KZG year end thoughts

937.16m shares in issue, market cap £5.15m, NAV as at 30/06 £10.9m, discount to NAV 52.7%

Dear reader,

A week on from my conspiracy theory musings about a shadowy Kazera Sosei, we now have AMS as a 26.69% shareholder, a name emerges Prem Premraj - the CEO of AMS. A bit of googling later, that name only appears to appear in relation to the KZG news. What does that mean?

Meanwhile the accounts have been finalised ahead of the 6 month deadline but slow at 5.5 months to produce. Must do better please KZG. However speculation that they would fail to produce accounts in time proved to be unfounded.

Conspiracy:

As I spoke about last week, a takeover could still happen. Interesting that Align still appears to hold 3.3%. What does that mean? Will Align continue in 2024 and retirement is delayed? Input from two “Dragons” for Den(nis) is no bad thing.

Value:

AMS spent £3.75m to own 250m shares. That’s the equivalent of paying £14m for KZG net assets of £10.9m. Why? Well for a start the HMS and Diamond Licences/Mines/operations are in the books at just £0.75m. The 2.5% Royalty has zero value in the books. So AMS have paid pro rata £2.4m premium to net assets (£0.64m to be precise as they own 26.69%). So what’s their possible calculation?

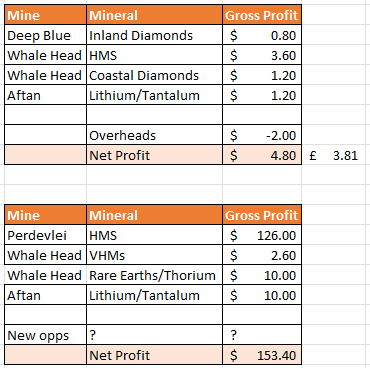

The estimated run rate income suggests the assets are hugely undervalued. KZG bought the mines at bargain prices. Assets that could generate £3.8m PBT at a very conservative Price Earnings of 7 are worth £26.6m. So almost double what AMS paid.

The top section are my estimates for the royalties and two mining operations for 2025 (i.e. run rate after ramp up). I’ve split out the diamonds from the HMS. My calculations and valuation thoughts were covered in this article so I won’t repeat them again.

The upsides in the 2nd section, I also covered previously, were the 35x larger beach. I’m applying a 35x to the $3.6m to arrive at $126m GP i.e. I’m assuming no economies of scale. I also spoke to the fact that the HMS contains Valuable Heavy Minerals (at about 2% concentration). VHMs fetch a far higher price. There’s a capital cost to introduce separation. Equally monazite can contains REEs and Thorium or Uranium. For the HMS to be radioactive SOMETHING is making the Monazite radioactive. The company has confirmed that both of these avenues are areas to explore in the future but that it only makes sense to do this once operations are underway.

I also speak to a $10m upside from Aftan. What is this? Well, if KZG do exercise their right to take back Aftan (after all Hebei Xinjian are in technical default) they can put the Lithium/Tantalum mine into operation and on their doorstep is a processing plant. The JORC resource is an estimated $277m (with upside potential according to Align).

KZG also speak of bigger and better things than Aftan including in this interview below. Dennis explains either the debt will be sold, or the mine sold to another party, or Hebei pay up. This will resolve in Q1 2024. Remember the Arcadian operation begins in Q1 2024.

The Diamond Pulsating Jig starts up and processes the stored diamond rich gravels built up over 6 months at a rate of 20 tonnes/hour.

The HMS is ready to go once the radiological permit is satisfied. Dennis explains offtakers are happy to provide magnetic separation. The coastal diamonds can also be processed by Deep Blue.

Risk

There is a going concern statement in the accounts in relation to being paid by Hebei and commencing HMS operations. It’s my understanding if neither of these two things occur by CY2024 H2, then the business would need further funding.

Then if it couldn’t sell the Hebei debt (even say with a haircut of a few million) which seems unlikely to me, or they couldn’t secure a line of credit, or complete a fund raise (even again with a discount) in July 2024 it runs out of money.

That’s the going concern.

Then shareholders are reliant on what 64% of a de-risked and ready to go HMS operation is worth, what 60% of a live inland diamond operation is worth and what a debt of £9.5m which can still be collected by an acquirer is worth. Oh and what a 2.5% royalty on a JORC of $277m with potential resource upside is worth.

Another HMS miner Base Resources (BSE) is sitting on $92m cash and their current Kenyan operation is in wind down while its Madagascar operation is several years away. So that’s just one example of a suitor who would be interested in picking over KZG’s bones if it all goes Pete Tong. Kenmare (KMR) with $110m cash is another HMS operator.

Can KZG shareholders lose? It’s my personal bet that the value and development stage of the assets mean there appears to be no downside….. and imminent upside.

Going concern “red flags” give some people the willies - but I believe you need to consider the circumstances the assets and lack of liabilities.

Conclusion

While some will point to the going concern as a reason not to buy KZG and long term holders feel their suffering will never end (to paraphrase bulletin boards), the full year accounts FY2023 are positive and offer no surprises.

In fact it’s quite hard to believe that a business reporting a 0.7p/share gain for the year remains at a 0.6p ask. That’s a price earnings of 0.85. Bonkers.

This is not advice. My advice is if you need investment advice go and get it.

Have a good weekend and may I wish all my readers a very Merry Christmas.

Oak