Pocket some HGT

A rule of 40 is for wimps. Bring on a rule of 50.

Dear reader

Before I speak of HG Trust move over Mr Kennedy and here’s an incredible rendition of Vivaldi. It can only put a smile on your face this weekend. We need it. A shorter bank holiday week never feels shorter, does it?

On with HGT.

You would have paid £3.55 per share earlier yesterday.

457,728,500 shares in issue means a £1.62bn marcap and net assets at 31/3/26 of £2.4bn.

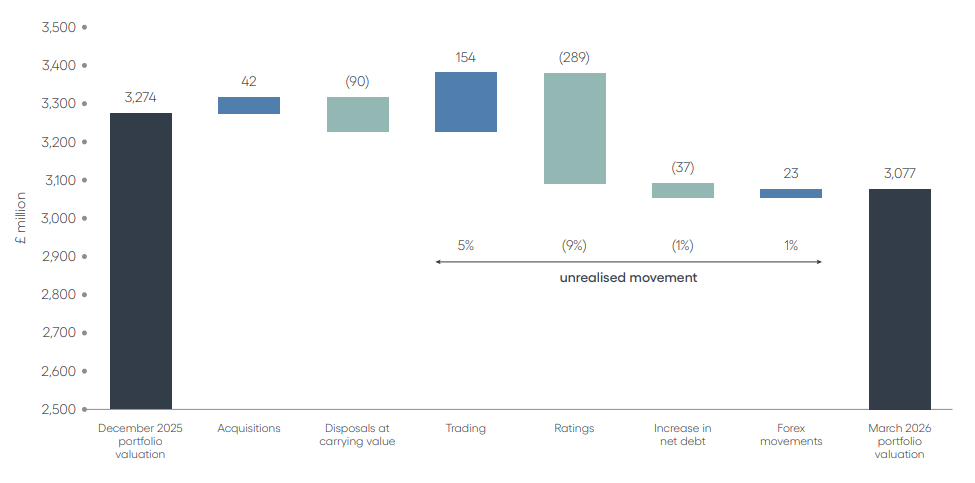

£3.55 is a £1.73 per share discount on £5.28 per share of assets, so a 33% discount. Where £5.28 per share is based on a £3,077m net portfolio less £677m debt.

Where in 1Q26 there was -£289m of adverse valuation i.e. 63.8p per share was “wiped off” the valuation due to “multiple compression”. More on that in a bit.

Where that same portfolio generated 34p per share of earnings.

So an investment of £3.55 generates 34p in 3 months, and 26.5p is attributable to equity. That’s £1.04 of earnings per year. That’s nearly 30p of trading EBITDA in the £1 of HGT shares:

HOW?

Each £1 of HGT NAV is earning about 20p of trading earnings before interest tax depreciation and amortisation per year.

That’s calculated based on £154m x 4 (£616m) on a portfolio of £3077m, where 2400/3077 or £480m is attributable back to the NAV of HGT.

But since you are paying £1.62bn to earn £0.48bn EBITDA that’s 29.62%

NEARLY 30p in the pound!

Wait, what?

Weren’t we told AI was going to replace software? That software is doomed? If so then why is it instead generating record levels of trading profit? Why are profits far higher than prior years? Could it be that the detractors have it wrong? Deeply wrong. Wouldn’t be the first time would it?

Trading profit is at record levels - but is it just a one off? Even if you take the lowest results over the past six years - during lockdown - you still get a trust earning an EV/EBITDA of 16X. Ignore that as a one off (we were all tending to our gardens and clapping for the NHS heroes Thursday at 6pm, out clapping our neighbours clanging a saucepan perhaps) and the average is an EV/EBITDA of less than 8X.

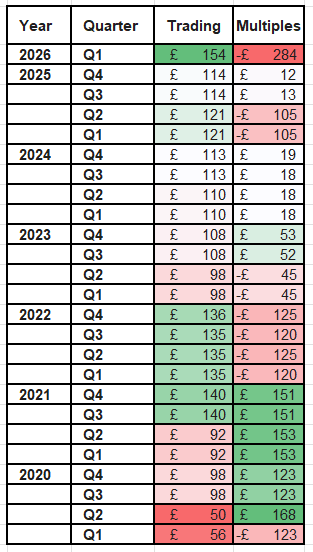

Based on 1Q26 it’s just over 5X. (£154m x 4)/£3077 = ~5.1X

What’s a fair price for HGT? Consider that 5.1X is a third of its peers.

Microsoft 19.5X, ActiveOps 46X, Sage 14.6X, Intuit 14.6X, ADP 14.3X

That’s just focusing on the “Trading” result since 2020.

MULTIPLES

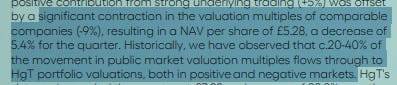

The second column is the gain and loss each quarter through multiple compression (and expansion). Valuations are made vs public markets (mark to market) and the likes of Xero, Sage, Oracle, etc. (Probably). The -£284m in 1Q26 was a contraction of valuations from 25.2X to 24X.

That’s despite an observation that the correlation is quite weak and only 20%-40% of the public market movement flows to HgT valuations. HGT use mark to market even if it’s a poor predictor.

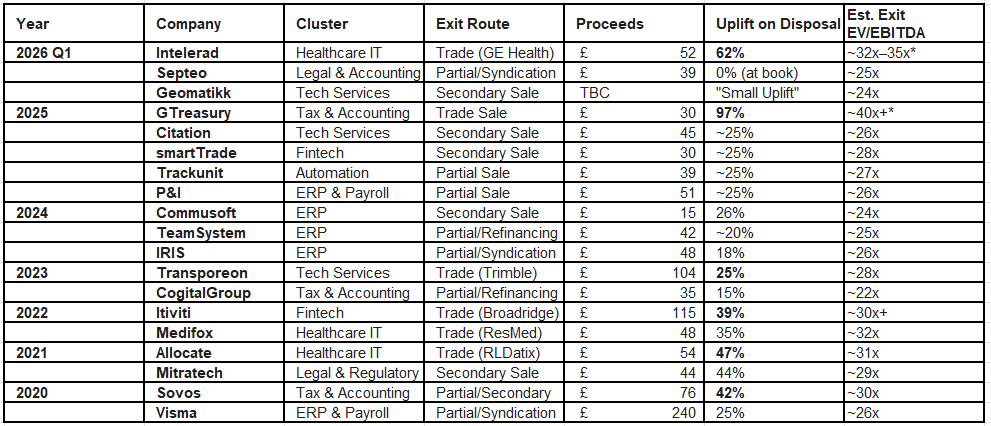

So when did HGT sell holdings at 24X? Once in 1Q26, once in 2024, and they dropped their pants with a low ball 22X exit with CogitalGroup. That’s 3 out of 19 times the portfolio’s current multiple valuation of 24X or less was the ACTUAL exit price valuation.

I was curious about Cogital. Evidence of AI erosion of profits? But no. The 22X CogitalGroup was a massive “buy-and-build” project and it was a partial sale at an attractive valuation to bring in a partner who could handle the complexity where the incoming partner gets a tickle - gets room for multiple growth and the payday for them and for HGT (partial sale remember) comes once the integration is completed.

So 16 out of 19 times the EV/EBITDA was higher than 24X, and quite a bit higher. Arguably based on real world sales the portfolio is undervalued by about £800m compared with the average exit multiple.

£2.4bn NAV should be £3.2bn. So £3.55 per share “should” be £4.80 based on exits.

Rule of 50

Based on the Q1 2026 results released on May 7, 2026, HgCapital Trust (HgT) is comfortably clearing the “Rule of 40” hurdle across its portfolio.

What is the Rule of 40?

The standard SaaS formula is Revenue Growth % + Profit Margin %.

The combination of both “should” be over 40. HGT scored 50 in 1Q26:

LTM Revenue Growth: 16%

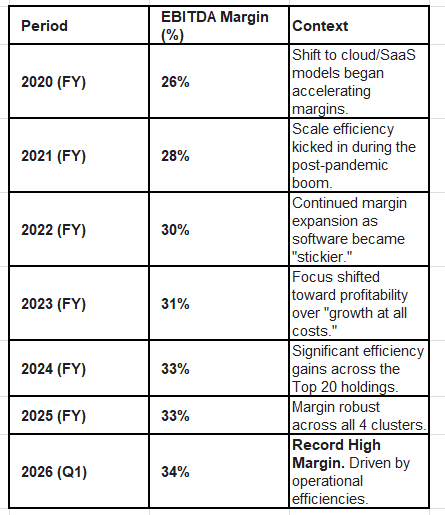

EBITDA Margin: 34%

Total Score: 50

Comparison Scores: Microsoft 62, Intuit 48, ActiveOps 33, Sage 32, ADP 32

Context

An aggregate score of 50 is considered elite for a portfolio of this scale (£2.4bn Net Assets). It indicates that the underlying businesses (which include 49 vertical software and service companies) are not sacrificing profits for growth.

Key Performance Drivers

The “Trading” Cushion: While valuation multiples in the broader software market (tracked by the IGV Index) contracted sharply, HgT’s underlying portfolio trading remained robust. Trading performance added +5% to the NAV, which acted as a partial shock absorber against the -9% hit from the nonsense multiple contraction.

EBITDA Outpacing Revenue: EBITDA growth of 19% is slightly ahead of revenue growth (16%), suggesting that the portfolio companies are successfully finding operational efficiencies (improving margins) even in “challenging conditions.”

Resilience vs. AI Fears: Chairman Jim Strang explicitly addressed the “AI disruption” fears that have caused public software stocks to sell off. He argued that Hg’s focus on vertical software (proprietary datasets with 100% accuracy requirements, like tax or legal software) makes them beneficiaries of AI rather than victims of replacement.

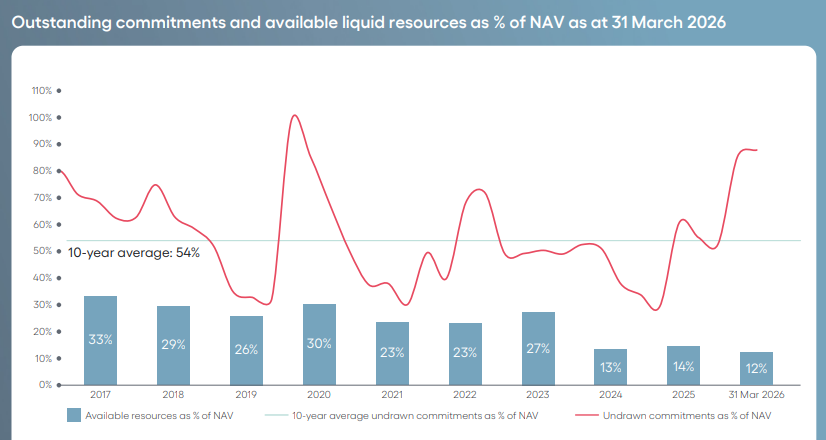

Commitments

Commitments to follow on funding 2026 to 2031 represent 88% of HGT’s NAV and is portrayed by detractors as some sort of negative. But HGT’s parent (fund manager) Hg invests around 10X more in a year than just the funds of HGT. It taps into clients money and there is no obligation to fund follow ons (although obviously that affects the % of ownership, and potentially miss the opportunity etc)

These are the outstanding commitments as at 31/3/26

The Paradox

Despite a Rule of 50 performance from the underlying companies, the trust’s share price was down 22.9% year-to-date at the end of Q1.

This creates an interesting setup: the operating engine is running at an elite SaaS level, but the market price is being dragged down by sentiment and the broader sell-off in listed software peers. The board has responded to this “indiscriminate” sell-off by initiating a share buyback programme, with £19 million repurchased as of today.

The share price is at 5 year lows despite delivering strong results since 2020 - and 2026 being stronger.

To arrive at 19% EBITDA growth overall in 1Q26 I considered the chart which breaks the portfolio into percentages that are growing at different speeds. I used zero for the 6% of the portfolio growing less than 5%, 7.5 for the 13% growing 5% to 10%, 15 for the 42% growing 10% to 20% and to get to 19% overall growth I had to use 30.1% growth for those growing >20%.

So nearly two fifths of the portfolio (by value) must be growing their profits by 30% on average per year to be hitting an overall 19% EBITDA growth.

We also know based on the sales growth that that EBITDA growth is through more sales not cost cutting or taking short term gain for long term pain.

Of course if the detractors have this wrong and if HGT are using AI (as they tell us they are) then you’d expect EBITDA margins to decrease, wouldn’t you? AI nibbles away at profits and vibe coders decimate sales and margins.

But that’s not true.

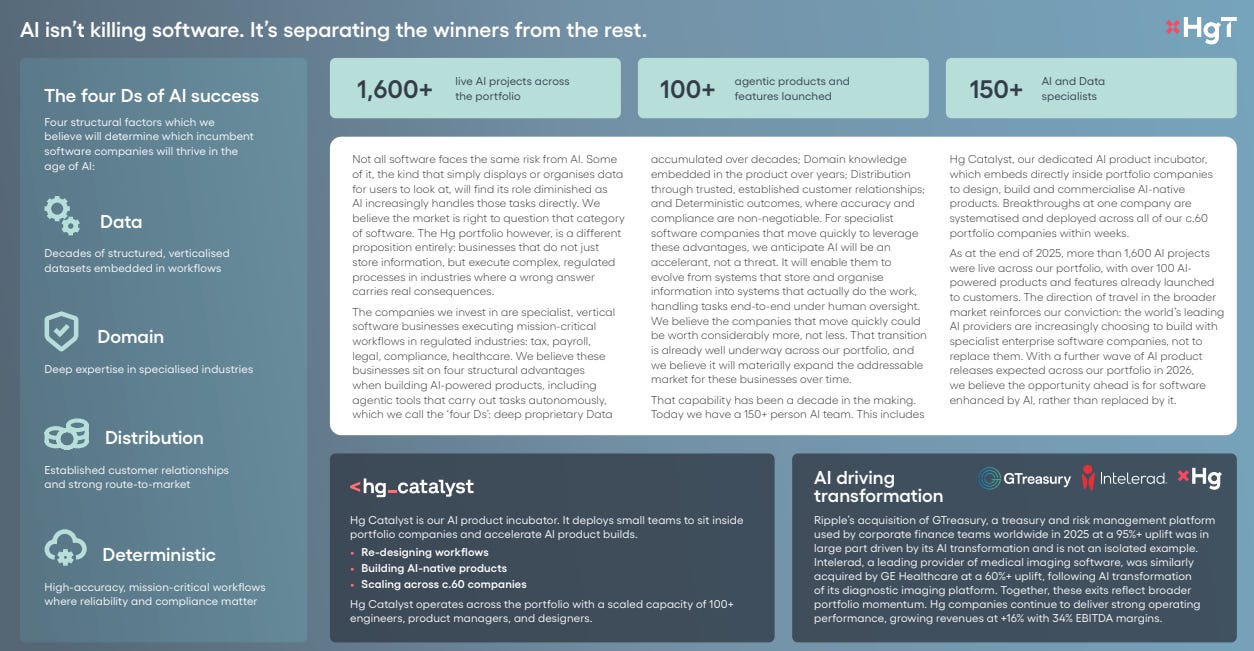

“AI isn’t killing software; it’s separating the winners from the rest” declare HGT.

Key Reasons:

Decades of structured, verticalised datasets embedded in workflows.

Deep domain expertise.

Trust. Established brands and relationships give a route to market.

High-accuracy, mission-critical, where reliability matters. No hallucinations please, we’re British.

Interesting to note a 95%+ uplift and a 60%+ uplift for its latest disposals following AI transformation. AI increased value. AI isn’t killing software but HGT are demonstrably making a killing - on both occasions - by adding AI.

Conclusion

I covered HGT previously in “HGT out to dry” and all of the same arguments in that article still apply today.

AI is simply capital vs labour and AI even agentic AI is unlikely to replace databases and systems. They work alongside. They add value. They are adding value. Twice.

Meanwhile, NAV reductions based on a 24X valuation multiple is a nonsense that hides value in plain sight. The rule of 50 up from 44 is extremely exciting. The growing 34% EBITDA margin is part of that 50.

Comparing HGT to listed peers, no one else is valued at 5.1X EV/EBITDA. No one.

Considering that AI is meant to make us smarter, the sheer lack of intelligence in this valuation is more than a little ironic.

Regards

The Oak Bloke.

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

OB - very interesting podcast on PCT trust. Few words on software and very interesting on AI in general.

https://youtu.be/8_XbnRrV4xw?si=LpmdH_rXuYAA0H87

the following comment in the article is not correct: ‘Each £1 of HGT shares is earning nearly 30p per year’. The HGT portfolio valuation is £3.2bn which at a 24x EBITDA valuation implies an EBITDA of around £130 million per year. The market cap of HGT is £1.7bn, therefore this implies an EBITDA yield of around 8% and an earnings yield of likely between 4 and 6% per annum (and not 30%).