Dear reader

After a lovely two-week hiatus in Africa with as much internet signal as you’d expect in the early 1990s, but now back in Blighty, here is your article 205 from the Oak Bloke.

I’d really like to continue from my prior article DEC-ade planning. In part of this article I explored what DEC are themselves exploring: opportunities for alternative wellbore uses. I speculated that:

The model I expect DEC would follow would be to run a 2nd set of pipes from power stations and large industrial users back to CCUS-ready wells and for DEC to do the sequestering.

But how practical is this idea to capture carbon? Is this just a pipe dream? What detail lies beneath the blithe statement? And what risk?

I hope to explore that further today.

DEC currently have 17,700 miles of “Midstream” pipelines. While upstream in O&G parlance refers to the primary production, midstream refers to the transportation of natural gas. Oil is trucked meanwhile according to the DEC sustainability report.

Whether 17,700 miles covers all transportation is a moot point but a 2nd set of pipes for 17,700 miles at an average $10.7m a mile (according to O&G journal) although can range from $0.3m - $22.6m a Km according to Gem.

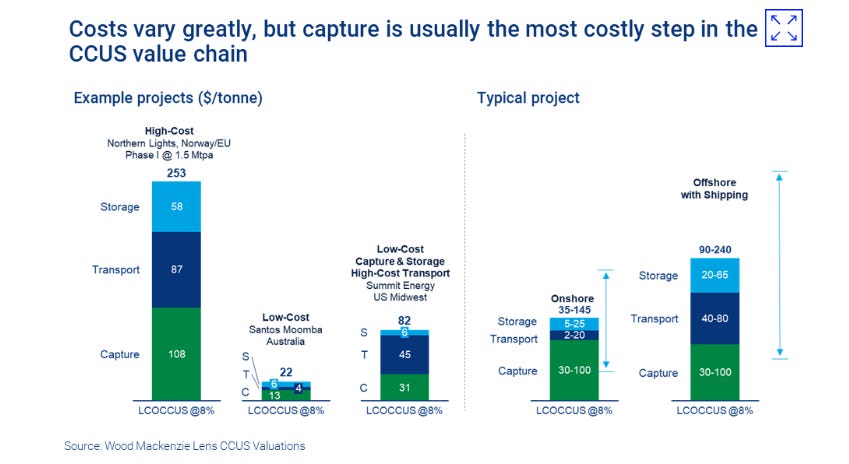

Let’s assume $10.7m a mile. That comes in at $182bn. Ouch. According to this report by Wood Mackenzie the cost of transportation per tonne of CO2 of $7-$45. Assumes zero marginal costs (which isn’t realistic) that translates to 4bn - 26bn tonnes of CO2 to hit $7-$45 a tonne. That’s up to 50% of global emissions. Hmmm that’s not going to happen.

But the pain doesn’t stop there. The bulk of cost is in the capture. A further $30-$100 a tonne according to the same report.

In my article I also spoke to the incentives.

$50 to $85 per ton of CO2, for sequestered industrial or power emissions, and from $50 to $180 a ton for emissions captured from the atmosphere and sequestered.

But who would receive this benefit? I blithely assumed DEC would. DEC being the service provider storing the CO2. But what about the polluter generating the CO2 (the industrial/power emitter), do they get a cut? What about the project builder who builds the capture facilities? Who gets the revenue? Or is there a mixture between these?

Let’s start to unpack this.

For a start I do not believe DEC will run extensive pipes across their whole estate. And to spend $182bn to run a set of pipes would be balmy. But does DEC need to? Instead, surely, they would selectively pick wells which are proximate to an industrial user or power generator. Wells for storage require a Class VI permit from the EPA, and the EPA report they are focused on ramping up federal and state capacity including the technical and regulatory expertise needed to evaluate permits. Congress provided funding via the IRA and the BIL to add staff to the Class VI permitting program at the EPA, which committed to focusing on streamlining the permitting process, performing continuous programmatic evaluations, and increasing public outreach, awareness, and transparency.

Selectively building pipelines

If we are talking 10s of miles of pipeline, suddenly the economics change. $10.7m a mile for 30 miles is $321m. Still a princely sum, but achieveable and amortised over millions of tonnes, it’s conceivable that the $7 a tonne number could be achievable. Assuming the $7/tonne comprises 50% op. cost and 50% capex we are talking just 92m tonnes of CO2 to arrive at $7/tonne. To put 92mt in perspective Chevron’s “River Bend CCS” project has a 620Mt storage resource. The simple truth is if it’s not profitable and practical, then it won’t happen. DEC speak to “early stage exploration” of this idea.

I also believe the idea that the polluter receives any part of a credit would be bonkers too. The polluter avoids a liability (pollution) and future carbon tax. That’s their reward, surely? However I was remiss in not exploring the role of the CCS facility provider. I’ve read different approaches of using either a solvent or steam but this animation provides an illustration. There’s clearly an opex and a capex cost to extracting CO2.

Of course the polluter might also be the project builder. i.e. the industrial user or power generates also builds and operates the CCS facility.

At this stage it’s also clear that DEC would not be the project builder/operator, although who knows for the future - they’ve developed NextLVL from a series of acquisition so perhaps an opportunity lies in developing CCS expertise too?

But let’s assume not - for now. So a more realistic approach is to consider the revenue opportunity as a split of revenue according to a $7 vs $30 split of costs, based on Wood Mackenzie’s cost estimates. In this way we are looking at an inverse pareto distribution of 20/80. 20% of the $85/tonne revenue for storage is $17/tonne revenue so that leaves $3-$10 a tonne profit to the storer (i.e. to DEC) using Wood Mackenzie’s numbers, even after giving to Caesar what is Caesar’s (i.e. the CCS project builder/operator).

DEC isn’t planning to blaze a trail with CCS. Larger players like Chevron, Equinor and Shell have been blazing for over 10 years. In fact as at July 2023 there are 41 CCS projects in operation, 26 under construction and 325 in development.

CCS capacity grew 48% year on year to 361mtpa. This is an acceleration from a 35% CAGR going back to 2017. Growth in pipeline is even higher at 57% growth year on year since 2020. So the idea of DEC following in the many other footsteps appears to come with diminished risk (since the economics are increasingly understood and costs decline as projects move down the experience curve). The project comes with significant policy support (not least from the US Inflation Reduction Act).

In fact it is estimated the IRA alone, will increase CCS by 70%-80% globally (200-250mtpa) by 2030.

But it’s not just the IRA!

While I blithely omitted risks and downsides I also omitted upsides too. CCS gets support from other US sources too. The 2021 Bipartisan Infrastructure Law (BIL) and the 2022 CHIPS Act also provide financial and policy incentives. The BIL provides $12 billion for programs such as carbon management, research, demonstration and deployment up to 2026. The funds provide $8.5 billion in supplemental funding for CCS for FY2022- FY2026, including funding for the construction of new carbon capture facilities and commercial carbon storage facilities, and $3.6 billion in supplemental funding for DAC, primarily to support the establishment of four regional direct air capture hubs in the US.

The CHIPS Act Sec. 10102 authorised the DOE to establish a “Carbon Sequestration Research and Geologic Computational Science Initiative” and at least two carbon storage research and geologic computational science centers to expand the fundamental knowledge, data collection, data analysis, and modelling of subsurface geology for advancing carbon sequestration in geologic formations. Under CHIPS, the US Department of Energy (DOE) will carry out research for the sequestration of carbon in geologic formations.

The experience curve is not only happening in the US either. Norway, the UK, the EU, Canada, Japan, South Korea, India, Australia and China are all aggressively working on CCS projects too.

Is DEC also feeling Blue?

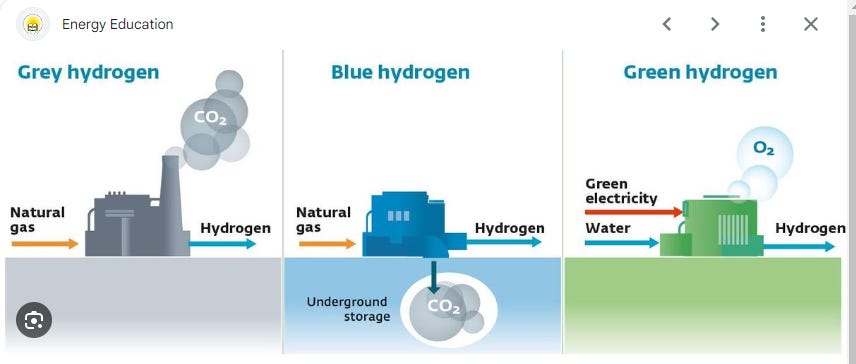

My article also omitted to consider Blue Hydrogen. I have previously considered green hydrogen both in my article nice looking sales CWR and IP Group’s Hysata holding. More on that later.

For colour-blind readers here’s a partial guide to the Benetton many colours of hydrogen.

Interestingly DEC’s peer EQT is deeply embedded in Blue Hydrogen to the point where they boast they will be scope 1 & 2 CO2 neutral by next year. That’s quite an achievement if they can pull it off? Blue hydrogen is a form of returning CO2 to a well. Imagine reader how many (fewer) miles of pipeline you’d need if you could strip the “H” (the hydrogen) from the CH4 (methane) and send the CO2 down into an adjacent well? And the H2 down existing midstream pipes. The remaining CO2 goes straight into the ground either to stimulate further production or for storage. Hydrogen can be blended with natural gas also.

The US government as part of its BIL committed $7bn in late 2023 to developing “Hydrogen Hubs” driving a further $50bn of private investment from the likes of EQT which is leading with the hub in Appalachia (which received $0.92bn of the $7bn).

The strategic location of this H2Hub around Ohio, West Virgina and Pensylvania is the development of hydrogen pipelines, multiple hydrogen fueling stations, and permanent CO2 storage also have the potential to drive down the cost of hydrogen distribution and storage. The Appalachian Hydrogen Hub is anticipated to bring quality job opportunities to workers in coal communities and create more than 21,000 direct jobs—including more than 18,000 in construction and more than 3,000 permanent jobs, helping ensure the Appalachian community benefits from the development and operation of the Hub. (Amount: up to $925 million)

DEC is on the sidelines of this initiative at this stage but where EQT leads DEC can follow - at lower cost and lower risk. That’s the point of creating a hub, is that you initiate activity that then perpetuates. As a major Appalachian player, DEC stands to benefit if this hub can succeed and grow.

Beyond the Blue

As well as CCS, as well as production of blue hydrogen I also omitted to consider hydrogen storage. I read about recent US research which concludes exhausted gas wells could be used to store hydrogen.

Hydrogen is typically stored in liquid form in tanks has to be stored at 350-700 PSI (to go from gas to liquid). The energy needed to compress it to those pressures is a major component of cost. Interesting then that wells would not require pressurisation and that losses were found to be minimal.

It might surprise you reader to learn that 1.2TW of Eletrolyzers are currently being built - and a third of that number is in the USA. Electrolyzers are a means to convert green electricity into Hydrogen. A KG of hydrogen holds 33.3KWH of usable energy based on its lower heating value and some electrolysers consume 50-60KWH of electricity hence the 40%-50% efficiency “round trip” argument. But Hysata have achieved 41.5KWH and Ceres can achieve 52KWH or 39KWH combined with industrial processes.

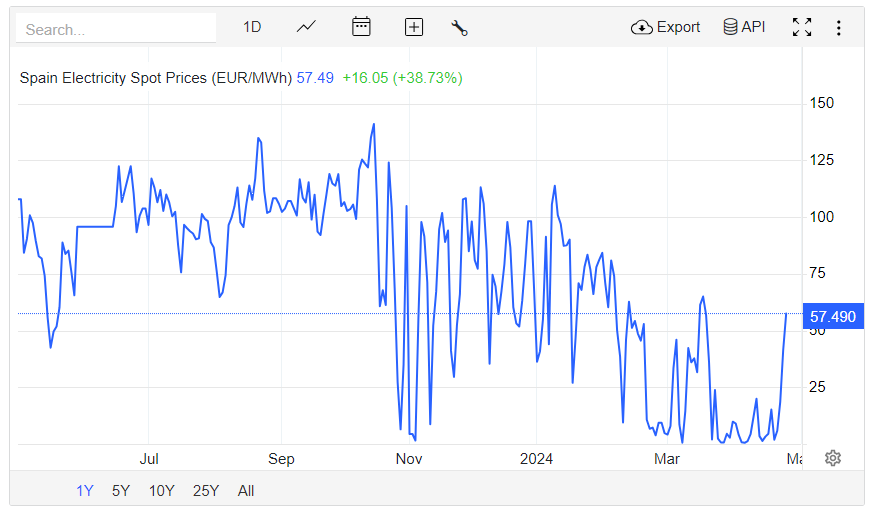

Even with only 40%-50% efficiency, I am mindful that renewables wax and wane. This has been acutely evidenced to me based on Spanish electricity prices. I was gobsmacked to see wholesale electricity practically being worthless during large parts of April. A MWH cost mere Euro cents as can be seen below. With solar and wind production being rapidly built in the USA, opportunity to store hydrogen will grow too.

Other energy storage opportunities I omitted to discuss:

At Renewell Energy, CEO and co-founder Kemp Gregory aims to convert North America’s 2.6 million inactive oil and gas wells into clean energy storage systems. The idea is to store and release electricity by lifting and lowering a cylindrical weight sealed inside each well. At an estimated $5/kWh, this storage method is cost-effective and contains methane leaks as an added benefit. Launched in 2020 and based in Bakersfield, Calif. and Houston, Texas, Renewell graduated from SOVS’s HAX program and has since received $2.7 million in DoE grants and raised $3 million in seed funding from investors including SOSV, Third Sphere, and Preston-Werner Ventures, the VC fund of Github founder Thomas Preston-Werner.

Energy Dome, led by CEO and founder Claudio Spadacini, is developing a utility-scale, long-duration “CO2 battery.” It stores clean energy by compressing CO2 into liquid at ambient temperatures and then releases energy as needed by allowing that CO2 to expand into gas and drive a turbine. Energy Dome claims its systems will last for over 30 years without degradation and cost less than half as much as an equivalent lithium-ion system. Based in Milan, Italy, Energy Dome closed a €40M Series B in April 2023 led by Eni Next, the venture arm of Italian energy giant Eni, and co-led by Neva SGR, the venture wing of Intesa Sanpaolo, a European banking group. In total, Energy Dome has raised €54M.

Ramya Swaminathan, CEO of Malta Inc., leads a team developing thermo-electric energy storage. Built for electric utilities, grid operators, and industrial firms, Malta’s system uses electricity to drive a pump, which converts electrical energy into thermal energy by creating a temperature difference. The resultant heat, stored as molten salt, and cold, captured in antifreeze liquid, are the basis for a thermodynamic heat engine that drives an electric generator to produce power for the grid. Based in Cambridge, Mass., Malta incubated at X, Alphabet’s Moonshot Factory, and has raised $86M from investors including Proman (natural gas products), Breakthrough Energy Ventures, Chevron, Facebook co-founder Dustin Moskovitz, Alfa Laval (heat transfer, separation and fluid handling systems), and Piva Capital.

Penultimate thought

If 17,700 miles of pipelines has a replacement cost of $82bn, then that asset is pretty valuable isn’t it? Yet the book value in DEC of that pipeline is a very small fraction of that. Hidden value?

Conclusion

To be entirely clear (and as DEC are entirely clear in their 2023 sustainability report) these are long-term opportunities being explored.

Yes, there are risks to trail blazing into these areas. But DEC isn’t doing that. So when “considering the risks” it seems others are undertaking those risks at least partially with US government support. Where others lead DEC can follow.

The economics of following into these areas appears attractive. If I too blithely spoke of building pipelines, then on a practical basis yes transporting CO2 has to happen somehow. Yes it’s true there’s infrastructure and capex/opex costs to that CCS infrastructure. It is also true that initiatives in this area are not trivial.

But I put it to you reader that I have evidenced substantial progress is rapidly changing the picture around CCS and it is reasonably conceivable that DEC-hands should be considering the value of the DEC estate not purely for its reserves of gas and oil (although obviously these are important) but also for future strategic value beyond its fossil fuels.

I also stand by my earlier conclusion that DEC’s ability to steward its assets is an “inconvenient truth” for detractors. Its ability to be the Right Company at the Right Time is not only to play an active role in Energy production but also contributing towards Net Zero.

Beyond the circa 60% discount to NAV, based on book value let alone NPV, should we also consider its future strategic value?

Whether you consider its future strategic value to be to a lesser or greater value again is a moot point…. but it certainly exists.

What is considered today its liability - its ARO - is also to a lesser or greater extent also an asset. And is the value of that asset - its estate - reflected in the price of DEC? Well, reader, it simply isn’t.

This is not advice

Oak

WSJ had a great article about carbon capture that relates to this thank you so much https://www.wsj.com/articles/environmental-protection-agency-rules-power-plants-fossil-fuels-coal-natural-gas-b6d2ea72?st=uib470dyz9aja0d&reflink=article_copyURL_share