Fair €aks Income

April 2026 update

Dear reader

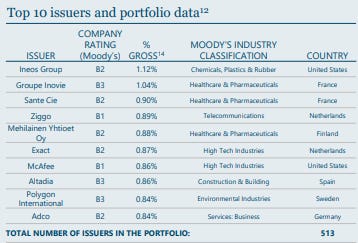

Fair Oaks (ticker LON:FAIR) is one of the OB picks from 2024 that continues to deliver bags of Cash. FAIR is a collateralised loans manager where the underlying debtors are Corporate businesses like McAfee, Ineos and Exact plus hundreds of others you’ll probably have never heard of. To buy FAIR you need to prove you’re a sophisticated investor so spruce yourself up reader, if you choose to partake.

Two months ago in “Fair Euro-Nough” I described a watershed moment, and a pivot to a higher quality, more defensive European position. Where are we today?

On April 30th, shareholders voted an overwhelming Yes to change the reporting currency and to carry out a 10-to-1 consolidation of shares. To understand why this re-coring matters, we have to look back at the dramatic rollercoaster ride of February and March that set the stage for April’s rebound.

Section 1: The March Disconnect (When Mr. Market Lost His Mind)

Let’s look at what happened when geopolitical tensions boiled over in the Middle East and fears over AI hitting the US software sector sent retail investors scrambling for the exits.

In March, US software loans got absolutely hammered, trading down to a miserable average of $0.88. Panicked investors saw ‘CLO’ and sold everything. Look at what it did to FAIR’s share price vs. its actual underlying value:

Share Price: Plunged an ugly -9.4% in March, dropping down to $0.424.

Underlying NAV: Actually rose +0.30% to $0.475!

Because of this emotional decoupling, the discount to NAV ballooned to an eye-watering -11.02%.

But as smart income investors, we look under the hood. While the US market was sweating over high-tech exposure, FAIR was sitting pretty in Europe. European CLOs only carry about 10% software exposure compared to 15-16% in the US. Furthermore, FAIR’s internal CCC-credit exposure sat at a fundamentally safe 3.28%—miles away from the restrictive 7.5% threshold that triggers cash traps.

Management quietly walked away from a US CLO warehouse that didn’t meet their return thresholds, doubling down entirely on expanding their European footprint. The business didn’t change; only the market’s mood did.

Section 2: April’s Rebound & The Tight Euro-Pricing

Fast forward to April, and the tables turned. A massive global risk rally—spurred by blockbuster US earnings and an electronics rebound—dragged leveraged loan markets back into the green.

The result for FAIR?

NAV rose +2.17%

Share price surged +6.13%

The discount snapped back from -11.02% to a smaller -7.31%.

But the real magic happened in the primary markets. On May 4th, right after the April books closed, the Master Fund anchored a brand new €381m European CLO: Fair Oaks Loan Funding VII.

This is where the competence of the manager shines. They priced their AAA liabilities incredibly tightly at just 130bps over Euribor, bringing their blended capital costs to 174bps. Compare that to the broader market average of 182bps for deals pricing that same fortnight! Because they locked in cheaper liabilities while buying discounted secondary assets, they expanded the structural arbitrage window. Even better? FAIR locks in a 4.5-year reinvestment runway out to 2031 for Fund VII.

Section 3: The New Euro Era — What the Maths Looks Like Now

Now that the April 30th resolutions have passed, your broker statement is going to look a little different.

First, the company has executed a 10-for-1 share consolidation, clean-cutting the penny-stock optics. Second, everything is officially moving to Euros (€).

Let’s look at the clean, post-restructuring April numbers:

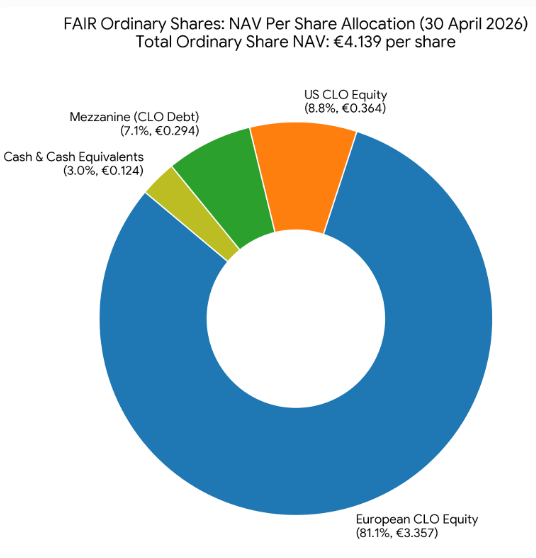

Post-Consolidation Price per Share: €3.84

Post-Consolidation NAV per Share: €4.14

The Cash Harvest: April was a quarterly distribution month, bringing in a massive €8.5 million in cash to the Master Fund—equating to a robust €0.21 per share for the quarter. (So about 5% of the market cap)

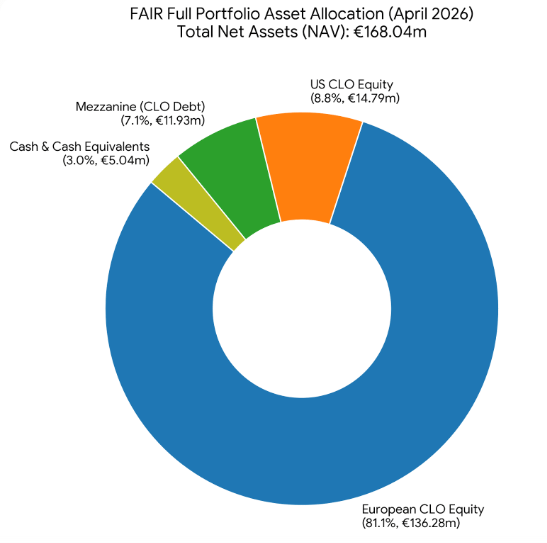

By alignment of the reporting currency directly with the asset base (90% Euro vs 10% USD), FAIR is stripping away the deadweight loss of FX hedging contracts. What you see is finally what you get.

#1 US CLO Equity

The 4 months of 2026 data proves that while US software concerns did cause a spike in stressed loans with assets under 80c peaking in March at 3.28%, but falling in April to 3.23%, the portfolio didn’t suffer any material defaults holding flat at a 0.03% weighted average default rate.

FAIR sold off a chunk of its weak CCC-rated loans dropping it from 3% to 2.4% keeping it away from the 7.5% trigger where quarterly cash gets diverted from FAIR. It also expanded its “over collateralisation” cushion (i.e. its safety buffer of assets less liabilities) to 5.1% so higher than at the end of 2025!

Cash yields are at a mouth watering 28.5% weighted average.

#2 The Death of the US Warehouse

Earlier in the year, Fair Oaks was actually testing the waters for a move into US Mezzanine debt. They were running a dedicated US investment vehicle known as the BSP CLO Warehouse 2025-3.

Warehouses are temporary, short-term setups used by managers to accumulate US corporate loans before bundling them into a formal, long-term CLO vehicle (where they would typically buy the BB or B-rated Mezzanine tranches).

However, when the market became highly volatile in February and March, credit spreads widened significantly. Rather than forcing a bad deal in an unstable market, management executed a defensive pivot: they completely liquidated and shut down the US warehouse.

Management explicitly confirmed this move to the market:

The Master Fund does not expect any significant impact on NAV from the US warehouse liquidation and currently expects to reallocate the capital proceeds into CLO debt at attractive levels.

#3 European CLO Equity

Stressed loans dropped by a huge 4.83% down to 3.37% in April 2026. Defaults have been zero for all of 2026. The over-collateralisation (safety margin of assets minus liabilities) grew to 4.2%, again higher than at the start of the year.

CCC-loans fell to 3.22% in April from 3.28% in March too.

Annualised Cash yields for Euro CLO Equity are running at a storming 32.9% which is 3.2% more than at the start of the year.

#4 European Mezzanine Loans

Mezzanine assets are traded debt bonds and their market valuations fluctuate based on interest rate expectations and systemic risk. The total weighted average valuation of the EUR Mezz book (measured as a % of par value) tells a clear story of active accumulation during a market dip:

January (95.0%): The year began with the mezzanine notes trading at a steady, high-quality discount of 95 cents on the dollar.

February (94.0%): When the broader market panicked over Middle East oil shocks and US software tech downgrades, institutional investors dumped riskier debt. Fair Oaks used this dip to accumulate assets.

March (93.4%): Prices hit their absolute bottom for the year. This 93.4% valuation represents the exact moment the manager finalized the liquidation of the US warehouse, rotating the cash into these temporarily mispriced, discounted European notes.

April (95.3%): As global risk markets staged a massive comeback, the mezzanine book experienced a powerful price recovery, surging to its highest valuation of the year.

In April, the trailing 12-month loan default rate declined modestly from 1.4% to 1.3% in the US and remained unchanged at 1.4% in Europe. The distress ratio improved in both regions, falling from 7.8% to 6.3% in the US and from 6.6% to 5.5% in Europe.

FAIR’s mezzanine performed well ahead of that 1.4% rate at 0.24%

FAIR flushed out distressed (sub 80c) debt in April, again to levels below the start of 2026.

By April the average collateral bid price inside these 14 vehicles bounced back to €0.97, soundly beating the broader European market baseline of €0.945. The over-collaterisation cushion was 4.41% in April so at a strong level.

There is also a move into defensive verticals like Healthcare as well as those with real assets and out of software and high tech.

Because these mezzanine notes pay a floating coupon tied directly to Euribor, they provide protection against sticky inflation and shifting interest rates. They are currently generating an average EURIBOR +8.16% meaning a 10.89% yield in April.

If we compare the 4 months we can build a picture that looks like this:

Act I: January 2026 – The Calm Before the Storm

The Macro Mood: Optimistic and steady. Management noted that trailing 12-month loan default rates were flat and highly manageable at 1.4% in both the US and Europe. Global credit markets were functioning smoothly.

Management’s Focus: They were hunting for incremental yield and expanding their footprint. At this point, they were fully committed to testing the US waters via the BSP CLO Warehouse 2025-3, trying to build a new dollar-denominated engine.

The Behind-the-Scenes Reality: The fund was still paying massive amounts of money to Wall Street banks to run cross-currency hedging contracts because their assets were in Euros but their public listing was in Dollars.

Act II: February 2026 – The Double-Shock Hit

The Macro Mood: Sudden anxiety. Two major thematic roadblocks emerged out of nowhere:

The AI Tech Panic: US credit markets began aggressively marking down software company loans over fears that generative AI would disrupt their business models.

The Geopolitical Oil Spike: Late-February saw heavy US and Israeli military strikes on Iran. Brent crude oil suddenly spiked, throwing global inflation and interest rate expectations into chaos.

Management’s Focus: Insulation and Defence. Management immediately used the commentary to reassure investors that their core European strategy shielded them. They pointed out that European CLOs carry significantly lower software exposure (~10%) than US packages (15-16%).

The Big Move: Recognising that the US credit environment was turning toxic, management didn’t hesitate. They chose to freeze and liquidate their US CLO warehouse, taking their chips off the table before getting burned.

Act III: March 2026 – Retail Panic & The Corporate Pivot

The Macro Mood: The peak of emotional market dislocation. Trailing default rates stayed totally stable at 1.4%, but “distress ratios” (the number of companies showing minor financial stress) spiked heavily to 9.2% in the US and 6.7% in Europe. Oil peaked at a staggering $118 per barrel on March 9th before cooling off (for now).

The Disconnect: This was the month retail investors on the London Stock Exchange panicked, selling off FAIR shares and widening the NAV discount to an absurd -11.02%.

Management’s Focus: Going on the Offensive. In the commentary, management calmly explained that the wider market volatility was actually good for existing CLO equity. Why? Because they were locked into cheap, historical financing costs, but could use fresh cash to buy up underlying corporate loans at massive, panicky secondary-market discounts.

The Catalyst: On March 19th, tired of watching the US Dollar listing muddy their financial realities and impose heavy hedging costs, the Board officially proposed the complete corporate restructuring package to drop the Dollar, switch to the Euro, and consolidate the shares.

Great harumphing was heard when they reset the dividend too, although it makes sense for a fund to live within one’s means so a move from $0.02 per quarter to €0.01 per quarter made sense to me and the expected return is still ~12%. The resulting sell off was an opportunity too and today at €4.00 a share FAIR remains cheap while the gross return to call is 19.3% and is quite a bit higher than the forecast yield at the start of the year.

Act IV: April 2026 – The Great Vindication

The Macro Mood: Complete risk-on euphoria. Blockbuster US corporate earnings pushed the S&P 500 up nearly 10% in a month. The Iran conflict cooled to a double blockade and an uneasy stalemate, dragging oil back to $100. Leveraged loan indexes roared back into the green, and distress ratios plummeted across the board.

Management’s Focus: Victory Laps and Capital Deployment. The commentary shifted to an incredibly confident tone. On April 30th, shareholders voted a resounding YES to all corporate restructuring plans, permanently moving the fund to a clean Euro footing and ending the FX hedging drain.

The Power Play: Management proved their institutional clout on May 4th by pricing a massive new €381m European CLO (Fair Oaks Loan Funding VII). Because market conditions had stabilised, they printed their senior AAA debt at an incredibly tight 130bps over Euribor, securing an ultra-cheap blended financing cost of 174bps—crushing the wider market average of 182bps.

Conclusion

Periods of market dislocation are precisely when defensive, active CLO managers thrive. While the market panicked over US tech debt and Middle East oil spikes, FAIR maintained a high-quality collateral bias, keeping average portfolio loan bid prices (€96.8c) comfortably ahead of the wider European market baseline (€94.5c).

With an annualised inception-to-date NAV return of 9.0%, the removal of USD hedging friction, a fresh 2031 reinvestment engine in Deal VII, and a discount that is still serving up a decent margin of safety (although to be fair not an unlimited margin of safety and risks of course exist), FAIR’s gone through a short-term sticky patch and profited from that volatility and looks structured to keep generating attractive cash distributions.

The structural repair is done. The currency mismatch is gone. It’s safe to say this portfolio is looking more than FAIR Euro-nough.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

I like this one and own some. However I take issue with this language:

"The fund was still paying massive amounts of money to Wall Street banks to run cross-currency hedging contracts because their assets were in Euros but their public listing was in Dollars."

It make perfect sense to denominate in Euros if most of the assets are in Euros but the hedging costs should not be all that 'massive', I wonder if they have disclosed them but unless they are singularly clumsy it should be pretty tiny compared to the yields they are receiving. I'd guess 0.1% per annum. Anything more should be just the yield difference between the two currencies and not a genuine cost.

I can envisage a scenario in the not too distant future where they might decide there is more opportunity in the US market than in Europe. Will they redenominate again?

Thanks for taking the time to clearly explain what's been goin' on with FAIR. I continued to add on the drops but with hindsight, without fully understanding the changes they were making. Hopefully this can now sit in my SIPP being productive and unnoticed!