Evening reader,

Listening to a recent Voxmarkets interview with this gentleman from the Marlborough Multi Cap this evening I was struck by the comment he made about a “$500m unrealised opportunity at DEC”. He doesn’t elaborate what he means or how he arrives at the figure $500m but he got me thinking. And looking. Looking for $500m

As you do.

PDP in O&G vernacular means proved, developed and producing - so it refers to active wells. So what happens when acreage is unproven, undeveloped and not producing? Well the answer is they DO NOT sit on the balance sheet, beyond their overall purchase price. So when I recently analysed in DEC-tecting fact and fiction regarding ARO (Asset Retirement Obligations) I was interested in what’s on the balance sheet and what’s getting added and removed to and from the balance sheet. You’ll recall that the ARO numbers reconciled with potentially quite some change to spare. And we concluded you’d have to be a bit of a spanner to think a well needs an average $100k to decommission. Or have a bit of an agenda.

So anyway, today let’s look at what’s not there on the balance sheet. If you read the DEC annual report there’s nothing to see. But if we visit their Corporate presentation they find an ah hah! Let’s look at Tanos.

This is from the 15th November presentation deck.

Let’s decompress what this slide is telling us. Top left corner, PV17 means the $250m to buy Tanos was like to spend $250m and get back the equivalent $250m in future earnings from PDP wells means you’d need to discount those by 17% discount to “break even”.

2.3X means the $107m gross profit (the EBITDA) from PDP wells is 2.3 times its purchase price. So in about 27 months you’d break even in simple cash terms (no discount).

20% accretive means $107m joins ~$428m to provide $535m FCF or free cash flow. And a similar-ish number for adjusted EBITDA. We kind of know these numbers already from the 2022 and H1 2023 results.

Over on the right PV10 $312m means instead of break even, let’s apply a 10% discount to future cash. In that case that cash is worth a discounted $312m (i.e. there’s a $62m “real profit”)

PV28 means that it would take a 28% discount on earnings on undeveloped and developed to “break even” to the $250m. And we can see there’s a $279m profit for the 50 undeveloped locations using a PV10 (10%) discount.

So reader, that $279m future potential value or profit IS NOT ON THE DEC BALANCE SHEET. Only PDP assets are in the balance sheet. It’s not in the annual report. Not in the numbers. Accountants insist on prudence. Instead, it’s tucked away in a presentation. Waiting for someone like the Oak Bloke to shout out about it.

Of course these hidden upside numbers “bubble to the surface” and can then get recognised to the P&L and balance sheet, when they are either divested or developed (AKA “Gain on Disposal”). DEC highlight this to us as “free upside” as we can see on slide 12 of the presentation below.

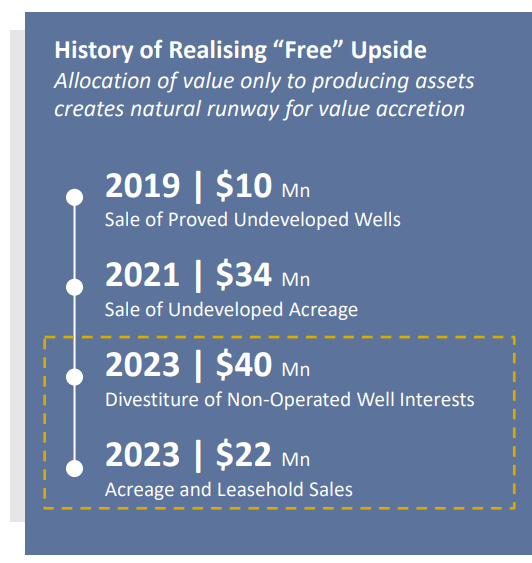

Now of the 2023 sales, one of them, $40m was from the balance sheet. It was PDP. This was for non-operated well interests. So disposing because DEC has a limited ability to apply Smart Asset Management - SAM - cost cutting and possibly location wasn’t close to other assets - so better to get rid if there’s a willing buyer.

Another $22m was non-PDP. In 2021 disposals were $34m and 2019 $10m. So that’s $66m “free” upside from non-PDP over the past 4 years.

How much non-PDP is there? $500m?

But let’s examine slide 23 further. $279m of value for 50 locations relating to Tanos acquisition. But we see there’s a further 300 locations listed in addition. What value are those I wonder? Could those be worth $221m hence the unrealised $500m? Or are 6x the locations worth 6x the 50 locations for $279m = $1.674bn? DEC only describe the upside as “substantial”. Where does $279m come from? These are estimates of reserves produced by an institute of petroleum engineers. It’s unclear whether these are P1/P2/P3 reserves (i.e. how certain they are). But we aren’t just talking about the price of land here, we’re talking about the potential estimated value of Oil and Gas under that land.

The point is whether it’s $1.7bn, $500m or another value we can see several proofs they aren’t worth zero. $66m reasons why. The hidden value is there in plain sight - and a further upside for DEC hands to consider!

If $500m is the correct number, do you realise that’s 2/3 of today’s share price! (Or 2.2X if $1.7bn is correct). Whatever it is that number will not show up on any kind of “traditional” financial analysis based on the statutory accounts.

The penultimate thought

Today you could buy DEC for £597m. That’s its market cap.

Cumulative dividends to date for DEC are £634m. Its historic return has exceeded its buy price which is an astonishing achievement for a young company which listed on AIM in February 2017! I tried to find comparative stats but can’t. Shell has possibly repaid 5-6X its market cap through dividends over its year (ignoring compounding) ….. but over its 127 years!!!! Where is DEC’s share price reflecting that its yield has been consistently great over its entire 6 years lifetime?!

This is the Wikipedia history of DEC which was a twinkling in Rusty Hutson’s eye in 2001, just before he bought his 1st gas well.

Today, with dividends maintained and a 22.8% yield, over the next 4 years and 3 months you will arrive at 2X returns for the market cap. That’s how insane the current share price is. 22.8%.

The final thought

I believe falling gas prices are driving the share price. But thank goodness we are substantially hedged at 85% of volume at $3.53. The market appears to be ignorant to this fact and is chucking DEC out with the bath water.

But imagine how much pain there must at these prices be for private/small gas well operators who haven’t hedged? Current prices are back to Covid lows when lockdowns were in full swing. Look outside reader, do you see empty streets of a lockdown? Do you hear clapping on a Thursday eve? Nope, yet here we are with the price of gas apparently. And some operations are losing money at these prices.

(Perhaps my utility provider is one of those? They just increased my price per KWH gas by nearly 10% from 1st Jan)

Meanwhile, stateside, DEC do have $135m of firepower. When’s the best time to buy distressed assets? When they are distressed. Couple more disposals out of that $500m hidden pot, some non-operated asset disposals, the H2 profits and who knows perhaps another Tanos-size acquisition with similar upside is on the cards in 2024!

Have a good evening.

This is not advice.

Oak

I guess the gas price issue is not just a halo effect. It's likely to result in renegotiated hedge contracts. Yes I know that shouldn't happen but it does, the legal punishment for breaking the hedge being much lower than the gains made by buying elsewhere, hence the 2022 $100m adjustment. It's an El Nino winter effect, but takes no account of the potential for export demand at these prices. It's a wait and see for sure.

House Democrats open probe into $DEC. Hard to predict what that means for the SP in the near future...