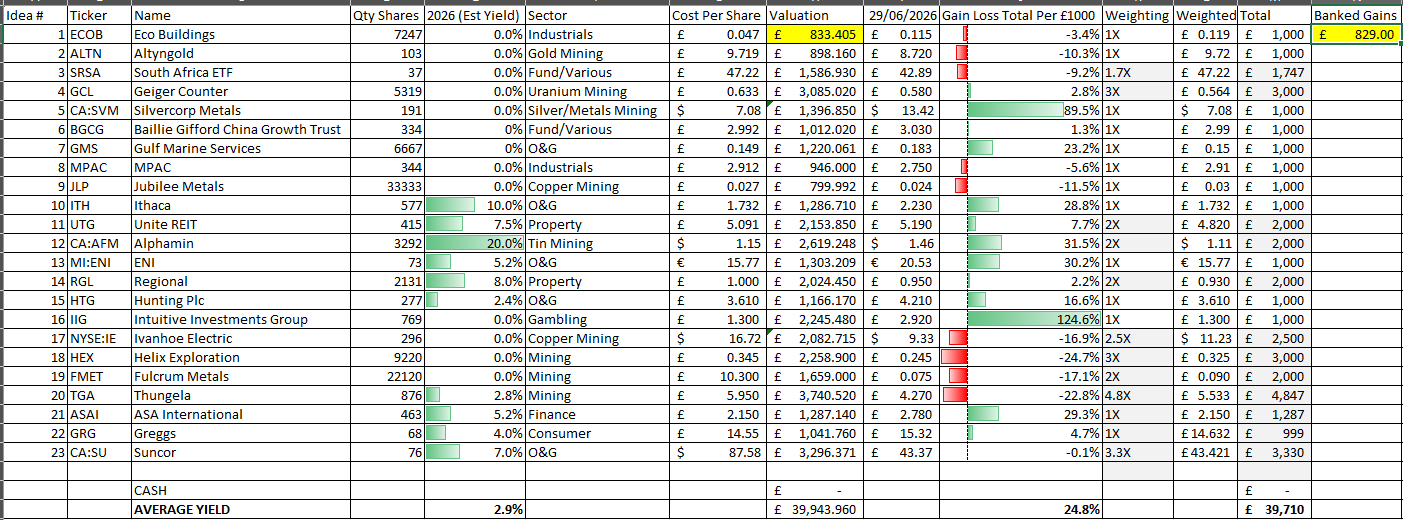

I’ve decided to exit at more or less the average buy price in the picks for 26 (given I averaged up to the original 4p) and best wishes to those who continue to hold but this one is no longer for me.

ECOB state a going concern basis is appropriate but the auditor disagrees. The question of CLN holders extending their repayments is the reason. I don’t have a strong view on whether they will or won’t but I’d rather not take the risk.

A resigning auditor in 2025 isn’t great either.

Nor is a €2m increase of receivables either. I was under the impression that customers were prepaying, a €1.5m contract assets isn’t great. ECOB can ill afford to provide that kind of working capital so this is a major disappointment for me.

New funds and £2.35m was raised post period where 120m shares in issue grew to 140m shares with 10m 22p warrants.

"Billions in Backlog": Eco Buildings has long touted a massive framework pipeline (hundreds of millions in backlogged international contracts across Western Europe, Chile, and recently Senegal/Indonesia). These headline-grabbing, multi-million-pound framework agreements have not yet converted into actual, un-diluted cash flow. Again I hope they do and will, but I’d rather miss out on some upside and rejoin once there’s clearer evidence that they shall.

ECOB in the UK:

Digging around it appears Alister Bennett ran Opulent Designs from 2021 until 2024 and Envirovoid 2024 until early 2026. Both companies were essentially dormant but advertised modular buildings in the Philippines and described Bennett as ex John Laing with 40 years experience and a UK government advisor for modular housing. So there is a logical reason for their involvement but no discernable track record. Thompson appears not to have ever been a company Director before.

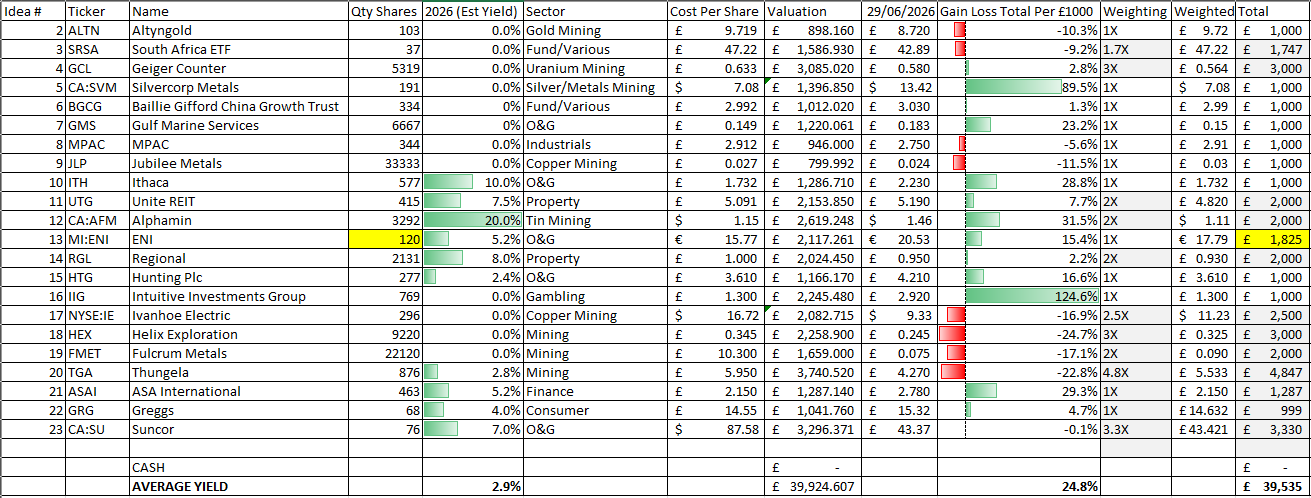

I decided to use the proceeds to add to ENI. Brings my average buy to €17.79

Why?

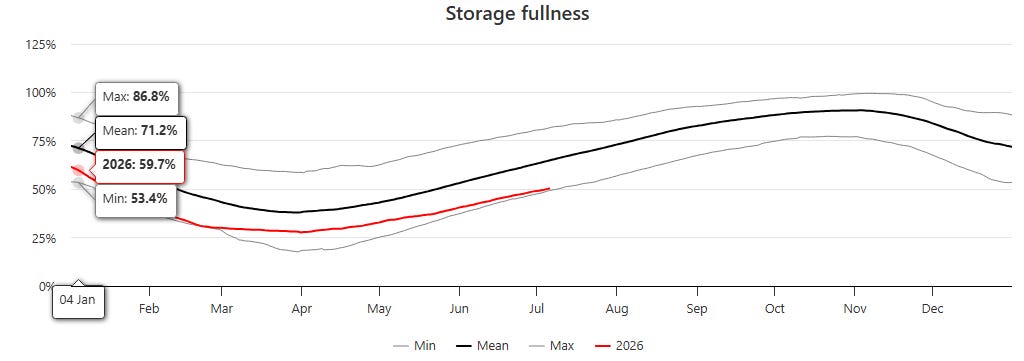

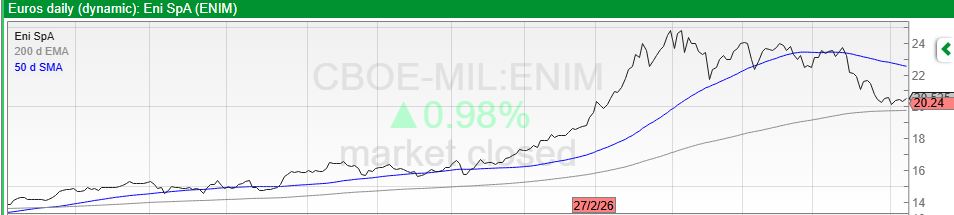

European gas storage levels are at “minimum” levels as pictured above, and ENI is a big beneficiary to this via its LNG supply but also as a downstream energy supplier. At €20.53 ENI offered a compelling price equal to that of the day prior to the third Gulf War. Time will tell whether a lean into O&G is foolish given the bounty of plenty we keep getting told about. I remain deeply sceptical as to the truth of that.

Regards

The Oak Bloke.

Disclaimers:

This content is for educational and informational purposes only. It does not consider your personal circumstances and is not financial, investment, tax, legal, or professional advice. Nothing here is a recommendation, offer, or solicitation to buy, sell, or hold any investment. Investing involves risk, including the loss of capital. You are solely responsible for your own decisions

Micro cap and Nano cap holdings and even mighty S&P 500 companies might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Probably 18+m ago, I tried to identify ECOB's facility in Durres - for which no address was given on the website. And an address still does not seem to be on the website or, maybe, is just hard to find - under the contact section, all that's given is : "Factory address - Durres, AL" .

Following various hints I found dotted around, I used Google Streetview to drive along all the likely roads in the industrial area to the north of the city. I failed to find any location that matched the pics of the facility then on the website. I visited Albania with my wife, but by then my interest was waning, and we didn't get to Durres.

I've not followed the story since - and got a fairly rough ride on ADVFN etc at the time for daring to want to actually identify the site we were being shown & told about.

I'd still want to check out what we are being told prior to any investment.

ENI has had a brilliant run, up 48% plus divis over 1 year vs under 15% for SHEL. Great spot!