Dear reader

In last week’s article I covered hidden value in Grow the Revolut-ion where the confluence of the Forward Partners merger, recent fundraising, available credit and the prospective sale of two holdings Perkbox and Graphcore could soon lead to a Molten Ventures (Ticker:GROW) warchest of £195.5m (equivalent to 44% of the market cap of £440m)

But I was reflecting on other progress at Molten Ventures, following their 2024 Investor Day event. The double discount at Molten niggles at me. Is it real? I was therefore astounded to listen to CFO Ben speaking to how their internal audit committee review what is fair value, then PWC validate that, but Deloitte then come in and validate PWC’s work. So a triple audit as well as a double discount!

So a triple audit as well as a double discount!

You might wonder how the discount to NAV is therefore as large as it is. 67% according to MorningStar.

but I calculate it at 65.5% (MP £440m / NAV £1,274m)

So £834m of assets “for free”.

But that’s just one of the discounts. Here’s the other:

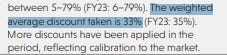

33% is applied, on average, to the GROW assets. For example in my article GROW’s Revolut holding is based on a $19.5bn valuation while other investors like Triple Point valuation use a $23bn valuation. This is what I meant by GROW’s self-flagellation.

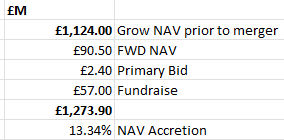

So taking the 30/09 £1,124m NAV for GROW is actually +£553m to arrive to £1,677m NAV plus the FWD NAV and fundraise gets you to £1,826.9m.

So the “fair” discount to NAV is therefore 75.9%. (440/1826.9)

And if you strip out the £195m prospective cash then GROW is at a 85% discount to NAV. (245/1631.9)

85% means you pay £2.32 for a GROW share, you get £1.03 back in forecasted cash, so you’ve paid £1.29 net. You still hold £8.63 worth of companies.

….

I also began wondering about post period activity…. here’s what I found:

NB: these portfolio companies were also covered in GROWing pains

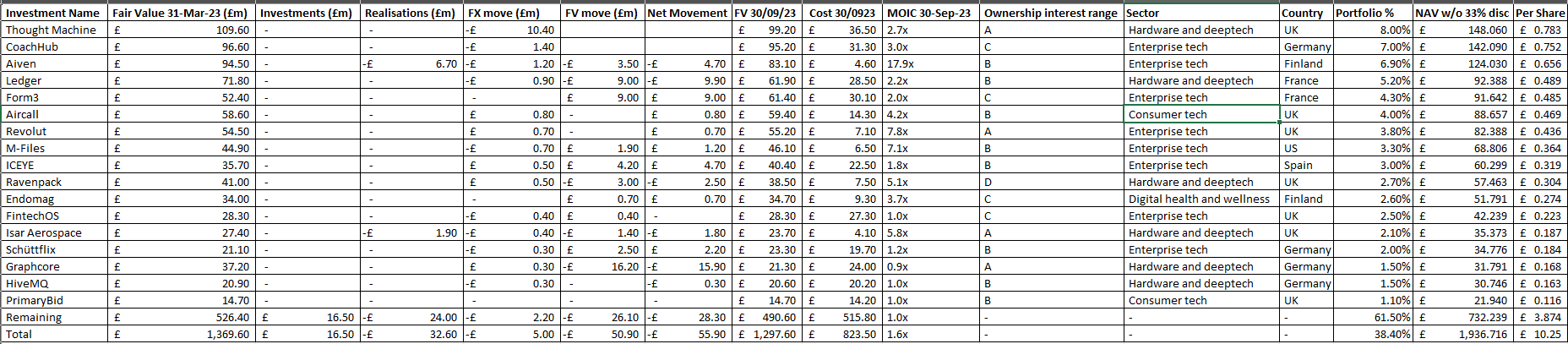

#1 - Thought Machine - NAV is 78.3p per share

A 2023 study by the Boston Consulting Group says fintechs currently have a mere 2% share of global financial services revenue, but are estimated to reach $1.5 trillion in annual revenue by 2030, constituting almost 25% of all banking valuations worldwide. 12X.

Fintech Thought Machine who build banking software appear to be progressing well with deals in India, Mexico, the US and Europe over the past months.

It is currently considering an IPO and thinks it can get $3bn (10% more than GROW’s valuation of its 4.63% ownership).

#2 CoachHub 75.2p per share

Congratulations. Assuming you are happy with the valuation of this and Thought Machine you’ve just hit profit. Your £1.29 reaches £1.53.5 with the 2nd share in GROW’s portfolio.

4th place in GP Bullhound’s 2023 Tech Titans “most likely Unicorns in the next 2 years” (they had a 90% success rate from 2021 to 2023). It’s valued at $800m in its last funding round so a mere 25% higher valuation will get them there.

This is an interesting example where CoachHub was used by 43,000 strong Cemex.

#3 Aiven 65.p per share

Aiven is the leader in its space according to G2. Aiven is a set of tools for developers to code faster and more efficiently.

This graphic tells you all you need to know, I think.

#4 Ledger - NAV is 48.9p per share

While the Oak Bloke and over half his readers think Crypto is a scam, this picks and shovels play is a way to profit from the movement.

Ledger’s main products are cold hardware wallets (which look like Flash Drives) for storing digital assets, allowing the owner to have full custody and security over their assets. The company currently says it secures more than 20% of the world’s cryptocurrencies and more than 30% of NFTs.

Last month Ledger introduced integration with popular Crypto site Coinbase, so you can buy your crypto nonsense and transfer it to a hardware wallet - your assets are safe and secure…. what could possibly go wrong?

Congratulations reader! With these four companies alone if you think their NAV is sound you’ve just covered £2.60 per share of assets (over double the net £1.29) you paid.

Shall we continue?

Form3 48.5p NAV per share

I ask you reader - how does a Fintech have a client list like this?

Yesterday, Form3 announced its new APP Fraud Solution. It works by combining Form3’s account-to-account payment processing with Feedzai's fraud and financial crime analytics. This produces a model that is trained to identify risk in both the individual sending the money and the person receiving the money. Understanding who is receiving the money is key to preventing fraud, as APP fraud involves impersonation that manipulates the victim into sending the money.

APP fraud losses accounting for nearly £500m per annum, the solution is timely, as it has been developed on the back of new regulation from the Payment Systems Regulator. This sees victims of APP fraud being refunded by their bank from October 2024, with **reimbursement now being the responsibility of both the sending and the receiving institutions**.

That’s why.

NB Eagle-eyed readers will spot that Form3 appear in the GP Bullhound list of Unicorns too.

Conclusion

I would write and write about how each of GROW’s holdings appear to stand up to valuation scrutiny.

Scrutiny by Molten. Then by PWC. Then by Deloitte. But the market knows better…. apparently.

Or there’s some serious hidden value here.

This is not advice.

Oak

There can be no other description of the UK equity markets other than "disfunctional". From mining to venture capital it's the same story. The risk appetite of retail investors has been strangled. The long-term consequences for enterprise, innovation and economic growth are terrible. If it was just cyclical I would not be too concerned but I feel this time it may be systemic. Companies will look elsewhere for capital if this continues and London will become a backwater.

While I approve of this analysis and find it very interesting, I suggest that Mr. OakBloke adds a disclaimer that most of his tips are small cap or micro cap holdings that suffer from higher risk and higher volatility than companies that are traditionally defined as "blue chip".