JLP - the high grade material deal

Jubilee Metals reports a further copper deal

Dear reader,

I sat listening to a Leon Coetzer interview in the mid week takeaway, only to find it has been reheated for today’s Sunday Roast. What a disappointment! It was a deja vu (deja ecouté?) moment.

Having covered JLP recently in the article “large waste project” it’s worth understanding the implications of this extra news.

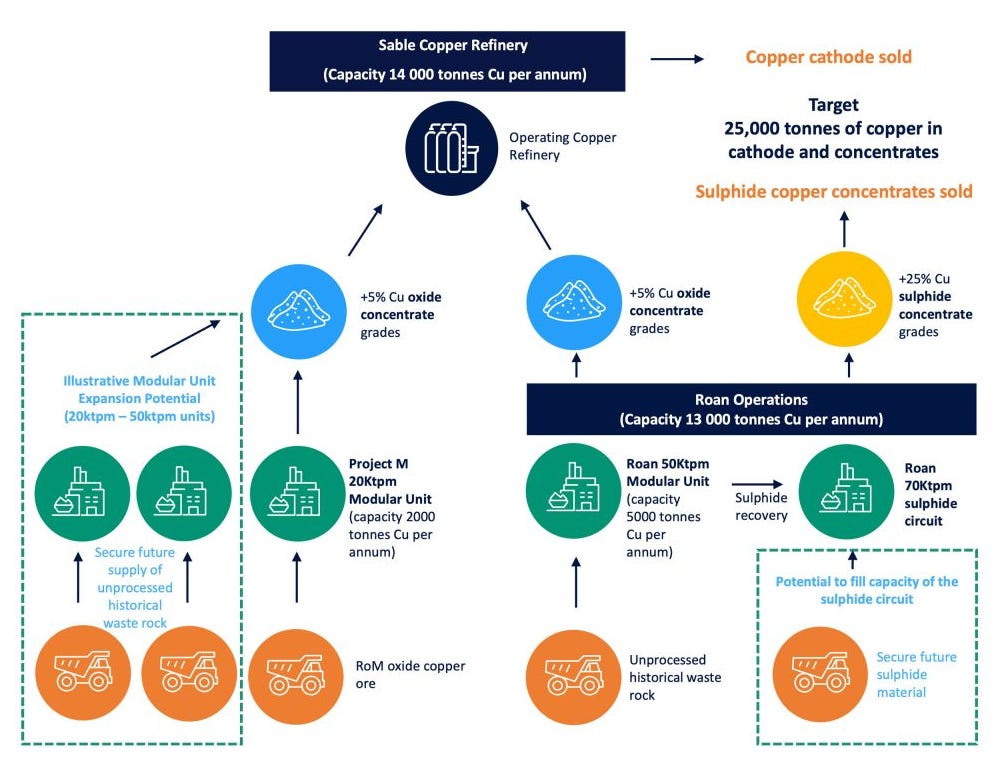

First of all confirmation that Roan has restarted so 40 days of 2025 have been lost, but the regulatory approvals are given, the distributed power is operational and a further deal has been struck:

So 200Kt of material with 1.6% copper, equates to 6.66 months at a rate of 30kt (out of 45kt capacity). Or 4.44 months if they do do a switcheroo and switch to 100% high grade (as would be likely). There is then a further 1.42mt of material for follow on purchase, if desired. (“over 3 years supply” equates to 0.045Mt x 36 months, less the 0.2Mt purchased)

The purchase price of $2.7m (settled in shares) equates to $13.50 per tonne of ore, or $843.75 per unit of copper produced.

At an approximate $4000 per unit/tonne of copper that’s a profitable trade, particularly when you consider the 1.6% vs 0.7% copper content is a 0.9% difference/uplift which on 45Kt per month is 405 tonnes extra. 405 x $4000 is $1.62m gross profit, less the -$843.75 per unit (so -$0.34m) nets to a $1.28m gain per month. So from 10th February to 30th June equates to $1.28m x 183 days less 40 days = $6m extra profit in 2H25 (to 30th June 2025), even after dilution.

An annualised run rate to profit would be an additional $15.36m operating profit per annum.

Of course this $6m extra in 2H25 is based on Oak Bloke assumption of $4,000 margin per unit which is conservative and based on historic margins (of $2,670) adjusted for scale and higher copper prices in FY25.

Notably in today’s recycled interview Mr Roast discusses a profit margin of $18m in his interview with Leon for the 200Kt of ore. On 200Kt that would mean a much higher $5,625 per unit margin (200,000 x 1.6% = 3,200 tonnes of copper, and $18m/3200 = $5,625 per unit. Leon appears to agree with Mr Roast on the accuracy of this calculation.

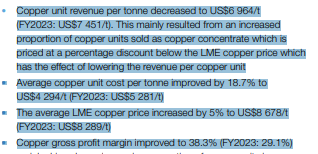

How have profit margins for copper concentrate improved at JLP? We are told in the FY24 report that it is priced at a discount to the LME copper price which is why average revenues were only $6,964 per tonne, despite Copper being $8,678 for the period.

Is $18m an inaccurate calculation? This would require an average copper price of around $12,250 per tonne to achieve that, based on a ~18.5% discount for concentrate, assuming average unit costs remain at $4,294/t as it was in FY24.

Or could the cost of producing Sulphides be much, much lower than producing Cathodes? Seems a pretty important point for investors to understand. Perhaps someone like the Jubilee guru Seisnav will know the answer.

I do agree, however, that 45Kt at 1.6% equates to 720 copper units per month and 8,640 per year. Leon again endorses this number, and points out that Roan alone could exceed JLP’s copper guidance (of 5,850 - 7,500 tonnes).

1,454 was achieved from Sable so assuming the same again in 2H25 gets you to 3,900 tonnes (assuming zero benefit from Project G coming on board in the period, potentially large waste rock too, Project Munkoyo ramping up)

4.7 months at 720 units gets a further 3,375 tonnes.

So 7,275 copper tonnes would be near the top end of guidance. If JLP can keep Roan going at 45,000 tonnes and Sable continues its refit but repeats the 1H25 performance.

Conclusion

The news of a higher feed was positive, but it really just builds on the recent “Large Waste” article. Following a recent 4.7p share price and its revisit to 3.9p JLP offers an intriguing opportunity, given its positioning in Zambia, for Copper, on top of Chrome and PGMs in SA.

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"