INOV-ious value

Keeping a sharp eye out for targets

Dear reader

Tomorrow morning we find out the percentage of shares that we have been able to tender….. if any. The £37m return of capital as a tender offer at NAV less costs (21.11p) is 40% above the share price and 110% above the level in my 1st article “The Most Unloved”

How many did you tender reader? How many have you bought since?

My answer to those questions is 100% and plenty. Here’s why.

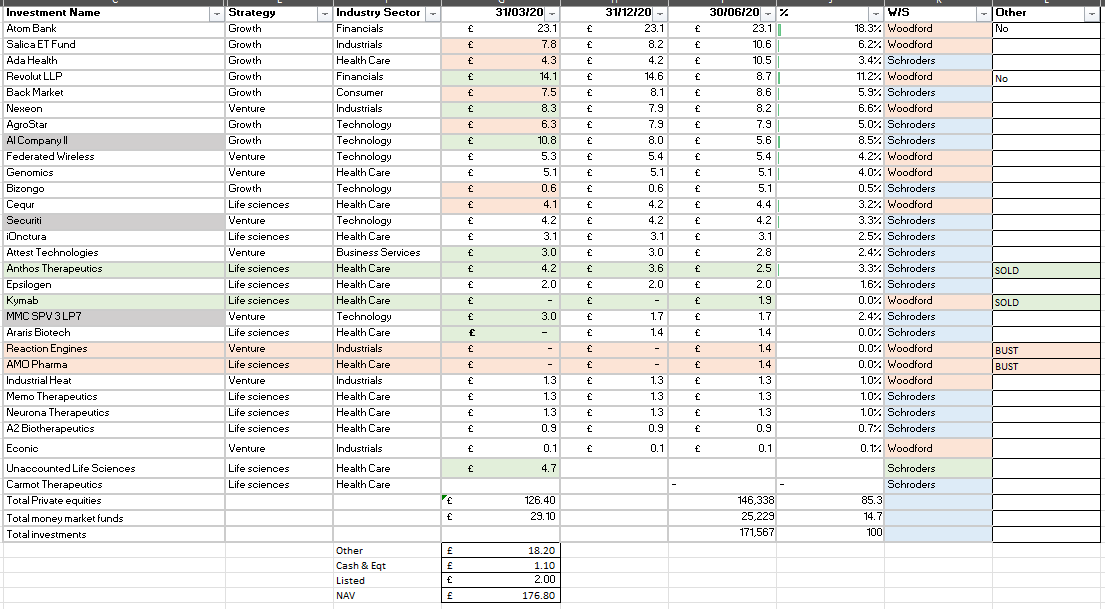

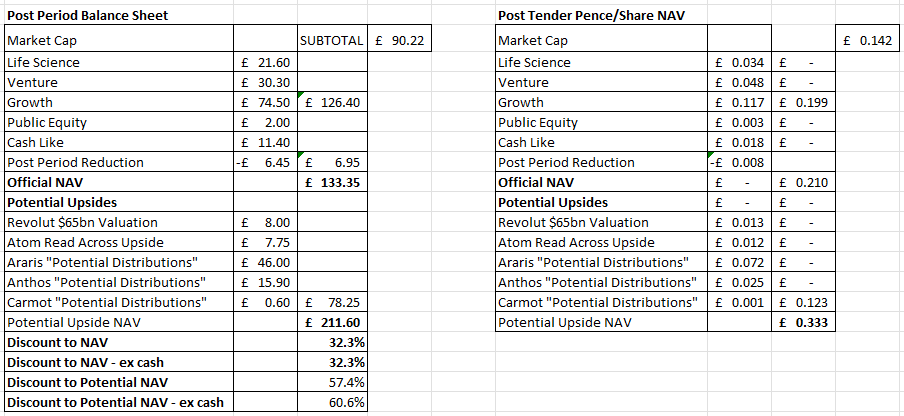

First of all let’s set the scene. This was the last official update - a NAV at 31/03/25 totalling £176.8m. The current NAV is 21.36p, and after costs 21.11p is being returned. I’m going to make the assumption that plenty of people (including all the harrumphers) have taken up the tender offer.

Meanwhile INOV has slipped back down in price to tempting levels, and at today’s 14.2p buy price that’s a £114.8m marcap.

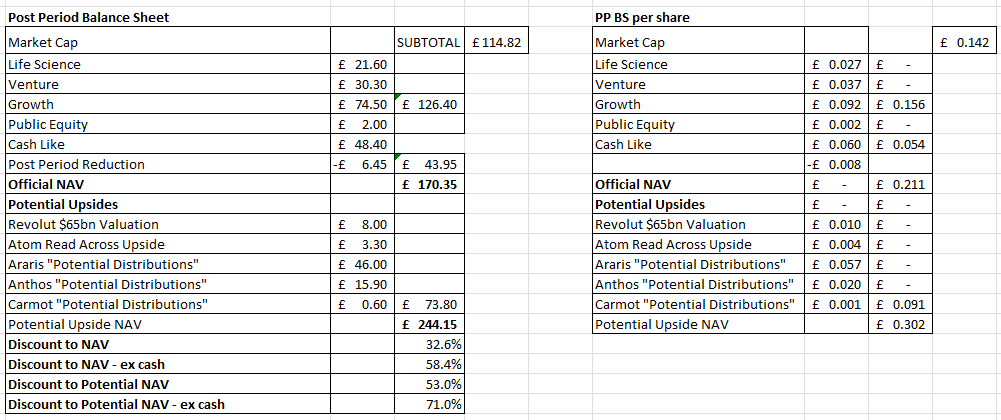

This was what I previously assessed the potential NAV to be.

The tender at 21.1p doesn’t take into account future potential upsides. Which potentially provides a 2.4p per share upside to 32.6p per share.

But I now believe the number is actually HIGHER

Why’s that?

#1 ATOM BANK

My £3.3m “potential upside” was based on its last funding round led by BBVA (in Nov 2023) and that was at a reduced £362m valuation round. INOV hold 7.28% of Atom Bank at a reduced valuation equivalent to £3.3m less.

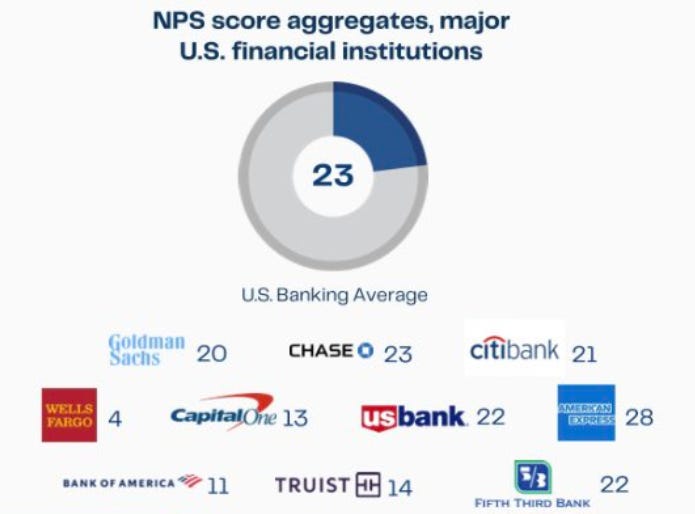

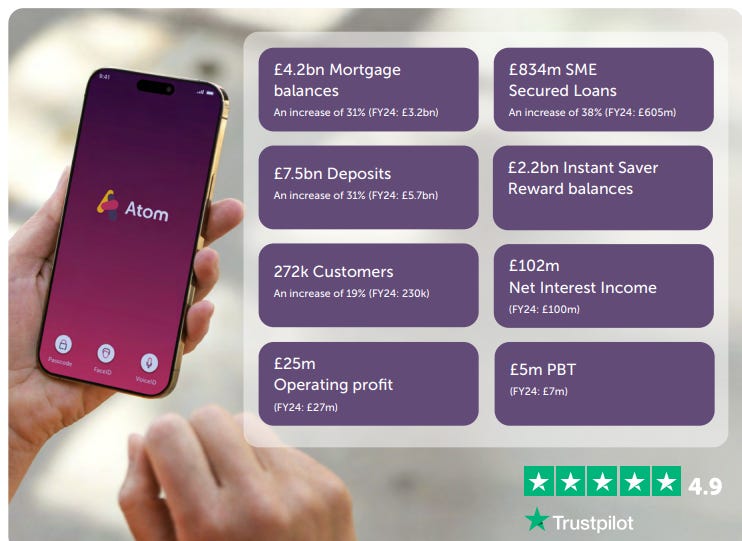

But what if £362m is almost certainly an outdated valuation? Atom announced their results ending March 2025 with net profits up 30% to £16.9m (from £12.3m)

Growth in customers, lending, deposits, Trustpilot Score (4.9) and Net Promoter increased from +88 to a TRULY ASTONISHING +89. Who gets such a score? Across 272,000 customers? Apple did - briefly - but only get about +70 today. Most UK banks get no more than +30. Some struggle to get double figures. Customer’s ain’t happy…..

Atom Bank delivered strong results in its FY25…..

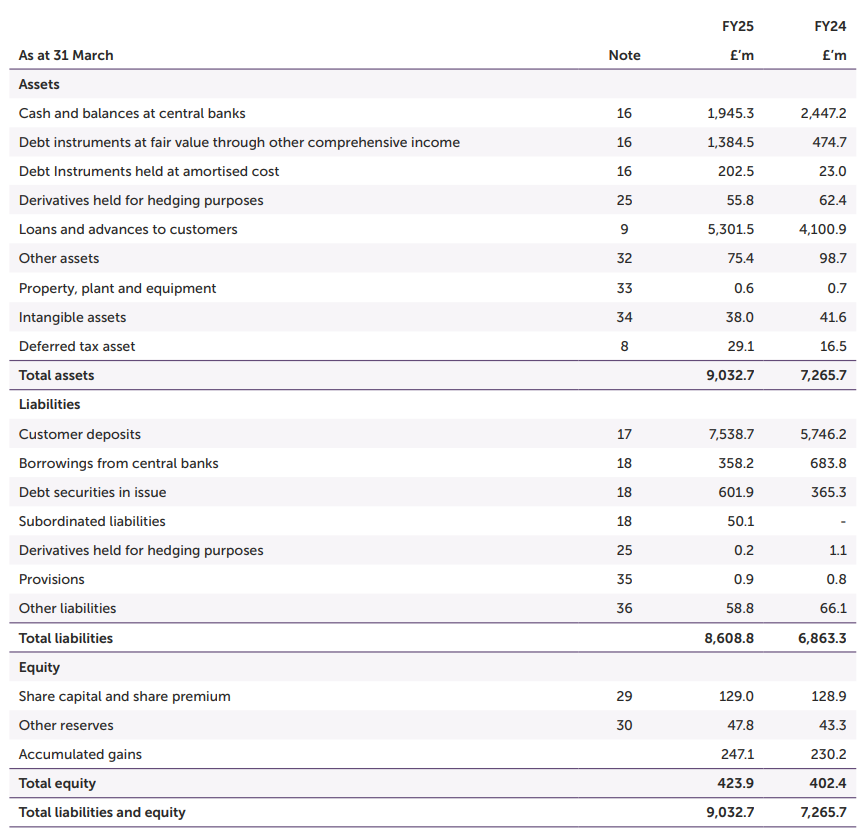

The current valuation doesn’t even cover the net tangible assets of £423.9m. And should the £38m intangible be valued at zero? What’s the value of a +89 NPS?

25X earnings is £422.5m which is another justification for a valuation of at least £423.9m.

Growth across the business was impressive, even though falling interest rates meant the net interest margin fell from 2.8% to 2.2%. So +30% volume and -30% rate meant operating profit didn’t grow year to year although this was mainly to do with the fixed rate savings products that have now rolled over into newer products at lower interest rates (reducing costs and improving margin).

Atom is all about scaling technology at a low marginal cost. People costs and overheads grew by about 12% despite the business growing over 30%.

Included in that 12% increase was technology investment to further introduce AI and further automate functions, but also compliance costs to progress its IRB permission. IRB or “Internal Ratings-Based” allows banks to hold less capital compared to the Standardised Approach, as internal models may assign lower risk weights to certain assets if the bank can prove lower risk profiles. This can improve profitability.

The regulator for this is the PRA, the Prudential Regulation Authority.

So ATOM I believe has a potential upside of £7.75m to arrive at a £30.85m valuation based on both current year earnings multiple at based on NAV.

#2 Revolut is worth $65bn not $45bn (or $42bn)

I previously said £1m potential upside based on a secondary valuation at $45bn. The newsflow has moved on since then.

Revolut is a global financial services company that specialises in mobile banking, card payments, money remittance and foreign exchange with over 52.5m retail users growing fast and a 2024 implied $45bn valuation will prospectively rise to $65bn in an upcoming funding round (if it proceeds).

Revolut achieved in 2024 revenue of over £3bn, and that’s a 72% increase year-on-year, driven by their customer adoption growth and product offering diversification. Their technology-driven operating model allowed a translation of that growth into profitability, reporting a net profit margin of 26%, as net profit grew to £790 million.

Revolut Business continued to grow in 2024, generating 15% of total revenue, as more businesses join to use its multi-currency accounts, global payment services and smarter spending tools.

A $65bn valuation makes INOV’s 0.046% holding worth £22.6m, versus the current £14.6m. So an £8m uplift, and not a £1m uplift based on a $45bn valuation

Conclusion

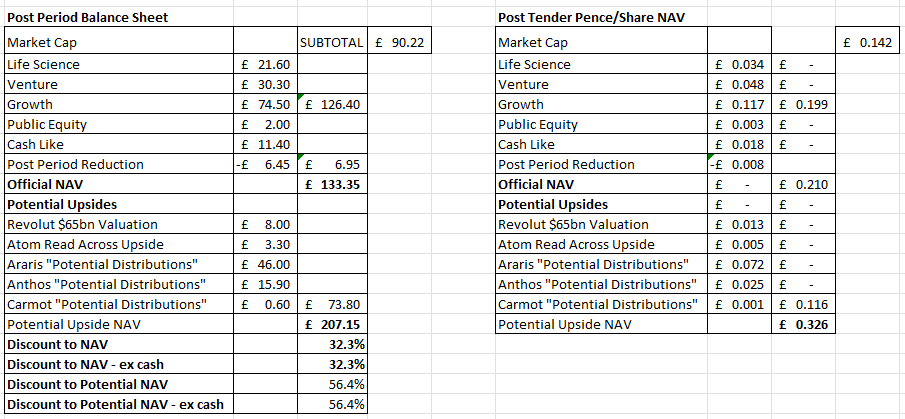

If these upsides are correct then INOV is worth 33.3p a share and there’s a 60.6% (ex cash) discount to the current 14.2p share price. Seems the current price could be quite tempting for its Atom Bank and Revolut holdings, alongside its fast-growing AI holdings as well as other ideas and follow on potential distributions from successful biopharma sales too.

Regards

The Oak Bloke

Disclaimers:

This is not advice, you make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

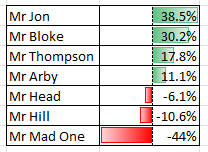

GROW flying up 22% in week. News on NAV increase was cause but good rises leading up to it.

Have you had a look at IP GROUP? Not an investment trust.

Roughly a 45% discount

£500 million market cap. £250 million of cash (roughly).

Aim to add another £250 million worth of sales before the end of 2027.

60 company portfolio.

Entitled to share on the sales of a diet drug which should be on sale around the end of 2029. Phizer is now the company that is going to produce it. Starting phase 3 this year.

Simply put very vintage assets.

FIPP is another one worth looking. BUT small £14 million market cap. 16 company portfolio. 23p NAV 69p (last update) NAV falling as they are not contributing to funding rounds. IE dilution but short to medium term the extra funding could easily increase the valuations. This portfolio also looks vintage. FIPP up 15% yesterday on no news. Big spread.

Oh and I forgot Augmentum on a 47% discount. Growth capital is in my opinion looking very cheap and ready for a rebound. With some already showing some very decent increases.

Very useful info above, but would have been good to know it before the tender deadline passed. So I gather you tendered 100% of your holding and then bought back the same amount at 14-15p on the market? Or maybe it's worth waiting to see your allocation before buying back?