CAML 'air

1H25 report from Central Asian Metals

Dear reader,

CAML blythely reported its results yesterday.

Blithely cut its dividend by 50% too using the other 50% to fund a $10m buy back. Great harrumphing was heard and a sell off ensued. I pounced at 149p. Let’s consider why.

1. What’s in CAML’s hump…… a 2.7p gain

First of all it was fairly easy to spot that sales were 474 tonnes fewer than production. At today’s $10,020 price that’s a $4.8m future gain. (eq’t to 2.7p per share)

$1.85m of finished goods may not look much but remember it’s held at cost and copper had an EBITDA margin of 72% in 1H25 - so that’s potentially $6m-$7m worth of copper in finished goods.

2. A 1.1p per share gain from NWR

Second CAML in the post period walk away from NWR with a profit of $2m profit net of all expenses , (eq’t 1.1p per share) and speaks of the experience it has gained. With long lifetimes left at Kounrad (9 years) and SASA (14 years) there’s no rush to go out and buy something whatever the cost.

CAML bid out quite quickly so perhaps they might have bid up the selling price further. I speculated in “CAML1h25” that a gain above 2p might be possible had they done so. To more than cover the $2.3m expenditure and come out 1.1p per share ahead seems a reasonable outcome.

3. Buy Back

A $10m buy back at today’s market cap is $356m (£263.3m)*. So CAML is priced at a $18m discount to its assets as at 12/09/25. $10m at an assumed £1.50 average share price will buy back 4.92m shares leaving 176.9m shares. At today’s 4.5p x 2 rebased dividend that equates to a cash saving of £0.44m per year from reduced dividends.

*- that’s based on the share price ask price 12/09/25 of £1.448 and 181,832,998 shares in issue

4. Follow the Money

Speaking of cash, the Cash generated from ops (down 10%) is far more impressive than Free Cash Flow $16.2m (down 46%). How come? One-off factors I cover below, wage rises, advance tax payments and Capex spend.

So there are quite a few factors that appear negative at first glance and in fact have been used as the basis to reduce the dividend when the underlying performance is not actually far less negative.

Although part of this cash generated is due to silver - and I cover that below.

5. One-off factors.

Running two plants is very much going to mess with your profits. That’s a one-off factor and now only one plant is being run.

FX created a $1.8m adverse movement too.

Of course further work is needed at SASA as a priority, and CAML are bringing in experts. Understanding and resolving the issue of orebody grade is the priority.

But the market has missed the upside from recent Capex spend. For example CAML achieved a 10% higher production at SASA in 1H25. From what they describe more to come too.

6. Don’t be fooled by a reduced EBITDA margin!

Silver prices have messed with the numbers too. Essentially part of the deal at CAML’s SASA mine is they have to sell the silver for a fixed $6 an ounce. If silver doubles in price or more (as has happened) revenue rises but the cost of sale rises by exactly the same amount. Silver has added approx $2.2m revenue and -$2.2m cost of sale to 1H25.

Consider these two simple examples of how your profit margin apparently gets “smashed” even though your profits are no different.

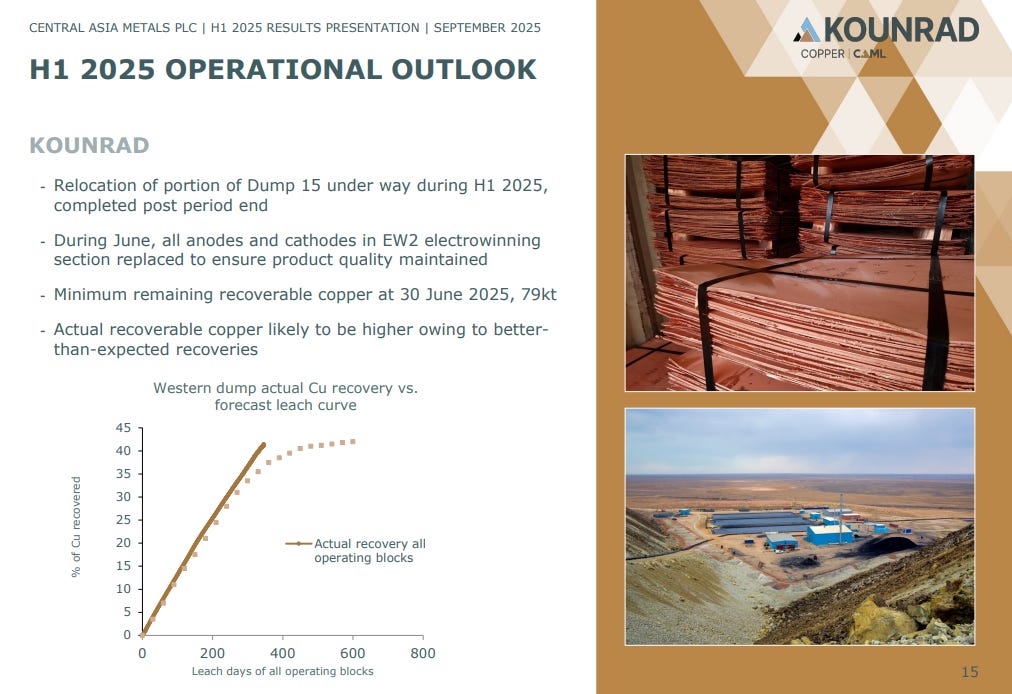

7. Kounrad remains a world-class Copper asset

Consider that Kounrad is outperforming expectations based upon its feasibility study.

Consider, too, that Copper is just above $10,000 per tonne. Prospectively could head higher. Just yesterday I was writing about how August 2025 UK motor vehicle demand for BEV/PHEV/HEV vehicles are now 49.7% of all cars sold. Those cars use lots of copper. Electrification is happening rapidly look at the US build out in 2025, Data Centres could consume 0.25mt - 0.55mt by 2030 (adding +1% - +2% global demand)

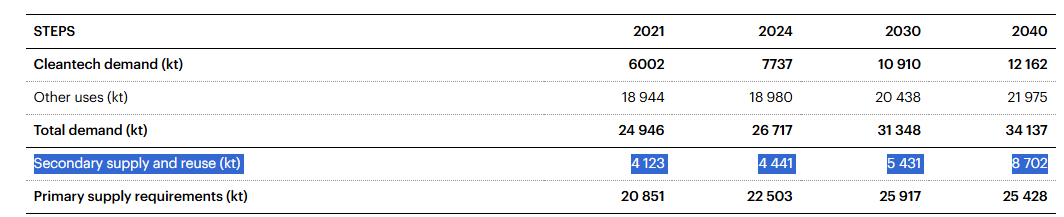

Essentially the question as to whether Copper will go up in price (using the IEA’s forecasts) is whether you agree that recycling of copper can increase somehow by 25% from today’s levels - so by about 1m tonnes per year.

Or if not then will projects get investment? Yes, some, at $10,000/tonne. But not all. Some projects will need higher Copper prices and outlook to get a successful investment decision.

8. I’m excited about Aberdeen Minerals

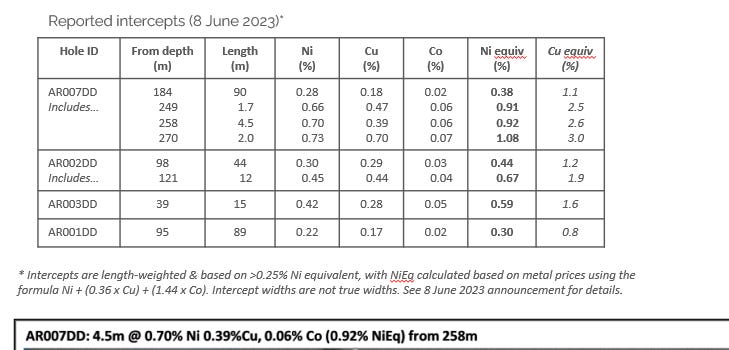

Aberdeen’s previous drill results are shown below based on a Nickel equivalent resource but the 0.36X copper and 1.44X Cobalt is way out, based on today’s prices. It should be 0.64X copper and 2.3X Cobalt.

If we ignore that and instead use the Copper Equivalent then the samples are very interesting. At 0.8%, 1.1%, 1.2% and 1.6% Cu equiv is well above the 0.4% - 0.6% global average for large Copper mines.

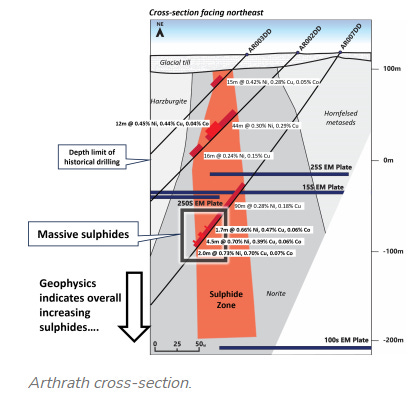

The above results are based on the below black lines and they only gone down just over 200m depth. The geo phys indicates that the resource continues to 400m or deeper…….

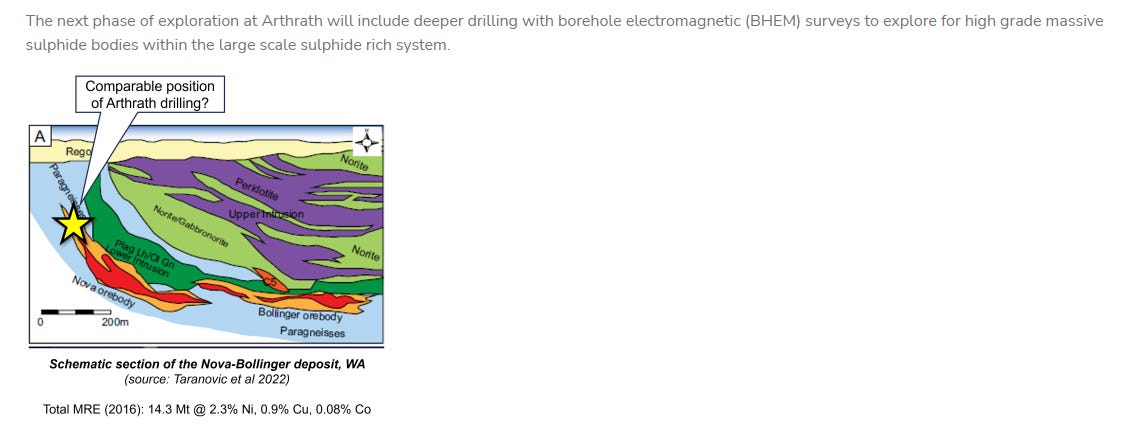

And that its project might and I say might be comparable to a Western Australia project called Nova-Bollinger. In the case of N-B there were 14.3Mt at 0.9% Copper, 2.3% Nickel and 0.08% Cobalt i.e. 2.7% Copper Equivalent. At as assumed 75% recovery you’re talking about £2bn of revenue (less operating costs).

Conclusion

A 6% dividend plus buy backs, plus a business which costs $360m to buy already has $70m cash ($290m net) and is capable of generating $50m - $70m free cash flow per annum

Regards

The Oak Bloke.

Disclaimers:

This is not advice, you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Thanks OB,

For another brilliant write up on CAML today. I watched the YouTube video a couple of times and the detail you have gone into is impressive. I skimmed the results on the day and thought they would get clobbered by about 20%. But I didn't see the detail that you have disclosed. Research is where I definitely need to learn more, along with a better understanding of the accounts.

I bought some more shares today as they definitely look cheap at the moment. I bought some a while ago at a higher price, so today was not only a good opportunity to get some at good price before everyone wakes up to that, but also to average down at a good rate.

Please keep the good ideas coming. Your work is much appreciated.

Graham.

CAML crashed today after the miner warned of a shorter lifespan for the Sasa zinc-lead operation, in North Macedonia, with a new life-of-mine plan resulting in a non-cash impairment charge of up to US$120 million.

Anyone selling? I am up 26% still so considering bailing.

https://www.proactiveinvestors.co.uk/companies/news/1088220/central-asia-metals-shares-drop-as-report-points-to-shorter-mine-life-at-sasa-1088220.html