CHRYing out loud!

A "likely" 5.5p/share gain - but what's the bigger picture?

NAV 134.65p, 69.5p/70.1p ask. 595.15m shares in issue. 47.94% discount to NAV.

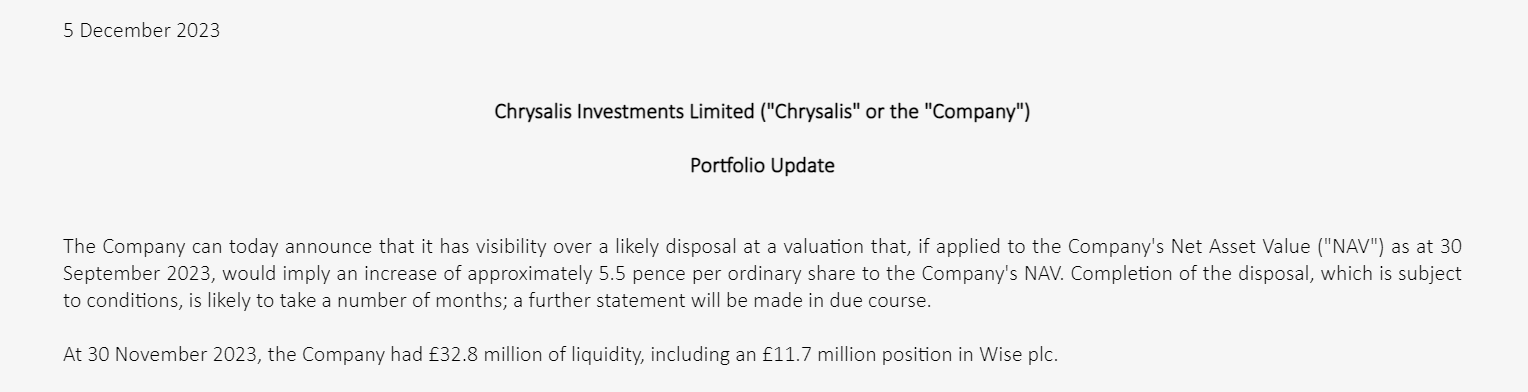

Today’s RNS:

I recently wrote about Chrysalis in don’t CHRY and pondered

A/ The potential future value of holdings

B/ The (in my opinion) unjustified discount

C/ The shafting of investors in the past

Sure enough a number of readers spoke out about the shafting (but not the discount or value). The past behaviour certainly colours peoples’ view of CHRY. Jupiter, the investment manager, got a huge £112m payout on the back of huge rises in 2021 but which had no clawback or deferred element. So in 2022 CHRY crashed and the gains reversed. That payout was a sore point. That incident is in the past now and a revised agreement is much fairer to investors. Cuts to charges and a new fee structure would prevent a repeat of yesterday. I guess there’s also an element of going the extra mile to try to convince investors to vote on a continuation.

So today’s news is of a 5.5p gain on a “likely disposal” to an unnamed holding. Who could that be?

If it’s CHRY’s largest holding, WeFox, which is 23.5% of the portfolio or 31.6p/share then 5.5p uplift represents a modest 17% gain.

But more than this, it UNDERLINES THE FACT THAT THE 48% DISCOUNT IS RIDICULOUS in my opinion. Moreover, it would represent a £220m cash realisation on top of £32.8m current liquidity. Why does that matter?

RNS 13/10/23

Summary of capital allocation policy

The proposed policy sets out a framework for disciplined capital usage, based around three principles:

· The Company will aim at all times to maintain a prudent cash reserve - the Board and Portfolio Manager guide that an appropriate cash reserve is currently believed to be £50 million;

· Having met the cash reserve requirement, the Company will next prioritise distributions to Shareholders - the Board currently intends to utilise its existing authority to buy back up to 15% of its share capital and, if required, seek further authority from Shareholders to continue share buy backs until £100 million of cash has been distributed, conditional on the ongoing discount; and

· Thereafter the Company will balance its capital allocation between further distributions to Shareholders and portfolio investments, aiming to distribute up to 25% of net cash profits on realisations.

So the impact would be £100m shares bought back (assuming they can all be bought back at 70p) is 142.8m shares. Net shares in issue drop to 452.35m. NAV drops to £701.37m which is 155p a share so a 20p gain per share.

Beyond this, “25% of net cash profits” which is presumably proceeds net of the buy back is £30m and is 6.6p a share extraordinary dividend. (assuming its paid subsequent to the buy backs). CHRY is left with £90m “firepower” of cash and listed holdings.

Now of course it might not be Wefox. Could be any of the top 4 (not #5 Klarna which is heading for an IPO), so the dividend would be less or zero.

Conversely, for any of the top 4 the percentage gain would higher. At the smallest end (and I’m excluding Graphcore, Wise and Sorted from being the unnamed disposal for various reasons), but taking Secret Escapes. That is 4.17p per CHRY share. So 5.5p uplift would represent a 231% premium to NAV. There would be a £58m cash realisation plus £32.8m liquidity = £90.8m so a £40.8m of buy backs.

Conclusion:

Whether a big or small holding the “likely” news of a 5.5p uplift is significant. The market has reacted with a 0.7% increase today. For CHRYing out loud, the market is asleep! Do the maths.

This is not advice.