Part 1 of 3 - Considering RBTX and Rockstars

A deep dive into an ETF called RBTX - or should it be No-botix?

Dear reader,

I was keen to explore investing in Robotics. In a fund? An Investment Trust? No, I thought I’d try an ETF. I think it might be the first ETF article written by the Oak Bloke. Hmm no the 2nd. I covered the highest-yielding ETF called SDIP in my article “SDIP-ping into paradise?” (Hint: Paradise Lost)

RBTX meanwhile is managed by Blackrock’s iShares, so a highly reputable fund manager. They’d be all over the Robotics theme, right?

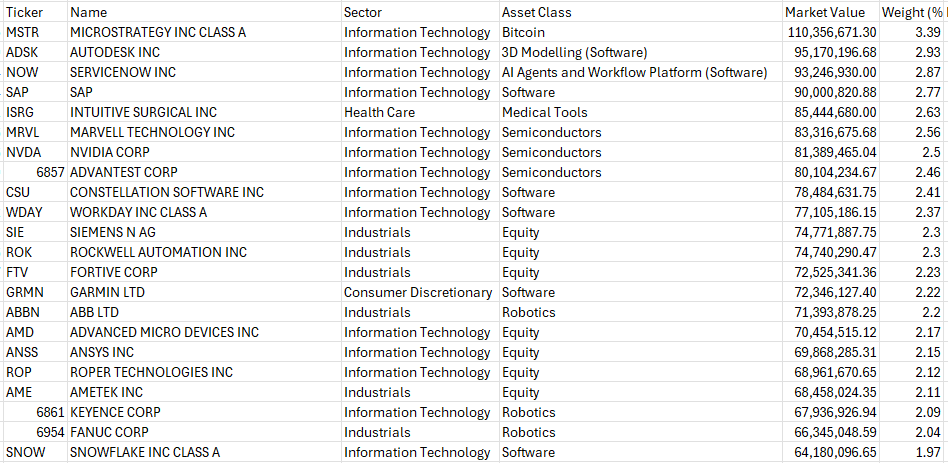

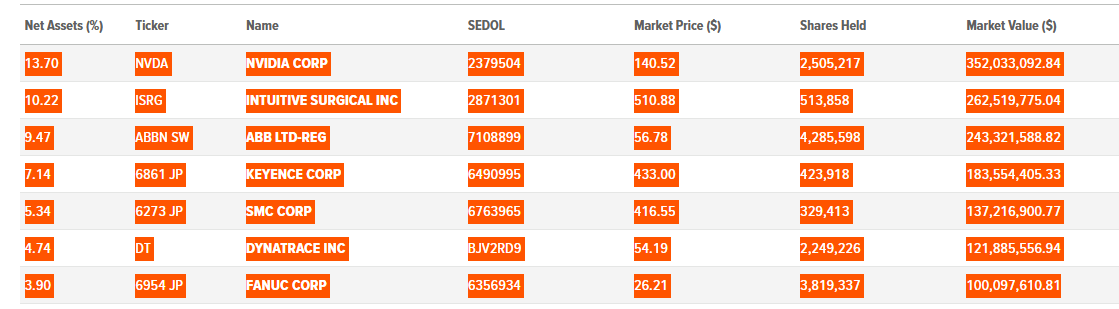

RBTX Top 10 Holdings:

1. Microstrategy # 3.39%

AI Suite Software for Business Intelligence featuring Bot building, natural language queries to create data visualisations and integration with MS Teams, as well as platforms like Snowflake and Databricks.

But I recognise the CEO Michael Saylor. Isn’t he the billionaire who nearly went bankrupt due to Bitcoin crashing in price? Ah yes, here he is in Fortune Magazine.

As at 30/06/24 Microstrategy hold 226,331 Bitcoins and they are on the books at just $5.7bn. Hmmm. That’s just $25.1k per bit coin. Hmmm. So at today’s market price those bitcoins at $72,236 are worth $16.35bn. $10.65bn of “hidden” value.

Except they are as well hidden as a Hezbollah leadership bunker. Microstrategy has 200m shares trading at $258 each and this puts its market cap at $51.6bn vs a book of $2.8bn (and $4.2bn of debt). So including the so-called $10.6bn of hidden leaves a further $38.2bn of premium to market cap.

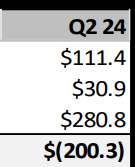

The AI/BI software itself looks quite good but its quarterly sales of $111m barely covers its own costs, and there’s barely any growth. A -$200m quarterly loss includes $180m of Bitcoin “Digital asset impairment losses” so a -$20m loss, really. This is due to a weird accounting rule where any downward losses must be expensed to the P&L but not any of the “hidden” gains. So you could be kind and say its software business is “near break even”.

But the stated strategy is to keep buying as many bitcoin as possible, and the reason we are told they are doing this is because Bitcoin is not even 1% of the world’s assets. Yet. And they’ve not crashed back to 0% (again) either.

I’m left with an uneasy feeling that this stock defies gravity - but am impressed how you can’t dispute they’ve achieved a 1200% stock price gain in 4 years. If I owned it I’d be very tempted to sell as quickly as possible to lock in that gain. It looks incredibly overpriced with very little to justify why it is on such a multiple.

In any case the top holding has nothing to do with Robotics. Not a great start.

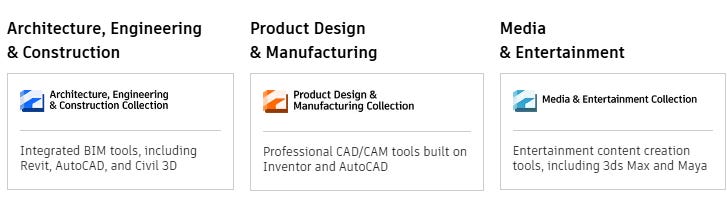

2. AutoDesk

A P/E of “only” 32, a PEG of 1.9 and who knew that Autodesk don’t just make AutoCAD but also tools for manufacturing, product design and media?

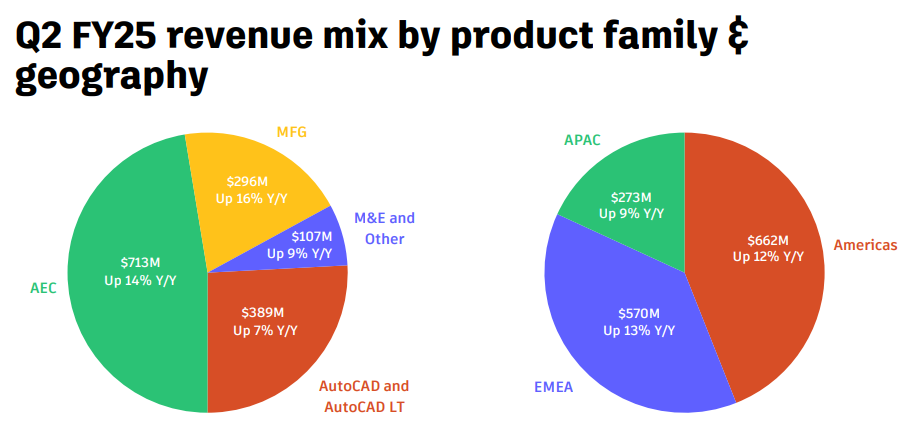

Autocad (in the AEC space) and Autocad LT make up 3/4 of revenue but Manaufacturing is actually the fastest growing space.

Looks a strong company but fully valued at its current price with no upside on analysts’ consensus. Yet again it has nothing to do with robotics.

3. ServiceNow 2.87%

Another guy I’ve seen on Bloomberg is the CEO of ServiceNow. David Rubenstein asks him why did you leave SAP to work for a smaller company. He tells David it’s because he saw the future. Rubenstein says tell me in plain English what you do, and reading about ServiceNow the waffle he tells Rubenstein about being the backbone of IT is quite different to what ServiceNow actually does!

I found ServiceNow is a low-code platform to build Workflows i.e. business processes for internal departments, but workflows connecting your business and your customers and suppliers. Think graphical dashboards and design tools to build processes with connected lines and drag and drop. ServiceNow have just launched an AI agent that works within those workflows. 85% of the Fortune500 use ServiceNow is a good boast to have too.

With an eye-watering 58.3 P/E ratio, and 2.4 PEG (i.e. 25% earnings growth), you do pay for this quality share. I actually really like it, the product looks good and I can see how could drive service automation and why 85% of the Fortune500 do use it.

But there’s no robotics at ServiceNow.

4. SAP 2.77%

Business Enterprise Software.

I’ll keep this short - no robotics.

5. Intuitive Surgical 2.63%

Doctors use many technologies that enhance their capabilities beyond what the human body allows. MRI and CT scanners, for example, enable doctors to “see” inside the body. Similarly, many surgeons perform robotic-assisted surgery using a da Vinci system because it extends the capabilities of their eyes and hands.

So Surgical Tools that make surgeons more productive, and drive better outcomes for patients going under the knives. But not exactly robotics. at least not today. At least we seem to be getting warmer.

At a p/e of 66.4 and with a growth of 17% this isn’t an undiscovered stock and you are paying a price for quality.

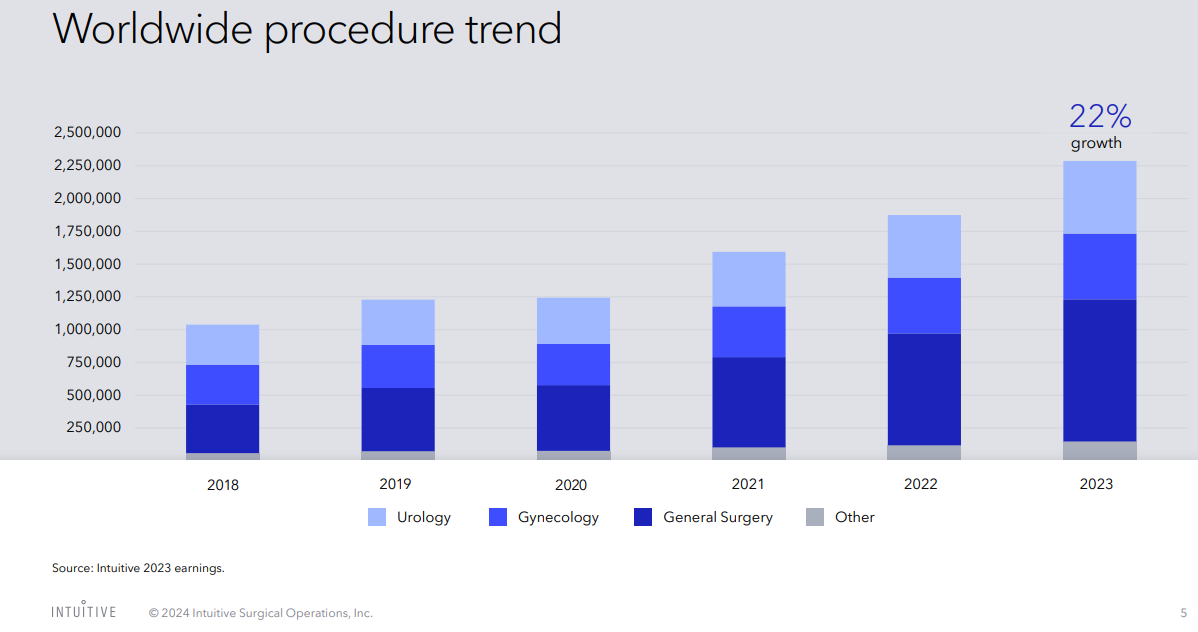

The number of procdures is growing, and hospitals with at least one intuitive robot which have gone on to buy more robots are strongly growing the number of robots i.e. it appears clear they are proving their worth.

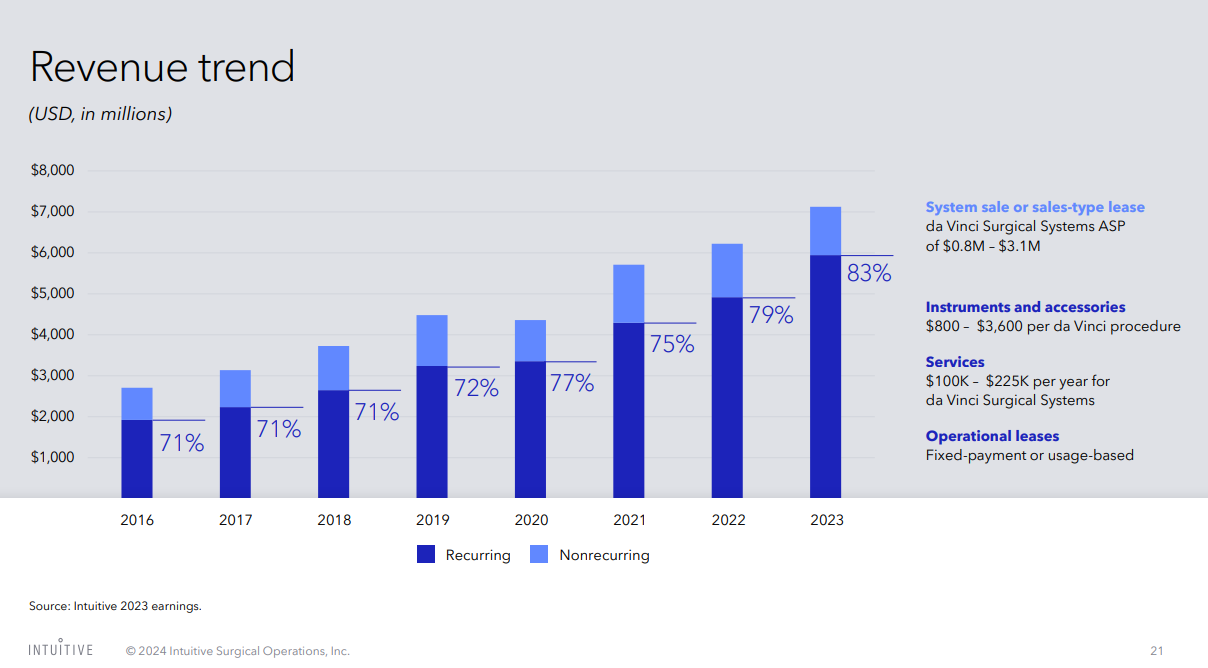

What is noticeable is the degree of recurring revenue from instruments, accessories and services. A 69.1% gross margin for physical hardware (and software) is an impressive number.

I’d rather like to consider Intuitive more but this 2.63% holding isn’t tempting enough to make me like RBTX on its own. So where are the Robotics in RBTX?

6. Marvell 2.56%

Semiconductors - not robotics.

7. Nvidia 2.5%

Semiconductors - not robotics. Fully appreciate Robots do contain Semi Conductor chips (I watched Arnie being lowered into the Molten Furnace in T2 because of one he had in his head), but hey, there are Semi Conductor ETFs and I am looking for Robotics. Give me robots please.

NB I will be looking at NVidia in more detail in Part 2.

8. Advantest 2.46%

Semiconductors - not robotics. A Japanese company and the P/E is “only” 40.

9. Constellation Software 2.41%

Software for various verticals especially “mission critical”. Imagine you bought an airport? You’d then need to buy an Airport Information System. So the next time you’re at an airport you’ll remember the Oak Bloke told you about Constellation as you stare at the departure boards.

But no robotics.

10. Workday 2.37%

ERP software for Rockstars (if you believe the adverts).

Possibly some robotic and hammy acting in those adverts on Bloomberg - but no robotics. To riff with the Rockstars in the adverts: “Just because you are called RBTX does not make you a Robotics star.”

Conclusion

RBTX is not for me (in case you’d not realised this). If you’d bought it at the depths of the Covid sell off you’d have doubled your money until today but its performance hasn’t been great - 23% over 1 year but only 3.9% over 3 years. Given the meteoric rise of some of its top 10 holdings over 3 years there must be some stinkers losing money lower down. If you want to own an ETF which invests in software companies valued at 50-60X earnings plus semiconductors valued at around the same RBTX is worth a look.

The top #10 comprise 27% of the RBTX and robotics is a tenuous name. Some interesting companies but at fairly hefty prices. Who looks at the composition of an ETF to make sure they are buying the “theme” it says on the tin? You just assume don’t you?

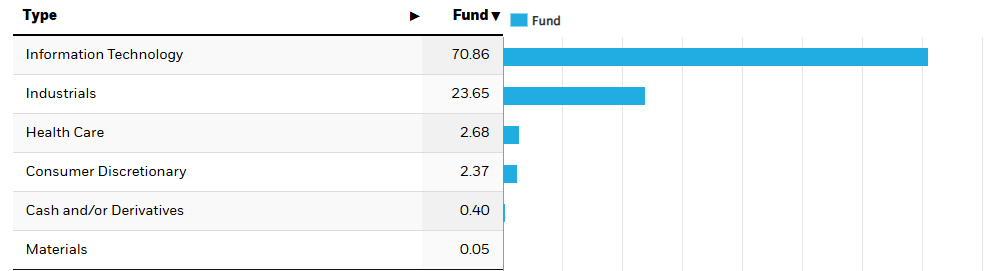

The iShares web site tells us 70.8% IT and 23.6% industrials so perhaps that isn’t a surprise.

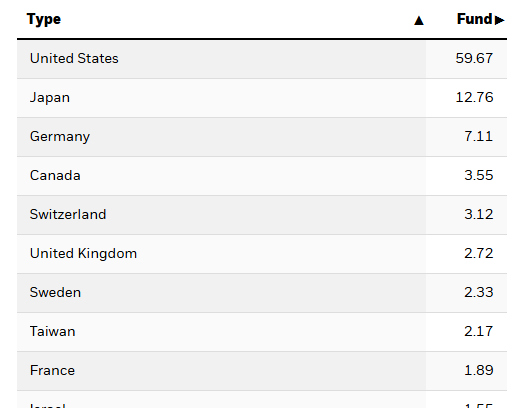

It shows 2/3rds North America, 15% for Japan/Taiwan and Europe.

If I cast the net wider and taking the top #22 (the top 50% of holdings at RBTX) there’s less than 7% of actual Robotics, although I do like ABB, Keyence and Fanuc. I’ll be discussing each of those in a future article.

No, actually let me give you an amuse bouche. Why Robotics? Why Japan? Robotics because I believe AI is fully valued and on peoples radar. Because is true value not taking an AI brain and giving it hands and feet (or wheels)? Robotics is the perfect complementary technology to AI and its day will come, soon. In fact self driving AI only makes sense with a car. Chat GPT can annoy and frustrate you with text responses but can’t make you a cup of tea. Tesla’s Optimus can (allegedly). Robotics also has military applications. Robotics drives efficiency. Robotics is also the antidote to the Demographics time bomb in parts of the world, or indeed for the world, including Japan. Encouraging more babies perpetuates the strain on the planet’s resources.

For example if I look at Fanuc at position #21 in RBTX it is a Japanese Robotics company then we find a £20bn market cap, generating £0.7bn net income and growing with a P/E of 28.5. Quite reasonable.

Why Japan? - Because it’s cheap. But also because of the great passion and expertise. I believe we will find some interesting companies there. But also because of the Big Mac Index.

The Yen is nearly back at 200 Yen to a £1 and I’m chewing over the reality that the Big Mac Index makes buying Japanese a very profitable prospect. Consider, reader, that a Big Mac Meal is 650 yen or £3.25 in Japan, and I don’t believe 200 Yen can continue. At 150 Yen to the pound, a Big Mac Meal would cost £4.33 which is still a lot less than the UK (or USA).

A recent presentation from Ruffer spoke to how they believed the Yen would weaken (and they held some sort of Bond as part of a hedge strategy).

A 150 Yen FX rate to the pound would also mean Fanuc would then be worth £26.6bn not £20bn and its earnings rise from £0.7bn to £0.93bn - in GBP terms.

So how do I find a Fund, Trust or ETF with lots of Japanese Robotics? With 30% of its portfolio, Japan, for example? Well it’s not RBTX that’s for sure.

Where can I find over 50% is Capital Goods and Equipment and about 25% software and semiconductors?

Where the top #10 at RBTX Intuitive Surgical is 2/3rds of the 15.2% healthcare, and Fanuc Robotics is a decent 3.9% of the portfolio.

All will be revealed in Part 3 reader.

But in Part 2 I’m going to consider Ark Invest Robotics and AI

Regards

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings including those held in an ETF might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

Good strategy to analyse the underlying holdings rather than just believing the name on the tin. I've got a small holding in L&G Artificial Intelligence (AIAI or AIAG) which is used for long term exposure to AI trends, and then I try to trade larger amounts in the AI leaders when they have pullbacks like Nvidia, Lam Research, TSMC, AMD etc