Counting Discounting

Review of "May the Fourth of Discounts"

Dear reader,

Thank you to the 96 (!!) folks who have contributed to the Oak Bloke’s 2025 Fundraiser for Emmaus.

Emmaus gives people a hand up and not a hand out - and that’s why I ask you to help me support them.

Thank you!

I happened to revisit my article “May The Fourth of Closing Discounts” this week and wondered 8 months later on how have these performed?

Are there any lessons to learn, or pockets (chasms) of value?

Since my May 2024 article I have added new ideas to my “universe” of VC/PE (APAX, FIPP, MERC, JPEL, XLPE, LIV) and I considered extending this article but decided to just consider the prior consideration set. Contrasting 10 holdings is enough work as it is!!

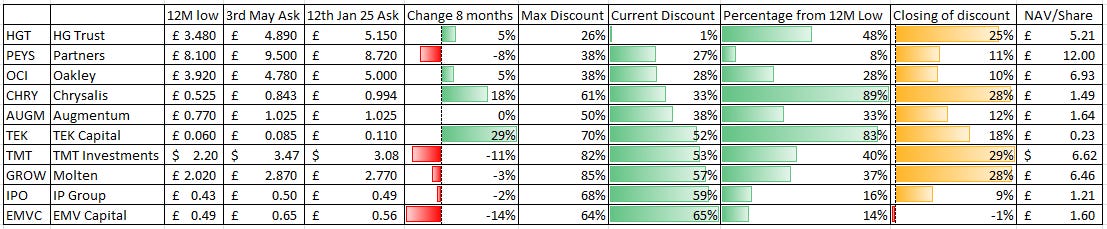

Re-running the numbers we see HGT compared to its maximum discount today trades on nearly no discount while IP Group and EMV Capital has barely moved.

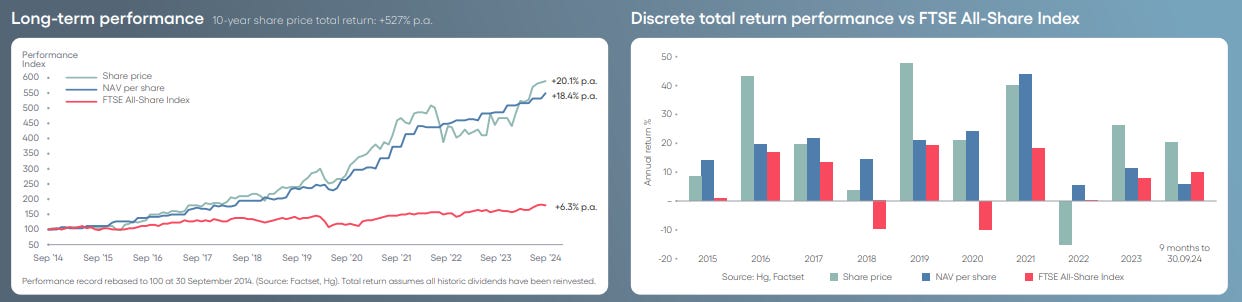

Could consistent returns for HGT be the key? No lumpiness, just a steady NAV growth? We see that below. HGT has delivered that growth over the long term. By focusing on software and typically SAAS subscription software, it is valued more like a software business. Software is a potential beneficiary for the application of AI.

EMVC

OB 25 for 25 idea EMV Capital delivered NAV growth in 2024, but achieved no realisations. Its holdings are admittedly earlier stage, and less cash generative. Not so much software to see here. Although we do see a 23% NAV fair value performance nowhere in the share price.

So not far behind EMVC in terms of discount levels are two FTSE250 businesses: GROW and IPO. It is a great surprise to see them at >50% discount to NAV. Well I hold them so it’s not a surprise to me but I mean it should come as a surprising relevation to many.

Note in my list I have put IP Group’s NAV at £1.21/share based on the post period newsflow around realisations at FeatureSpace, Intelligent Ultrasound and also the price reversion of (listed) holding Oxford Nanopore. The official NAV as at 30th June is about 15p a share lower.

GROW

Since my article Molten (ticker GROW) released their 30th September NAV in their interims. Shortly before these were released I wrote about GROW in “grow GROW so sew”. I saw last week the share drop to £2.70 so bought more. That £2.70 buy price is covered by just five of its holdings:

a/ Thought Machine with its string of banking software clients coming online in 2025

b/ Coachhub with their enviable client list

c/ Aiven with its AWS, Google Cloud and Azure partnerships providing data centre users a simplified and secure way to deploy, manage and scale,

d/ Ledger with its Cryptocurrency storage gadgets

e/ Revolut and its prospective 2025 IPO at its fair value.

Any upward valuation to the first 4 is in the price for free.

Plus £4.30 per share of other holdings are also in the price for free.

IPO

IP Group with its long string of announcements and realisations, none at a discount. How many more realisations will it take? How is it trading below its market price back in May considering the news flow since then? Also considering the buy backs? Considering a 31% appreciation of its listed holding ONT?

On the 4th May there were 1.03bn IPO shares and today only 0.973bn shares remain so that’s 0.06bn bought back so nearly 6% of shares in 8 months.

TMT

OB 24 pick TMT has been quieter in its newsflow but since the 3rd May announced its 1H24 result where its NAV was unchanged at $6.62 per share, with its Praktita AI learning holding increasing in fair value 12.4X in just 5 months! Bolt prepares for its IPO.

TEK

Another OB 24 pick TEK IPO’d its Gen IP and while volatile, it trades not far off its initial price adding 2p a share to TEK. Another holding BELL is also an OB 24 pick and the jury is out on that one, but with $4m of invoice funding it has its 2nd device launched in the market and 2025 is when Hon Hai start paying royalties to BELL. Guident is going to be IPO’d in 2025, and Lucy another volatile stock has launched its safety glasses, Nautica, Eddie Bauer, and next come Reebok. Finally Microsalt is double its IPO price and its global food company continues to place orders and continues testing and sign offs. What news flow will we see on that in 2025? What is the value of halving salt in foods, without compromising flavour?

AUGM

Augmentum reduced their NAV by 2.7p mainly via a reduction at its holding Grover (rent don’t buy) although the outlook for Grover appears to be improving. Meanwhile its bank Tide, lender iWoca and banking-as-a-service holding XYB all grew in fair value. Realisations of Onfido and FullCircl were both at premiums to NAV. AUGM’s top 4 have performed strongly (and I’m bullish about Bullion Vault given the movement in gold/silver in 2024 and now in 2025)

Partners

Partners Private Equity is actually down in NAV terms from 15 Euros to 14.40 from 12 months yet has ranking of nearly 90 on stocko. Its P&L past results are a mix of gains and losses, but this chart shows a decade of steady NAV growth and points towards promising future performance.

Oakley

Were the 2010s a decade of disappointment for Oakley ticker OCI? If they were then post covid someone put some fireworks beneath Oakley and changed its trajectory for the roaring 20s. Will we see more roar in 2025?

Conclusion

I don’t hold HGT, PEYS and OCI. I hold the rest.

Where you land with this rather depends on your perspective. The holdings across the 10 are vastly different. The “Private Equity” and “Venture/Growth” labels they share but the holdings are all very different.

HGT focuses on mature software holdings so gets valued as a software business. Having used the software of some of its holdings it’s not one I like very much, but that’s not necessarily a good reason to overlook this. I do wonder about the competitive dynamics vs Oracle, SAP and Sage. Yes the world of ERP is a big place but it is filled with big and successful opponents. I do wonder whether that steady NAV uplift is enough of an incentive to own this. That’s the perspective of an outsider looking in. Clearly it is well-liked by many.

Partners (previously Princess) is a much lower profile holding, but actually shows strong long term performance and backed by a global PE house. I come away a little bit intrigued to explore Partners further at a later date.

OCI appears to pick good businesses which are large, later stage and well funded, but appear a mish mash (I appreciate readers might vehemently disagree with my superficial view). Also what happens if the roaring 20s stop roaring? The 2010s were pedestrian.

CHRY is the top performer in terms of “most improved” but rather than exit, the upside with Klarna, Smart Pension and other holdings (as I wrote about earlier today) means I’m reluctant to sell. The headline 33% discount does not tell the whole story of upside I believe. A big question turns in 2025 to how will CHRY recycle its realisations? Can it buy exciting new ideas?

AUGM has some holdings which are going great guns. Tide, Zopa and Bullion Vault are all ones to watch in 2025. But AUGM has suffered a few setbacks too.

TEK has actually delivered a far stronger performance than many expected. The Oak Bloke was a lonely voice on this idea for quite a while admist a mob of angry harrumphers. Cash remains a challenge for TEK although making limited realisations of its holdings should ease that in 2025. The fact that its share price is >100% covered by listed holdings means you effectively get paid to buy TEK for free. Listed holding exceed the share price by 4.6p a share, and once Guident is floated by 12p (assuming it IPOs only at its NAV with no upside) - that’s the 52% discount for you. Once Guident in 2025 is listed and its EV regenerative energy car suspension spun out or killed off what then? Will we see a sell down of listed holdings and new holdings added, or a wind down of its activities? I really don’t know, but any of those paths should offer upside.

TMT’s big event in 2025 will be Bolt.eu and its IPO. The read across from Lyft and Uber bodes very well. Its many software holdings and early stage businesses meanwhile contain some gems. PandaDoc is one I particularly like. 53% discount in a thawing market is cheap.

GROW at a 57% discount (plus more if you consider the fair value of IPO candidate Revolut), is compelling. It has achieved good realisations in 2024 so holds plenty of cash plus has a large VCT/EIS business to back holdings also. Appreciate this is neither an OB24 for OB25 idea but at £2.77 it is deeply mispriced, and GROW gets my #1 pick for this article.

To substantiate that a little further, consider over 4 years ignoring FX GROW has delivered £1.1bn of gains (and -£0.72 bn of losses). Net gains of £100m a year for a share you can buy today for £516m, equates to nearly 20% underlying performance per annum.

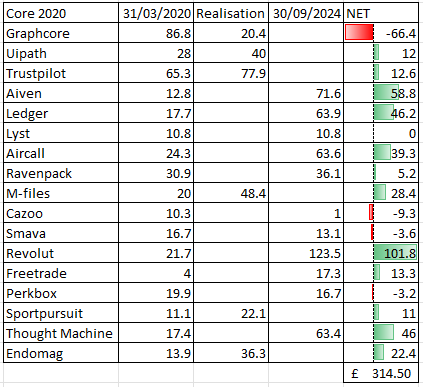

Another way to visualise GROW is to take the Core portfolio from 2020 and ask what happened. The result is a £314.5m net gain. Those that remain in GROW’s portfolio as at 30/09/24 are shown in column 3 (M-files was disposed post period), while those sold or disposed are shown in column 2 along with the amount realised. Column 4 shows the net gain or loss. It is interesting that over 80% of net gains (£314.5m of £359.3m) come from a handful of core holdings from 5 years ago.

Graphcore vs NVidia is an standout exception. It lacked scale and any kind of government support (UK Gov bought NVidia chips) but could have been so much more. Its Intelligence Processing Units were far better suited than NVidia’s Graphic Processing Units to data centre tasks. Softbank now own Graphcore and it is being absorbed into Arm. That’s one to watch. Other GROW losses are pretty negligible while the 5 year gains - and the hit rate - on a 5 year basis is fairly impressive.

OB24 idea IPO is deeply mispriced too, at its 59% discount, despite large realisations in 2024 at a premium, 6% of shares bought back, and a warchest to commit to its holdings and a large VCT/EIS business too. Its #1 holding Oxford Nanopore is up 31% since its last NAV results for June in 1H24. It gets my #2 pick for this article.

Finally OB25 idea EMVC is a deeply unloved creature, and holds the largest discount as a result. It does need to achieve some realisations and wins, and to grow its AuM but that’s why I picked it for 2025. If it does achieve those two objectives from its heavily pregant portfolio then the upside will be substantial.

Regards

The Oak Bloke

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

I've always struggled to reconcile HGT reported NAV performance with the 7-8x net debt/EBITDA in this rate environment... and 26x EV/EBITDA is priced to perfection! fwiw I prefer e.g. CTPE with 3.1x and 11x respectively

Given your deep dive in IP group is it fair to assume that’s your favorite? Other than discount to NAV, what are the reasons you like it more than others? Is it the deep tech focus or perhaps mgmt team or overall strategy?