Lemme ATM! Lemme ATM!

The 1Q25 result - is a price drop a big opp?

Dear reader

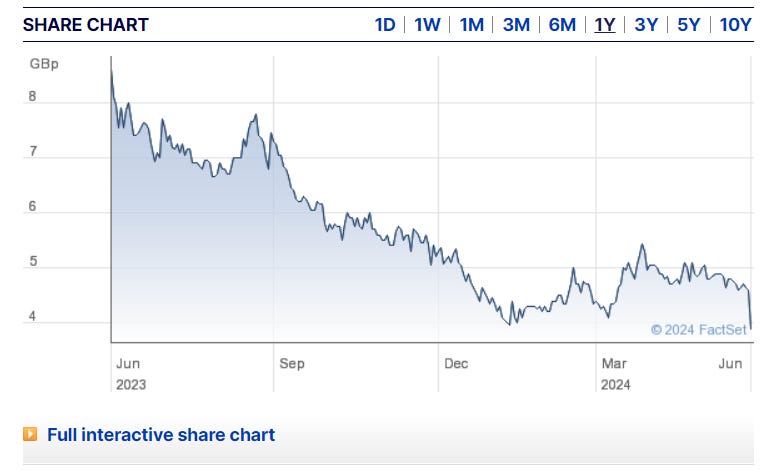

Andrada (ticker ATM) has descended to 3.8p bid / 4p ask a few times over the past year. And has halved over 12 months. Ouch. Down 15% last Friday. Double ouch.

Why?

Well Lithium pricing is a factor as I set out in my article Tins-are-still-improving. But a 15% drop was on the Q1 results and probably this sentence:

The answer is due to a one-off issue. Now of course you could say that’s a lack of foresight by management etc but this is mining and excrement happens in mining.

Let’s consider the underlying performance and progress. First of all the TPH (tonnes per hour) is extremely consistent, over an extended period of time. Second is that the ore processed is up 10% year on year, thanks to utilisation also up 10% and availability up 2%. I have maintained for some time the quality of the production management at ATM is excellent. The bit which dropped was the recovery due to that one-off factor.

But consider what the contained tin would have been without that factor. Let’s use the Q4 recovery of 72%:

0.141% x 238kt x 72% recovery = 241 tonnes. So 18 tonnes more, and a 5% improvement quarter to quarter. The AISC would have been $26.6k not $28.7k ($28.7k x 223 / 241)

Consider too that the AISC includes stripping costs of overburden. These are strangely not capitalised to WIP and then recognised once the stripped ground is mined, instead expensed immediately. The stripping ratio is the ratio of waste material to useable ore, and the life of mine ratio is quoted as 3.5.

In Q2 the stripping drops from 2.4:1 down to 1.5:1 so that reduces that cost by around a third. But what is that cost? To work out the cost saving we must factor in the royalty of 5.1% to Orion. That cost was $307k in Q4 and $350k in Q1.

A little bit of mathematics leads me to estimate that 1.5:1 stripping reduces the AISC by ~$2,000/tonne. ($900,000/240)

Later, in my model from 3Q25 the 3.5:1 ratio takes the cost back by ~$4,000/tonne.

So combined with the one off factor the underlying AISC going forwards drops to $28.7k in Q1 to -$2.1k and -$2k = $24.6k per tonne, then back to $28.6k per tonne (£20,268) from 4Q25 (October 2024). So the average in 2H25 is $26,600 AISC (or £20,945). This is before any expansion but including new costs like the Orion royalty.

Expansion & the price of tin

But expansion IS underway. The funds and agreements with the banks and with Orion are now in place (they weren’t 12 months ago when ATM was twice the price of what it is today). Back when tin prices were at least 20% lower than they are today. When the forecast for tin was bleak after falling rapidly - and it isn’t today. Trading Economics reckon tin has 10% upside from here. $36k in 12 months time vs $32.6k today.

Either investors holding ATM 12 months ago were totally insane or today ATM is incredibly cheap.

Expansion is happening. It is being built as I write. Viljoen also points out the reduced stripping ratio I’ve explored above…. no wonder he believes “ideally positioned”. Costs down revenue up. Ching! Ching! The ATM starts to fill.

The investment into volumes of tin should increase to 1,600 tonnes so a 75% increase from today.

The expansion will reduce AISC by ANOTHER 10% - so potentially to $22k/tonne (which is £17k)

The commissioning is due CY 1Q25 - which is (confusingly) 1Q26 (i.e. February-April 2025)

Here is my revised forecast of the P&L in GBP.

This is based on a 2H expansion from March 2025, I’ve assumed a 6 month ramp up to the full 2,600 tonnes annualised of tin concentrate (and a 1,534 contained not 1,600 per the name plate). I’ve further assumed the lithium pilot circuit begins March 2025 and the full expansion March 2026. I’ve assumed the additional beneficiation costs of $20,000 a tonne from 1H27 (remember there’s no additional mining costs but beneficiation costs). $18,000 a tonne is conservative but this will also factor in capex and depreciation of said capex. Or $18,000 cost per tonne represents the revenue share to a Lithium partner. (NB More than $18k and there is no increase in profit - it is not worth doing).

This assumes a partnership regarding the Lithium expansion occurs and an agreement is put in place fairly soon. There is a strategic process ongoing managed by Barclays. I also assume current low prices for Lithium revert by March 2026 (as forecasted). The “Production And Strategic Process Update RNS 12/03/24” sets out that a full-scale integrated processing plant would be a 30,000 tpa of technical grade petalite.

Revenue in this model increases from £22.57m in 2H26 to £38.26 a 70% increase of revenue. Just over midway in the 50% to 80% increase and based on higher future lithium prices.

Eagle-eyed readers will also see the mystery of the tantalum is solved. ATM aren’t selling it at low prices but were communicating about volumes of concentrate and not actual tonnes of Ta. Using the 10% concentrate data in the Q1 update I model an eventual 8.2 tonnes of Ta per annum - again conservative.

Conclusion

A 3.8p ask for ATM equates to a £59.3m purchase of ATM. Given the underlying progress it is bizarre for it to drop 15% in my opinion. People simply do not understand the dynamics and fixated on AISC costs in Q1 are up.

If I’m right in my analysis, these results lead to a FY26 P/E of 12, falling to a FY27 P/E of 9 using some fairly conservative assumptions which could surprise to the upside.

Final Thought

PS re-read the RNS. Varied Investors plural. Assets plural. I’ve considered the expansion of a single asset - lithium - via a single investor. Could we see multiple lithium deals not just one? Could we see the Tungsten at Brandberg West developed too? None of that is even in my model - but my eye is drawn to the pluralisation.

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Sorry to be coming to an old post, but these calculations were very useful. However last week's financial results suggest ATM is making significantly heavier losses than you were projecting thus far, unless I've missed something? £8.9M (non-comprehensive) losses for FY2024, vs your projected £4.76M. Have I missed something? And if not, would the more recent results cause you to update these projections?

Hi,

Sorry to prolong this discussion but the figures seem too good to be true. I think the problem is that if you take account of the lithium and tantalum revenue is calculating the AISC the entry in revenue in the spreadsheet should only be the tin revenue.

Also, I don’t think the company have said they will produce 30000 tonnes of Lithium per half year.

Thanks, G