Eye-say!

Dear reader

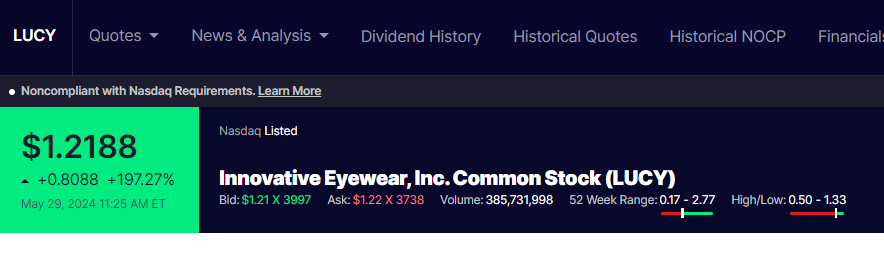

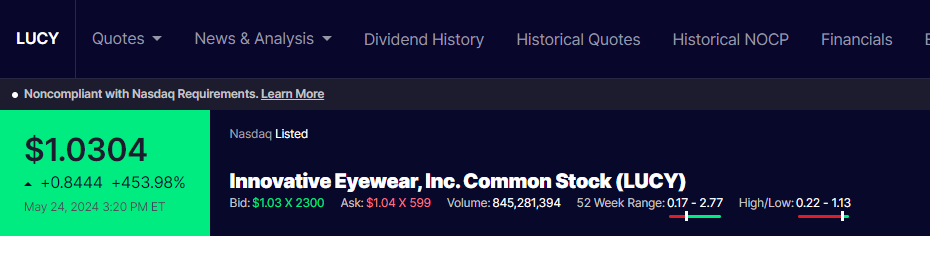

As I write this it would appear LUCY has become the latest meme stock. With “Dollar Lucy” a trending tag. I’m not complaining. Although I did complain about progress in the recent Q1 update.

Up +378% as I write.

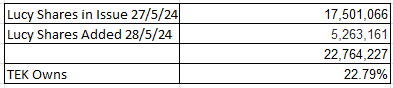

TEK owns 29.65% of LUCY so this rise means an extra 1.5p or so per TEK share. See my NAV analysis later.

Aside from memes, it was announced by the CEO Lucyd’s launch of Eddie Bauer is imminent. The Eddie Bauer glasses look extremely impressive. This launch video was released 3 weeks ago. As a happy owner of two pairs (one for me and one for the Oak Gal), I am tempted but, no, another pair would be greedy. Wouldn’t it?

CEO Harrison Gross confirms Eddie Bauer is imminent but also goes on in his interview to tell us that Reebok is “a few months away”, and “Armor”, its safety glasses range, too. With 3 major brands, powered by Lucyd as well as the Lucyd brand itself plus a unique product for industrial users if these are all in play in 3Q24 then the necessary revenue growth could follow.

Gross actually makes a lot of good points in his video about the benefits of smart glasses too. Privacy (compared to always listening - snooping - Meta glasses), induction volume is far safer for your hearing compared to in-ear headphones and air pods, as well as the market-leading 12 hour battery life (I have done all day hikes listening to podcasts with my Lucyds so my iphone gives out before the glasses)

Plus they are comfortable, and cool.

29th May update:

The price of LUCY triples today.

Eddie Bauer launches - presumably has the masses eager to buy.

A $2.5m capital raise yesterday comes shortly after another for $1.025m. The additional 5.2m shares at $0.475 means TEK’s holding in LUCY drops to 22.79%.

With $2.6m at 31/3/24 and $3.525m raised that’s $6.1m cash. Against that a cash burn of $0.5m a month from operating activities gives another 10 months runway - roughly from now at the end of May 2024. That assumes no investing activities or other financing activities. There are 5.2m warrants which could raise a further $2.5m today or soon.

But it is a near certainty that investing into Armor as well as Reebok will drain further cash. Countering that if the Nautica and Eddie Bauer franchises as well as core Lucyd sales can drive sales as well as if the cost of sales can be brought under control there remains a path to break even and profitable growth.

Clearly the meme rally showed one thing - LUCY has captured the imagination of American investors. It appears a new phenomenon has occurred. As soon as LUCY releases positive news the Memesters return in their droves.

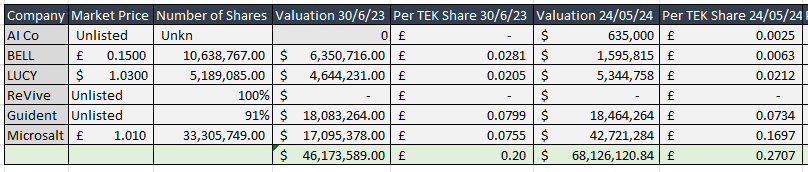

Meanwhile TEK’s NAV is 27.2p per share including 20p/share of LISTED holdings.

Microsalt

Another TEK holding is Microsalt. This week Microsalt has had a strong week with some consolidation today.

Today, too, Microsalt has activated its warrants. This is £3.4m of funds for Microsalt assuming all warrants are exercised. Holders have 2 weeks to decide. There are 2,753,507 undisclosed warrant holders but around 4.5m warrants are held by insiders. Exercising their warrants will be a vote of confidence.

If TEK wants to exercise its 2,558,140 warrants it will have to:

a/ Find £1.2m b/ At least 2.6m non-TEK warrant holders will need to exercise their warrants too (because TEK agreed not to increase its percentage ownership of SALT.

Assuming Microsalt’s share price remains at £1.01 then TEK would spend £1.2m to own an asset worth nearly £2.6m i.e. a cool £1,373,721 profit. (Or £0.6m more if SALT returns to £1.40)

Even at £1.01 per SALT share, £1.3m equates to a 0.7p per TEK share gain for TEK-kies.

The SALT IPO raised around £3m of funds so there must be a purpose for these additional funds by triggering the warrant.

The likely answer is sales & marketing and working capital. £3m won’t quite buy and fit out a factory. This warrant raise suggests there is imminent news in the offing. Why would SALT need extra working capital, reader?

Patent Granted

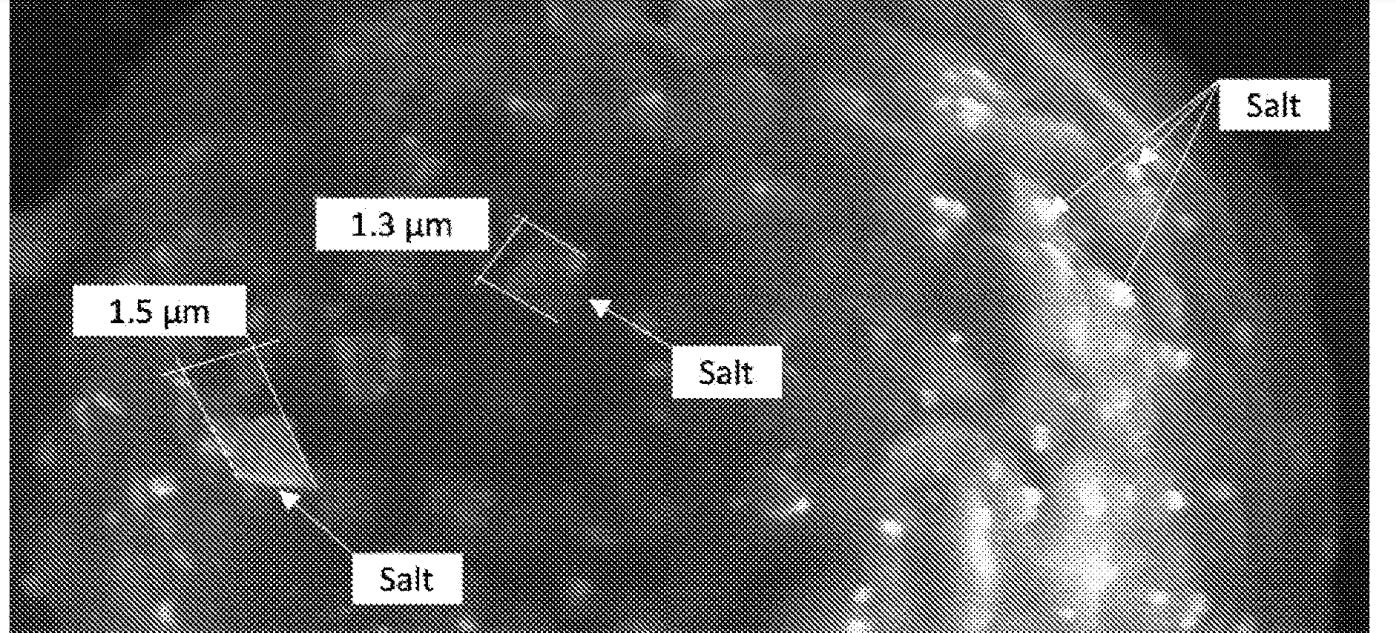

Meanwhile on the 15th May SALT was granted US patent number 11992034 “Low Sodium Salt Composition”

This patent is the technique of using a big particle (Dextrose) and then “sticking” little salt particles (as in less than 2 micros) on to it as can be seen in this magnified picture.

Let this sink in. No one can use this technique to reduce salt in food. That’s what the patent means.

What’s more this same (US) Patent is pending in China, Chile, Australia, Brazil, the EU, Canada, Japan, Russia, Mexico, India and Hong Kong.

No wonder the share price has increased - a major risk (not getting the patent granted) has gone away. The US market alone is enormous but there’s no reason to think the pending won’t be granted. It genuinely is a unique approach that required certain humidities, pressure, particle sizes and “know how”. Replicating this is not straight forward even if it weren’t patent protected.

The need for Microsalt is colossal. Look at the causes of death and tell me what percentage were due to or contributed to by excess salt. About 77% by my reckoning. Yet media coverage (at least in 2016) focused on other things.

The application runs beyond salt shakers, because another pending patent is for use in Baking. If you actually track your salt consumption many people realise bread products and ready meals are two of the main culprits why 5g of salt is very difficult.

Lower sodium bread and bakery products also means faster cooking (meaning a better nutritional profile and lower energy costs). The baked goods market is worth half a trillion dollars ($500,000,000,000) a year worldwide. Microsalt could dominate this as an essential go-to ingredient, much like today we might buy wheatgerm rather than white bread. Imagine having a monopoly on wheatgerm.

This is my forecast analysis of Microsalt. Previously I mused:

I can see a path to value where the whole thing easily gets taken out at £50-£100m by a large foodco.

Well SALT has already achieved that. Today it’s £44m and earlier this week its market cap was around £60m.

A £75m cash buy out would give a 73% upside to SALT holders and TEK meanwhile would get cash equivalent to 29.7p per TEK share.

That cash could be used for commercialising Guident, ReVive, the new AI Co as well as a special dividend. If 10p-20p were being handed to shareholders you have to ask would the share price be 11p?

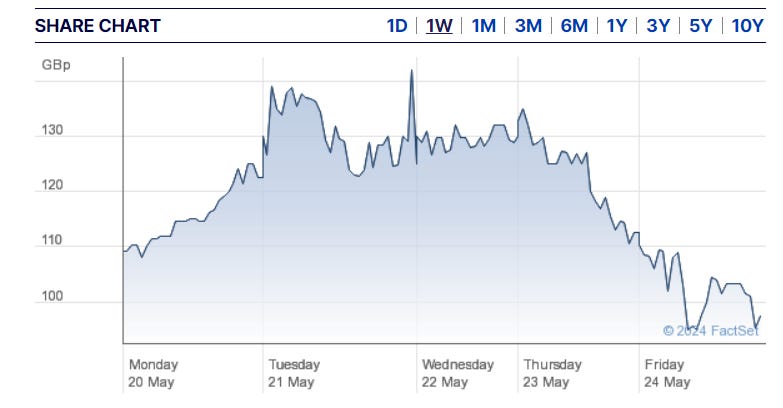

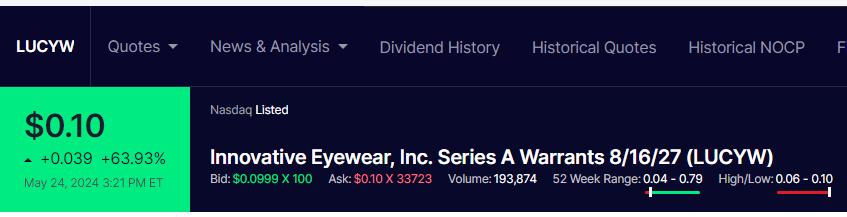

I’ve just checked back on LUCY and she’s broken the $1 barrier. There’s no need for a share consolidation, if this holds above a buck. The warrants are up 64% too (suggesting people are willing to pay for the right to buy stock at $3.75)

TEK’s NAV as at 24/05/24 (8.23pm BST) is 27.07p vs 11.5p buy.

A 57.5% discount where 2 of its 5 holdings have enjoyed meteoric rises this week. Bonkers.

I wish you a pleasant bank holiday weekend.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"