Introducing Microsalt - SALT - Part of TEK

Is it worth joining the IPO?

Today people woke up to something strange and unusual. A UK IPO.

I jest. It’s not that unusual. In fact there’s many exciting IPOs in Q4 2023 - including in the UK.

What about Microsalt, which is part of the TEK portfolio - and its 3rd IPO? If you dig into the PrimaryBid documents there is no definitive pricing or valuation…. yet. But let's try to work out what those numbers will look like.

I will update my overall TEK valuation titled Cliff doing a CliffHanger once I’ve completed this article on Microsalt

The NAV in TEK’s books is currently $17,624,102 as at 30/6/23 and TEK owns 97% of Ltd valued at $17,095,379. The “Ltd” owns 79% of the LLC valuing the US Business at $22,308,989.

It is the LTD which is being IPO'd. It is a hold co. It is the LLC where all sales and operations occur.

Meanwhile the prospectus speaks of raising £12m-£15m of funds ear marked for the below activities. Those values equate to between $14.5m and $18.3m.

"Usually" an IPO will be at or above the NAV.

"Usually" TEK has retained an interest (Skin in the game). Let's assume TEK intend to do the same as BELL i.e. TEK wants to retain 15% post IPO I say “usually” because nothing has yet been decided (or at least made public).

There are 3 scenarios:

a/ The “£20m” float. This is where £15m ($18.3m) is injected into Microsalt and £5m kept by TEK. This is what I believe is the redacted number in the prospectus - if the market can support that valuation. And more on that later.

b/ The “£15m” float. That is where the NAV of $17.1m x 85% = $14.5m worth of shares where the "aim" is to float at a 26% premium to NAV. (to receive $18.3m or £15m).

c/ The “£12m” float. That is where the NAV of $17.1m x 85% = $14.5m worth of shares where the "aim" is to float at a 0% premium to NAV. (to receive $14.5m or £12m).

£2.5m Primary Bid (option A or B)

Today (3/10/23) the Primary Bid offer has been revised to clarify it is to raise £2.5m concomitant with the IPO. Concomitant means alongside.

£2.5m is easily divisible into £20m or £15m.

A 22% dividend? (option A):

I would remind readers that TEK has spoken in the past of special dividends for its beleaguered shareholders. £5m would pay everyone a 22% dividend at today’s market price.

But I’d also point out the obvious fact that the extra £5m might be better used to support LUCY, BELL, GUIDENT, ReVive, its Corporate Activities with Universities or even to fund a 6th portfolio member. I ponder on what that might look like in my Cliffhanger article too.

I don’t believe a cheeky 22% payback is on the cards. Read section 14 of the prospectus relating to Lock In and Orderly Market - 12-24 month lock in for TEK.

So what will the IPO mean for TEKkies? Will it be another BELL or a LUCY, or something else entirely?

Well, at the £20m top end valuation each shareholder gains a 4p a share payout, or 4p of cash to fund stuff. Meanwhile the NAV of Microsalt increases by 2p a share. (7.86p/tek share to 9.86p/tek share).

At the £15m valuation TeKkies gain 2p (7.86p NAV/tek share to 9.86p NAV/tek share).

At the £12m valuation, option C at the bottom end, the NAV is static at 7.86p NAV/TEK share.

Why will people pay for Microsalt? Should I participate in Microsalt?

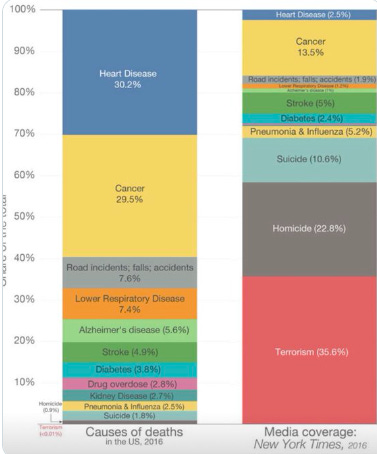

FACT#1 - The need for Microsalt is unparalleled.

Heart disease causes approximately one in three deaths globally: that is 17.9 million premature deaths each year, 50,000 each day, or one death every 1.7 seconds.

This infographic puts it in context. The problem is 12 times larger than most people probably read about.

Think I’m right in saying salt doesn’t help with Cancer (29.5%) or Stoke (4.9%) either, and probably some other leading causes of death too. Probably can’t blame too much Terrorism or homicide on salt consumption.

In the US alone, one person dies every 34 seconds from cardiovascular disease. Each year, cardiovascular disease costs the UK £19 billion – if the average salt intake was reduced by one gram per day, it has been estimated that 4,147 lives and £288 million would be saved each year in the UK. As a nation, the UK consumes 183 million kilograms of salt each year, and 70 percent of the typical person’s sodium intake is hidden in processed foods. There is a proven link between excess sodium consumption, high blood pressure and cardiovascular disease, which is the leading cause of death worldwide. It is estimated that 1.28 billion adults have hypertension globally. The WHO has stated that reducing sodium intake is one of the most cost-effective ways to improve health, as it can avert a large number of cardiovascular events and deaths at very low overall programme costs.

FACT#2 - There is no competition.

Potassium-based salt is said to taste bitter & unpleasant. I went out and bought some to determine whether that was true. It wasn’t intolerable but I could taste a metallic taste.

FACT#3 It ain’t just about the salt shakers or the salt’n’shake.

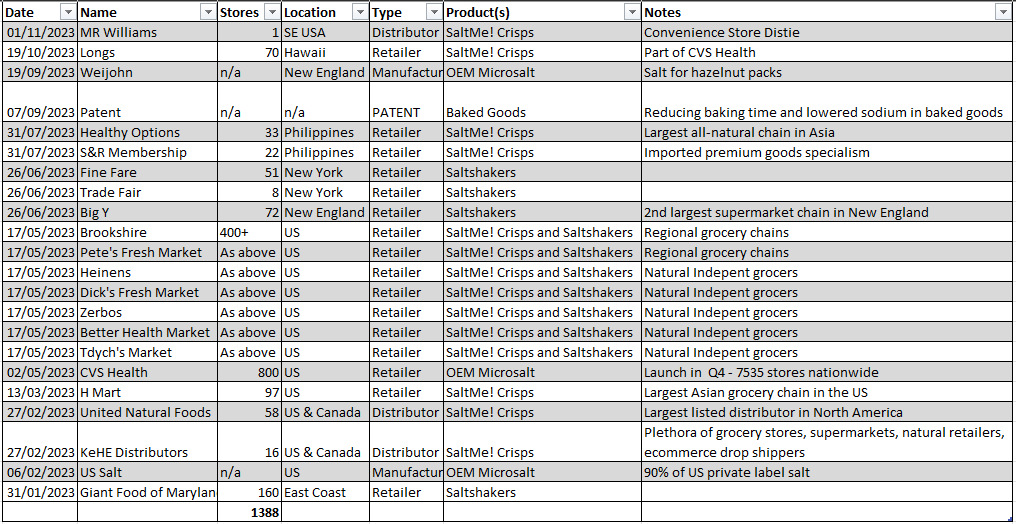

If you have read TEK’s update Microsalt’s B2C products are familiar (Salt Shakers and Potato Chips aka Crisps). We know they are stocked in 100s of Health Food Stores in the US, on Amazon US, and soon Amazon UK. Also a white label (no pun intended) deal with US Salt who supply 90% of private label salt.

The entire newsflow and focus has been on Microsalt’s B2C Sales Efforts. But Microsalt also has a B2B programme. Has this moved much further along than people realise? The prospectus reveals huge deals in progress.

To quote the Group currently has:

“various significant volume customer prospects at advanced stages with a range of national and multi-national companies. The nature and size of these existing and potential customers businesses is that once [Crystal] has been nominated as a supplier on one product line, the Directors expect further nominations across multiple other, and likely much larger product lines of that customer. “

Customer A (I believe this to be CVS Health which has 9,545 stores - noting too the RNS 19th October that Longs Drugs is selling SaltMe! crisps. These are part of CVS)

Customer A has identified numerous of its private label products which they are keen to substitute traditional salt with [Crystal]. The initial product rollout relates to four nut SKUs in approximately 800 stores in the US. The Group has commenced production of [Crystal] to be supplied for these private label products, with finished products expected to be on Customer A’s shelves in September 2023. Furthermore, it is expected that Customer A will sell [Crystal] shakers alongside products on end of shelf space from quarter one of 2024. The Directors expect both the SaltMe! Crisps and the shakers to be further rolled out across a significant number of Customer A’s 9,000 store estate in 2024.

Customer B and Customer C (I believe this could be Pepsi Co who operate extensively in LatAm)

Although separate entities, Customer B and Customer C operate under the same group and form one of the largest food, soft drink and snack manufacturers in the world. Following the achievement of global approved vendor status in November 2022, the Group recently advanced its commercial relationship with Customer B with the delivery of an initial 9.5 mT purchase order.

Continuing monthly orders of 9.5 mT (I think this refers to 9,500 tonnes of Microsalt) are expected, with a supporting purchasing agreement anticipated before the end of 2023.

Further line additions are then expected to follow in the first half of 2024 across multiple leading brands of Customer C. Discussions are progressing across several other geographical markets and the Group is currently negotiating a purchasing agreement for the Mexican and Latin American Markets. At the same time, discussions are ongoing relative to North American and global expansion. The Company is also negotiating a JDA to facilitate the coordination of additional product innovation and development opportunities in quarter one of 2024.

Sodium Reduction is one of PepsiCo's highest ESG priorities:

"We’re making sure to offer nutritious options that consumers are seeking, while still providing the same great taste. Our nutrition goals align with two of the United Nations’ sustainable development goals — Good Health and Well-Being, and Zero Hunger — and we help to work towards a future without malnutrition, hunger or food insecurity.

Customer D

The Group has been accelerated through Customer D’s R&D channels following positive sample and production results. [Crystal] has been confirmed for use in a rolled corn tortilla snack and an initial purchase order is expected by management in mid-2024. At such time, management expect that Customer D will release a joint press release citing [Crystal] as a key pillar of their low sodium solution(s).

Customer E

The Group is currently in the planning stage with Customer E, with samples of [Crystal] being sent for testing across several frozen food items in April 2023. Customer E already has an active low sodium initiative and initial orders are expected in April 2024.

Other Customers

On top of these there are already 3 Manufacturer/OEM agreements, 75 Distributors and over 1,300 retailers selling Microsalt products, based on public news announcements during 2023.

FACT #4 what if the technology ain’t just about salt products.

The fact that Microsalt can be used in Bakery combined with Maltodextrin, means lower sodium bread and bakery products as well as faster cooking (meaning a better nutritional profile and lower energy costs)

The baked goods market is worth half a trillion dollars ($500,000,000,000) a year worldwide.

What’s the value of this to Microsalt? This recent science article speaks to achieving reductions of 0.3%-0.6% but what if you could achieve 10 times that?

FACT #5 what if the technology ain’t just about salt

What about the underlying “nano flavour” technology itself? Will we in time see Micro-sugar? Micro-flavourings?

Saffron is more expensive than gold. Imagine you can make a Paella twice as fragrant with the same amount of Saffron.

Flavourings is another $39bn market:

https://www.statista.com/topics/6300/flavor-and-fragrances-market-worldwide/

Sugar is another $76bn market:

https://www.researchandmarkets.com/reports/5562693/global-sugar-market-size-share-forecast-2022

One where food manufacturers are struggling to balance reducing sugar and compromising taste:

https://foodmatterslive.com/article/sugar-reduction-food-firms-miss-voluntary-targets/

How do you value Microsalt?

You saw my “upper estimate” is £20. Why? Well MicroSalt’s pre-money valuation is £20m.

£20m is in line with TEK’s discounted cash flow forecasts based on a compound annual growth rate of 129% and (an exceedingly high) discount of 16%

£20m is also the price at which TEK converted its most recent CLN in November 2022.

Is a £20m valuation the upper limit? Well, much has happened since this valuation:

a/ Huge B2B deals in progress (Customer A-E)

b/ Microsalt’s potential for baking and other applications.

c/ Celebrity endorsement

I’ve maintained for a while that TEK shares are undervalued based on the facts. As a TEK holder you own something worth 7.86p/TEK share now (based on book value), or 3.8p/TEK share based on market price. The NAV (if not the market price) could increase by 5.24p a share (13.1p total), if the IPO is at option A at £20m.

Or an increase by 2p/TEK share (9.86p total) if it’s option B and moderately successful (i.e. £15m)

Or you get 7.86p/TEK share of your NAV on a listed basis if it’s option C (£12m).

In the future, I can see a path to value where the whole thing easily gets taken out at £50-£100m by a large foodco. In that scenario a TEK holder with 15% you’d get a 25p-47p/share gain.

As a Microsalt holder your upside would be much higher. Assuming a £15m float it’d be a 3x bagger or a 6x bagger.

Why would someone pay £100m? Is that not just a mad guess? Well think of it from a buyer’s perspective. Low salt is a powerful USP. A holy grail. Low sugar if that’s possible too.

When annual sales are in the $ billions (e.g. PepsiCo made $86bn sales last year) if you can grow those by 10% that’s $8.6bn of extra sales. If you can make your products less harmful you massively win on the ESG front. Plus people may consume more of your product. Food is a guilty pleasure. Think about how they advertise foods. Then think of the consequences of healthier foods. Crisps with half the salt - I can now eat double the crisps without feeling guilty!

These views are my personal opinion, not advice. Written to set out the facts for my own current and future investment decisions in TEK and SALT. I hope you enjoy reading my posts and good fortune in your own investment decisions.