Deep deep into Arqiva - part of DGI

Does it have 20:31 vision?

DGI9 own 48.02% of Arqiva and paid £463m.

Arqiva is beaming. Television & Radio that is. Starting at the Ally Pally back in 1936 when some clipped Queen’s English tones said “Hello Radio Olympia…” and broadcast to the nation for the very first time. Here it is:

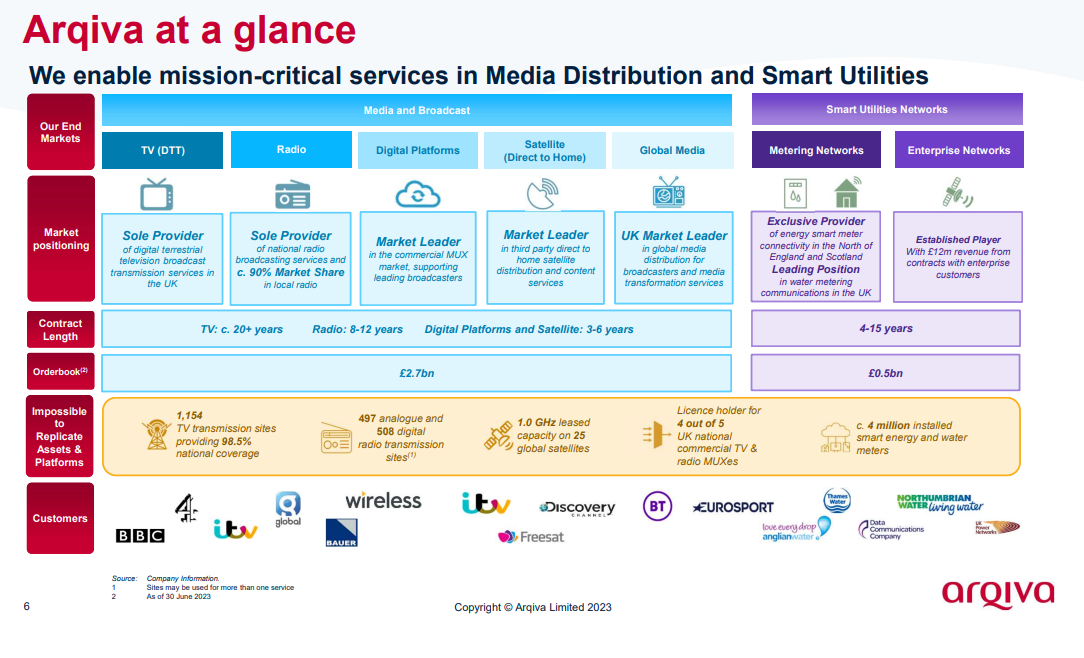

Since then it’s the main infrastructure provider of Freeview (98.5% of the population), Satellite TV, Teletext, DAB, Analogue Radio. Arqiva deliver the infrastructure (satellites, TV sites/masts) which connects broadcasters with 99% of viewers/listeners. It also is a big noise in the 5G roll out. When Kate Adie and her flakjacket are reporting from a far flung place in the world Arqiva makes that happen - broadcasters like the BBC don’t actually manage the technology infrastructure themselves.

Defensive anyone?

The latest accounts to June 2023 show:

Media and Broadcast contributes significant and stable cash flows to the group with a long-term contracted, substantially RPI-linked order book of £2.6bn which includes established, major contracts running as far as 2035.

Now it is working towards Vision 2031.

Couple of notable points:

1/ Arqade is a new and exciting workflow product for content providers to build and deliver interchangeable content for broadcasters. Think the equivalent of a “YouTube for Television” along with a play list. NBC Universal for example use this in Australia and NZ.

2/ Arqplex is a multiplexing deloyment which basically means being able to ensure the availability and quality of broadcast content using cloud-based technology - so like disaster recovery for TV - a way to stop this happening! Whoops!

Arqiva have so far sold 5 systems to ITV and 2 to Paramount. This is being sold worldwide. It was very well received by global broadcasters at a recent Las Vegas trade show, according to Arqiva.

3/ TV Habits - for years people moaned about how much TV we watch. 158 minutes a day is the average. More content is being consumed via the internet, it’s true. But Arqiva seems well entrenched and future focused on those multimedia trends.

Smart Metering

As well as Media and Broadcast, Arqiva has a large Smart Metering business which is growing fast (20% growth y-o-y in 2023) with recurring revenues with:

1.5m homes with water metering

2.6m homes with energy metering

There’s still another 50% of domestic connections plus business and industry. Then we come to Smart Grids. Arqivas’s Hybrid Connectivity Service is designed to support Utility companies with network monitoring and control needs.

In fact the accounts show:

“The smart utilities network products have an order book of £0.7bn (2022: £0.6bn), with contracts running as far as 2050.

What strikes me is that compared to other Smart Meter Providers (SMS, Yu Group) Arqiva offer an awful lot more than sticking a meter in. Their expertise in networks could enable them to dominate this market and add value where its competitors can’t.

It is much easier to build infrastructure when you’ve already been an infrastructure provider for over 100 years.

For example sewer level monitoring is more than a bit of a smelly issue for water companies - Arqiva can help. Leak detection too - guess what yes Arqiva can help here too. Thames Water and Anglian Water have both awarded contracts to Arqiva.

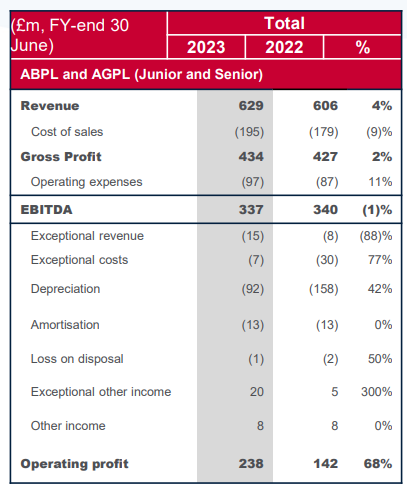

The accounts show a £238m operating profit.

Wait one. In Knives to Digital 9 you may recall we spoke before about Arqiva.

The pro rata EBITDA value we used for Arqiva was £91.3m. But 48.02% of £337m is actually £161.8m. 77% higher than I had assumed.

WOW!

Operating Profit is £238m (of which £114.3m accrues to DGI9). Obviously operating profit removes the concern that using EBITDA for an infrastructure player (where D or Depreciation is significant). In fact good news here. The fall in depreciation you see above, year on year is permanent - where in 2022 some one-off charges were made for legacy equipment being written off, via a Group IT transformation programme.

£114m well affords a £20m dividend. It could afford a £50m dividend. (which was the cost of the previous dividend which would be a 20% yield at today’s prices). It could afford a 44% yield dividend theoretically.

Debt

Realistically paying down debt is also important so before we get too giddy denuding poor Arqiva of cash let’s look at that.

Yikes. So at first glance Arqiva actually lost a whole load of money £606.8m in 1 year alone……. Or did it?

The magic trick is the bit I’ve highlighted. “Accrued interest on shareholder loan notes” refers to the fact that DGI9 and one other shareholder are accruing profits in Arqiva. So this is a form of shareholder funds (by another name). They also award themselves a 13-14% interest so that’s why this “interest” is colossal.

If you strip out that noise, the business owes £1,566.3m (inc. lease liabilities). Still a large amount. The repayment profile means some further refinancing is needed or paid down. So the fact dividends aren’t being paid to DGI9 is no bad thing. Debt costs 7.2% (£130.1m a year) so it’s worth doing. There are, too, hedges to complicate the world but we know from DGI9 the effect of these disappears in 4 years.

Net assets - again once you strip away the Shareholder loans and accrued interest the business has £855m of net assets.

Adjusted Net Income - In fact if you take operating income (£238m) and remove “real” interest and lease costs (£130.1m) gives you a more accurate income figure of £107.9m If you take DGI9’s share (48.02%) that’s £51.8m a year.

So we are back to DGI theoretically being able to take dividends which would afford it to restore its 6p a share - i.e. its 20% dividend - based on Arqiva alone.

Penultimate thought:

Very odd structure to Arqiva’s accounts. However Arqiva pays no corporation tax as a result. Unfortunately, a financially illiterate investor could reach the wrong conclusion about Arqiva.

Valuation

The deep dive has confirmed a couple of things.

Arqiva is as exciting a holding as I thought. In fact more so.

Let’s consider the recent news about fellow smart meter provider Smart Meter Systems (SMS) being acquired. Let’s consider what that means for Arqiva. For a start Arqiva’s smart metering is almost double the size of SMS. (£110m vs £189m of ILARR - I’m being generous and including traditional meters in SMS’s £110m… Smart Meters are £70m actually). Arqiva have 25% market share of UK Smart Meters versus SMS who have 14%. SMS was bought at an EV / EBITDA multiple of 20.0x (calculated based on LTM Pre-exceptional EBITDA of £71 million as of June 2023).

By comparison Arqiva has an EV/EBITDA of 11 (£3,714.2m/£337m) - again stripping out all the shareholder loan note stuff, so that implies that Arqiva could be worth £6.74bn (£337m x 20). If it were to occur, that would equate to a £1.45bn gain to DGI9….. or £1.68 per DGI9 share.

(Note SMS have a EV car charger, a BESS and energy services business whereas Arqiva have a Media & Broadcasting business so you may disagree the same valuation methodology should apply…… in my opinion Arqiva’s other business is at least as valuable as asset as its Smart Meter business)

The growth plans and the tailwinds it address along with the stability of utility like RPI linked income make this attractive indeed.

You could buy the whole of DGI9 currently for £255m and own 48.02% of what looks to have £855m of net assets - so a near 50% discount to NAV. With a takeover potential which would take it to 90% discount to NAV…… And that’s ignoring all of DGI9’s other assets.

On Arqiva alone, DGI9’s current share price makes no sense.

The fact DGI9 has fallen in price maybe its people simply not understanding the assets and holdings. Or maybe the world have grown desensitised to “Discount to NAV” and assume such numbers are hocus pocus. Just snares to entrap the unwary.

This is not advice.

Oak

Interesting result of the strategic review today. ....

Hi Oak, thank you for the analysis; sometimes markets don't get it...i didn't either ....or the market is implying derteriorating operating metrics for Arqiva and thus a deteriorating credit outlook.

Is there Arqiva debt trading publicly to see how the corresponding yields have evolved?

Anyway thank you for your writings , which are always presented in an entertaining fashion...

Saludos from Cadiz