Microsalt - IPO Part Deux - and 2 Mysteries

Part of TEK - one of the Oak Bloke Top 20

Happy news that Microsalt floats this Thursday. SALT will be the first IPO of 2024 and let’s hope not the last. I do not intend to repeat the prior analysis regarding the market opportunity of Microsalt in my articles What Happens Next and Introducing Microsalt.

Instead I’d like to explore 2 mysteries:

Mystery 1 - the case of the disappearing shareholding

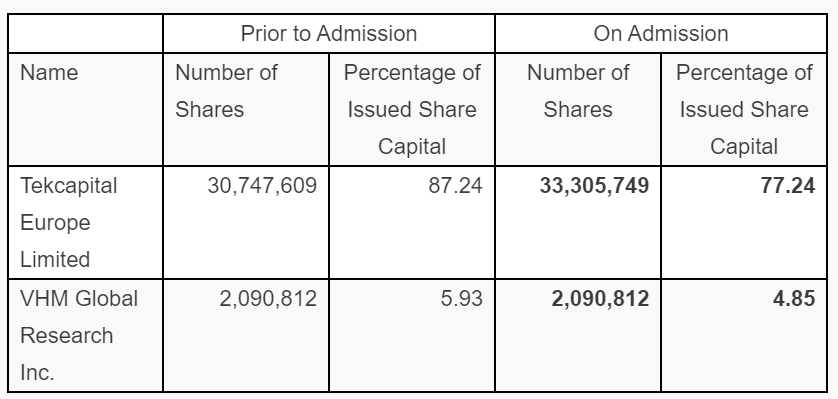

In the half year report it was reported that TEK Europe owned 97.2% of Microsalt Ltd.

Yet today the “prior to admission” states 87.24%, not 97.2%.

What happened to the missing 9.96%?

The answer is found at companies house where 7m shares were issued. Why? To increase the holding by Microsalt Ltd of Microsalt Inc. It now owns 92% of Inc (not 79% as before).

Meanwhile VHM Global which is owned by Microsalt’s ex-CEO Manzanilla now owns 5.93% of topco (and 4.85% post IPO). I expect the answer to the mystery is Manzanilla had contractual terms that entitled him to this.

Are the IPO terms fair?

Yes. £18.5 admission price is £1.5m below the premoney estimate I reported on before but nevertheless values TEK’s holding of 77.24% at £14,289,400. In its last accounts its investment in Microsalt was valued at $17,095,379 which is £13,460,928. So a £828,471 gain for TEK. Plus £3.5m of liquidity some of which will repay LUCY but leaves just under £3m. Plus TEK maintains a strong majority holding in a listed entity.

Not a huge gain, but a gain, and remember reader in my article 120 musings I said based on the current BELL and LUCY, TEK’s holding in SALT would have to fall below $12.8m which is £10,078,740.

This is 29.5% below SALT’s IPO price of 43p/share which would require a greater than 12.7p drop. So SALT remaining above 30.3p is the magic number on Thursday folks.

That’s where 100% of TEK is backed by cash and listed holdings. (and you get Guident and ReVive and the IP reports businesses for free)

Mystery Number 2 - shaking the SALT P&L (and BS)

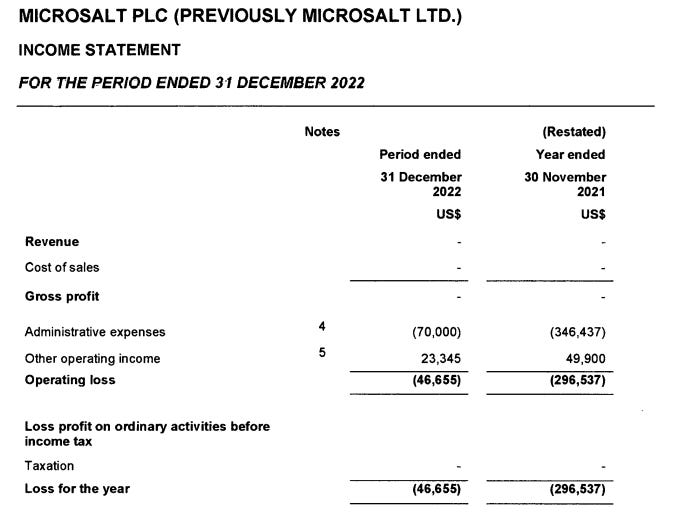

I read today in a Microsalt “Everything you need to know” article in the UK Investor Magazine at this link that Microsalt lost $2.5m in FY22 and achieved $300,000 revenue in H1 2023. I was intrigued. Had they? Nowhere had TEK or SALT ever provided any sales figures, nor had any P&L info about Microsalt ever been shared. Where had that author got their info? After careful review of all RNS I was still none the wiser.

I did, however, find very interesting news reviewing their accounts.

In 2022 Microsalt Ltd booked no revenue at all.

Its loss was not $2.5m in 2022 but instead a much smaller $46,665 loss.

Digging further I found the “$2.5m” - the loss is not a loss - it’s a loan from TEK to Microsalt. So Microsalt made a much smaller loss than has been reported.

But how did TEK value Microsalt in its 2022 accounts? TEK booked a $9,742,595 fair value gain on its holding in Microsalt in 2022 (and it’s nice to see that fair value value only 100% backed up with today’s float valuation)

YAWN?

Bear with me reader we are coming to the good bit.

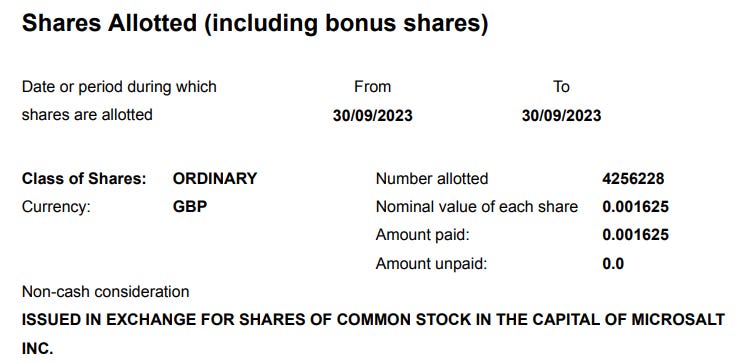

I spotted that Microsalt Ltd have given us a 9 month picture of their accounts as at 30/09/2023. They had to produce this due to the Mystery#1 share swap.

Why is this important?

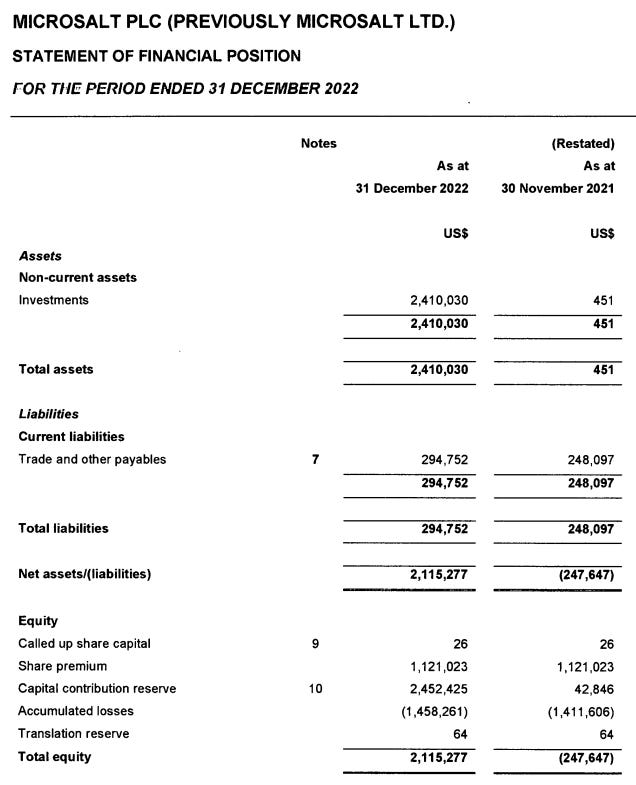

In these accounts we see debtors of £0.78m and we see a tidying up of share capital as they converted from Ltd to Plc (i.e. rolled up the accumulated losses and share premium). The difference in total equity in 9 months is the P&L outcome.

A £338,647 profit.

£0.3m is a modest profit but it shows that SALT is profitable, already.

That’s before continued growth from its various outlets, its B2B activities as well as all of the new post period activity below.

£0.78m debtors asssuming a conservative 60 day DSO (average debtor days outstanding) suggests an approximate £5m 2023 turnover to SALT (0.78*12/2). If that’s true £0m to £5m year one is impressive!

Not being funny when you are listed in nearly a thousand stores and have sold 20 tonnes to a B2B customer common sense tells you that your sales must be around this…. if not more!

Post Period (1st October 2023 onwards)

The above balance sheet is as at 1st October 2023 so what’s happened since?

1.Microsalt selling via Amazon UK (RNS 9/1/24)

2.MicroSalt continues to make on-boarding progress with several large UK food companies for inclusion of Microsalt® as an ingredient in their products. We will provide future updates in due course. (RNS 9/1/24)

3.MicroSalt recently received wholesale orders from two Fortune-500 companies, one a leading snack food company and the other one of the world's largest pharmacy/food retail chains. (RNS 22/12/23)

4.Additionally, the company is engaged in late-stage supplier discussions with other major snack food brands which the company hopes to announce in 2024. (RNS 22/12/23)

5.Secured placement of its SaltMe! low sodium crisps with distributor MR Williams Inc servicing convenience stores across North Carolina, South Carolina, and surrounding states up to Delaware and down to Georgia. (RNS 01/10/23)

6.Longs Drugs, a leading 70-store drug store chain in Hawaii owned by CVS Health, agreed to place MicroSalt's SaltMe! Crisps in their stores across the state. (19/10/23)

Penultimate Thought

Should I sell TEK and buy SALT?

If you’d sold TEK and bought LUCY, if you’d sold TEK and bought BELL would things have gone well for you? What I am trying to illustrate is that putting all your eggs in a single basket increases risk. It’s fair to say it also increases upside.

Will SALT be different? There are key differences for SALT. First of all LUCY is a B2C fashion/lifestyle choice (albeit with B2B coming via its safety glasses). BELL required medical approvals and further product development. Both have since gained substantial customers but that took time.

SALT begins apparently profitable, with a debtors ledger suggesting sales of some millions with large customers and a unique proposition.

It’s a hard call which is the right way to go. Both, I believe, will be extremely attractive. From a tangible assets perspective I have to come down on the side of sticking with TEK if you can only pick one, or going for a 70/30 split TEK/SALT if you want a stronger upside from SALT.

Conclusion

If you thought you knew everything about Microsalt you now additionally know:

It will IPO as a profitable, going concern.

It DID NOT make a $2.5m loss in FY22.

Its post period activity suggests profitability will grow.

The pre IPO reduced shareholding is not really a dilution because a correspondingly higher percentage of Microsalt Inc was gained.

TEK’s publicly listed holdings are probably going to 100%+ back the share price by the end of this week.

Microsalt’s progress and success is one of the reasons why TEK is one of my Oak Bloke Top 20 for 2024.

-

These views are my personal opinion, not advice. Written to set out the facts for my own current and future investment decisions in TEK and Microsalt. I hope you enjoy reading my posts and good fortune in your own investment decisions.

Oak

Hats off to you OB! I couldn't work out the TEK ownership disparity!

Take a look at what happened to the investors at MicroVentures. The company took our money and ran to the LONDON Stock Exchange.

Maybe you're missing some shares in that aspect as well.