PRTC-e for the big day

When the “Sum” is Greater than the “Parts

Dear reader,

Pretty much the entire Biotech sector has increased by around 30%–50% since 01/01/25, with US peers like BridgeBio (+140%) and Roivant (+35%) leading the charge. Yet PureTech Health (PRTC) has lagged behind, down roughly 12% over the same period.

Why?

PRTC isn’t just a drug pipeline; it’s a “hub” that owns a massive, undervalued portfolio of “spokes.” A year later, the market is still treating PRTC like a failing science experiment, even as the “spokes” keep hitting home runs. Let’s look at the math that investors seemingly refuses to do.

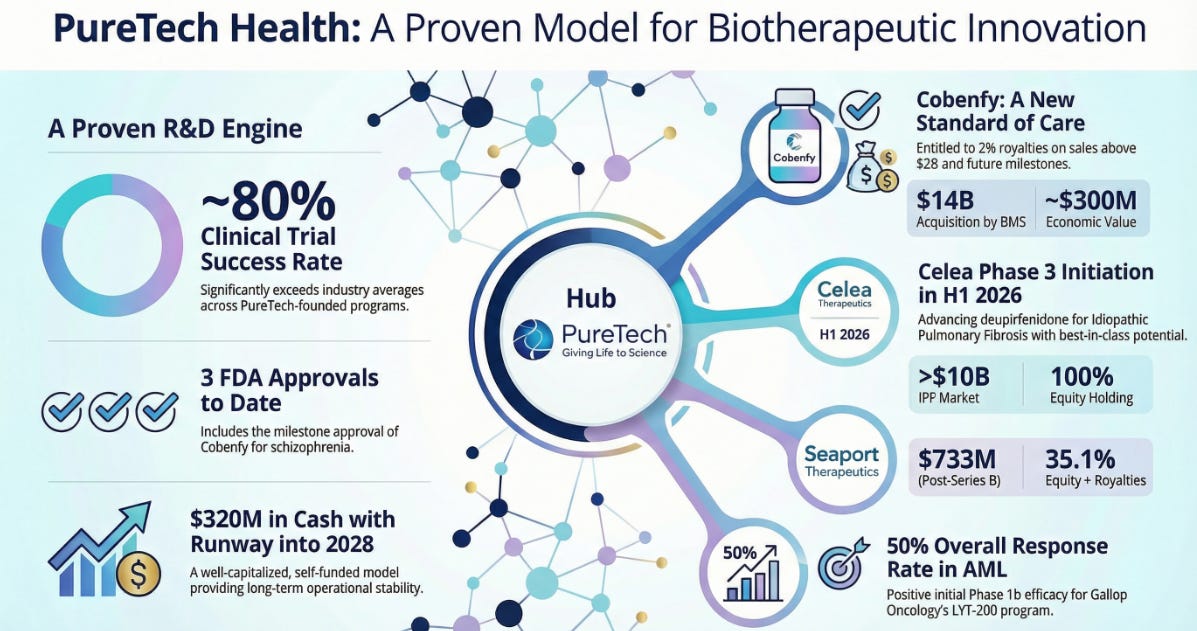

Who are PRTC?

In my prior article, PRTC-E doesn’t always make perfect, I argued that the market cap of PureTech was essentially “negative” if you accounted for the cash on hand and the value of its listed holdings.

The PRTC ratio showed that for every £1 of equity value you “paid,” you were getting exposure to billions in potential peak royalties and milestones. You were effectively getting the core R&D—the “Hub”—for free.

2026 and the “Orphan” Opportunity

Fast forward to February 2026, and the disconnect has reached “table-thumping” levels.

Deupirfenidone (LYT-100): The FDA and EU have just granted Orphan Drug Designation (ODD) for its treatment of Idiopathic Pulmonary Fibrosis (IPF). A Phase 3 trial is slated for 1H 2026. This carries significant strategic and financial implications:

Market Exclusivity: Upon approval, PRTC gets 7 years of exclusivity in the USA AND 10 years in the EU. This builds a massive “moat” around the drug.

Validation: Simultaneous US/EU designation confirms that regulators see the ELEVATE trial data as robust. LYT-100 slowed lung function decline to “healthy aging” levels without the gastrointestinal side effects that plague current treatments.

Financial Catalyst: PureTech’s founded entity, Celea Therapeutics, is currently securing outside capital for the Phase 3 SURPASS-IPF trial. ODD provides tax credits and waives multi-million dollar FDA fees, making Celea a magnet for venture capital.

The “Spokes”: The Hidden Billions

The market cap ignores the “Founded Entities” that are quietly maturing into giants. If you want to know where the value is, look at the spokes:

Seaport Therapeutics: Launched with $325M in funding (Series A & B). PureTech holds an approx. 35% stake. Seaport is using the Glyph™ platform to revolutionise neuropsychiatric drugs (like SPT-300 for depression), bypassing the liver to reduce toxicity.

Vedanta Biosciences: Targeting the gut microbiome. Their lead candidate (VE303) is in late-stage trials for C. diff. PureTech retains a significant equity stake and royalty rights.

The Karuna “Gift that Keeps Giving”: While Karuna was bought by BMS for $14B, PureTech didn’t just walk away with cash. They retained milestone payments and a 2% royalty on annual sales of Cobenfy™ (KarXT) above $2B. With analysts projecting peak sales of $5B+, that’s a pure-profit “annuity” for PRTC shareholders.

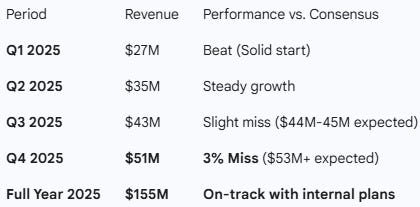

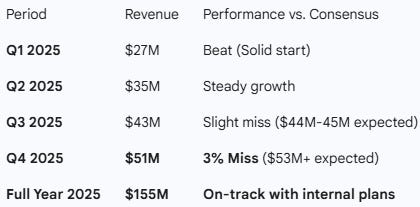

Cobenfy (the schizophrenia drug acquired from Karuna) is experiencing a steady but “sluggish” commercial ramp-up. While the drug is a cornerstone of BMS’s “Growth Portfolio,” its initial sales have slightly missed high Wall Street expectations as the company works to shift deeply ingrained prescribing habits in the antipsychotic market.

What do real world psychologists say? Flying colours say Psychiatric times.

Sonde Health: A pioneer in “voice biomarkers.” Using AI to detect depression and respiratory issues through a 30-second voice clip. As the “Remote Patient Monitoring” market explodes in 2026, this “hidden” spoke could be a massive strategic asset.

The PRTC-E Update

If we look at the potential Peak Revenue from the current pipeline (especially LYT-100 and the Seaport/Vedanta royalties) relative to the Cash-Adjusted Equity, the ratio is screaming.

Market Cap: ~£300m ($425m)

Net Cash & Liquid Assets: ~$320m (Covers ~75% of the cap).

Implied Value of Internal Pipeline & Spokes: Nearly Zero.

By my calculations, you are buying exposure to potential blockbusters at a price that implies they have a 0% chance of success. This, despite PureTech having a ~80% clinical success rate across its history.

Why the Market is Wrong (Again)

The City doesn’t understand “Hub and Spoke” models. They want a simple “one drug, one binary outcome” story. PureTech is a “complex” story of royalties, equity stakes, and internal R&D.

The Oak Bloke likes complex. Complex is where the mispricing lives. With Robert Lyne now firmly in the CEO seat and a leaner, meaner strategy (offloading Phase 3 costs to entities like Celea), the “momentum” is starting to shift.

The Verdict: Stick to the Spreadsheet

Most investors are “miserable” because the share price has crossed below its 50-day moving average. They see a chart; I see an opportunity.

PureTech is currently a “Value” stock wearing a “Biotech” mask. If you believe in the PRTC math, you don’t care about the 50-day average. You care about the fact that you’re buying a dollar for fifty cents.

The math is right. The price is wrong. I’m staying the course.

Regards,

The Oak Bloke

Disclaimers: This is not advice; make your own investment decisions. Micro-cap and Nano-cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip.”

Thanks for answering my question about PRTC on Vox Markets today. A very enjoyable show which you clearly demonstrated your detailed and Informed knowledge. No surprise when you consider the quality of the articles you produce. Hopefully it will soon be PRTC’s time to shine ! Thank you OB

Thanks OB. So many great articles in one day, you must be plum tuckered.

I've sold down some ITH today and entered the fray both here and ECOB. Potential for substantial re-rates look great at both.

Full marks 👏👏👏