PSH-PSH-PSH-teecuff - OB 2025 Idea #2

Pershing Square - a train station - and Bill Ackman's FTSE100 Fund

Dear reader

Pershing Square Holdings, based in NY, is so named for its offices overlooking Pershing Square, Manhattan. Which, in turn, is named after the “Eisenhower of World War One” John Pershing. Commander of the American Expeditionary Forces 1917-1920, Pershing was the only US General to become a 4 Star General in his lifetime.

Arguably PSH’s CIO Bill Ackman is a 4 star general in his own right. Self made from zero to $9.3bn - a true American success story, a poster child for “the land of opportunity”. This is a great interview to understand the lead person behind PSH.

PSH famously bet against covid. Or at least it bought swaptions in December 2019 totalling $27m that paid out $2.6bn in 2020. And crucially paid out just after a major crash of 2020’s lockdown. Ackman then swiftly swooped - buying Agilent, Berkshire, Hilton, Lowe’s, Restaurant Brands and Starbucks. Made billions more.

PSH repeated its party trick in 2022 betting inflation would drive interest rates up. Well, reader, you know what happened next. And PSH profited by $2bn.

A major reason that PSH is one of the Oak Bloke picks for 2025 is the possibility that things could go horribly, horribly, horribly wrong in 2025. I hope not. But the S&P500 is at a high valuation multiple and Trump’s favourite word could get us all into trouble. The trouble is history. Two gents called Reed Smoot and Willis Hawley aren’t names you are probably familiar with. But eagle-eyed readers will spot I’m referring to the Smoot-Hawley-Act - which contributed to the 1929 crash. In fact the parallels are very real.

Giddy excitement about the potential for Tungsten prices to shoot upwards abounds as I covered recently in “Tungsten got Tougher”. But there’s a darker side to trade wars and restrictions. Lots of casualties in a trade war even if the blood on the streets is metaphorical.

If so, then PSH is a potential insulation against that. If history isn’t instructive and tariffs are a smoke screen or negotiation tool so we see further upward movement in the US in 2025 then the PSH portfolio offers upside too. Its holdings are a series of ways to profit from businesses which are fundamentally undervalued and offer growth - at a double discount. PSH trades on a 35% discount to NAV currently.

Universal Music Group (“UMG”) 32.44% of NAV

UMG own numerous brands including EMI, Capital, Abbey Road, Island. Music revenue is via streaming but also through licencing. Consider all the ways you interact with music in your personal and professional life.

Universal powers all the streamers and social platforms “powering” ~9.5bn users. 9 out of 10 of the world’s top 10 artists for the past 10 years are housed at UMG.

Music on a cost per hour basis is one of the cheapest forms of entertainment.

It’s true UMG’s shares experienced a sharp drop following its 2Q24 results in July.

This was despite overall revenue growth of 10% and operating income growth of 11%, the problem was a deceleration in subscription and streaming revenue growth to single digits. PSH believe the quarter’s disappointing subscription and streaming growth is due to certain idiosyncratic and temporary factors. Specifically, the clock stopped at Tiktok and negotiations impacted revenue for half the quarter. The same with Meta. Both negotiations are now resolved.

Music streaming is still growing at a healthy rate. PSH believe that UMG’s underperformance this quarter will prove to be short term in nature and does not impact UMG’s medium and long-term growth prospects. PSH continue to believe that music has a long runway of future growth, as it remains under-monetised relative to history and when compared to other forms of media. It is double to what it was under “Napster days” of the 2010s but in real terms spend is about half of the 1990s.

PSH expect the industry to improve monetisation through new products and services, with better segmentation of customers including higher-priced “premium” tiers and increased subscription prices. You only have to hear news about “poor” Oasis missing out on ticket tout pricing to understand that the value of music far exceeds its price to its fans, particularly its superfans. UMG are working on ways to target superfans.

UMG’s management team led by Sir Lucian Grainge has a long track-record of growing and shaping the music market by working with its partners in innovating creative solutions to drive growth. For example, UMG’s efforts led to the industry-wide adoption of “artist-centric” initiatives that will result in a greater share of streaming royalties for its artists. UMG is also leading the industry by working with partners to launch new products to harness AI’s growth opportunities while also ensuring regulatory and legal protection for its artists.

As the world becomes “more like the West” is it reasonable to think there is a vast runway of growth from the East and the developing world.

Alphabet (“Google” or “GOOG”) 13.5% of NAV

Alphabet, the parent company of Google, delivered stellar business results in the first half of 2024. Revenues grew 14% powered by Google’s dominant position in the fast-growing digital advertising market as well as certain company-specific tailwinds including the increasing adoption of AI automation tools by advertisers and YouTube’s continued success in the Connected TV Medium.

Strong revenue growth coupled with cost control initiatives and stable staffing levels (headcount has remained flat year-to-date), resulted in strong operating leverage. Operating profit margins expanded approximately 340 basis points, excluding one-time severance and real estate charges.

In the second quarter, the company’s Cloud segment outpaced its major competitors with 29% revenue growth and achieved 11% profit margins, after first reaching profitability just 18 months ago. Google “own” the majority of the Fortune 500.

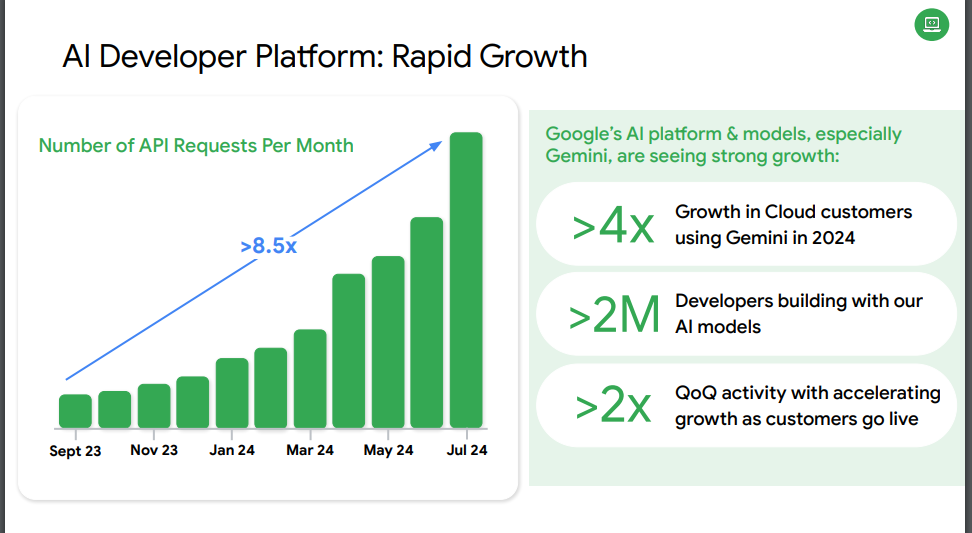

Amidst solid financial performance, Google is achieving notable milestones in its AI product development roadmap. At its annual developer conference in early May, the company unveiled the broad rollout of “AI Overviews”, which are AI-powered summary responses for certain types of queries. Early results from AI Overviews highlight how thoughtful integration of AI into Search not only improves the user experience, leading to more frequent and detailed queries, but also creates opportunities for greater ad monetisation through context-rich responses and higher conversion rates. Due to the encouraging initial success of its AI offerings, Google is meaningfully ramping up its AI investments and is on track to spend nearly $50 billion in capital expenditures in 2024, a more than 50% increase compared to the prior year.

PSH believe this increased level of investment will further differentiate the company’s technical infrastructure and cost-to-serve advantage relative to competitors. As a proof point, compute costs for Google’s generative AI search responses are down 80% from just a year ago. Such step-function improvements uniquely position the company to scale its AI capabilities to a user base of more than two billion consumers. Despite the material increase in infrastructure investments, the company remains committed to returning capital to shareholders and recently initiated a quarterly dividend of $0.20 per share, a ~0.5% dividend yield. The dividend supplements the company’s ongoing share repurchase program of approximately $16 billion in quarterly buybacks, which represents capital return equivalent to ~3% of the company’s market capitalisation on an annualised basis. The company also recently announced the appointment of Anat Ashkenazi as its new Chief Financial Officer. Anat had previously served as the CFO of Eli Lilly where she spent 23 years in various senior finance and operational leadership roles. PSH believe Anat’s extensive experience at Eli Lilly managing a complex, multiline business through multiple investment cycles will prove highly valuable as Google invests behind long-term AI initiatives while maintaining its strong commitment to cost control. Outgoing CFO, Ruth Porat, will take on a newly created role as President and Chief Investment Officer of Alphabet, including oversight of its portfolio of “Other Bets”. PSH look forward to Ruth’s impact on scaling and commercialising the company’s Other Bets ventures, including its promising autonomous driving subsidiary, Waymo.

PSH have been closely following the recent federal court ruling against Google in the Department of Justice’s antitrust case on the company’s default search agreements with Apple and Android OEMs. Google is appealing the decision and anticipates a resolution of the appeals process or a ruling on potential remedies to take at least several months, and potentially more than a year. PSH will continue to closely track developments in the case but believe that even in a scenario where Google loses its appeal, the company is well-positioned to navigate a range of likely potential remedy outcomes.

Hilton (“HLT”) 10.2%

In 2024 HLT generated strong revenue growth as the lodging industry experienced solid global demand against a favorable supply backdrop. Near-term industry trends remain positive, with continued strong international growth, improving business transient demand and extremely robust group demand, which is poised to sequentially accelerate in the third quarter. Demand supports the continued expansion.

Leisure travel continued to moderate from the high levels of recent years following the COVID-19 reopening. In the second quarter, HLT’s revenue per room (“RevPAR”), the industry metric for same-store sales, increased 3.5% as compared to 2023. Combined with strong 6% net unit growth, aggregate fee revenues grew 10%.

Earnings per share grew 17% year-over-year, benefiting from Hilton’s excellent cost control and continued best-in-class capital return. Reflecting an incrementally challenging macroeconomic picture, principally in China, the company slightly reduced the upper end of their prior RevPAR guidance, now estimated by management to be +2% to +3%, while modestly increasing full year’s earnings guidance.

Net unit growth continues to accelerate towards Hilton’s 6% to 7% long-term growth target supported by new brand concepts including Spark and LivSmart Studios by Hilton. Over the coming quarters net unit growth will be further boosted by Hilton’s acquisition of Graduate Hotels and the on-boarding of properties from Hilton’s partnership with Small Luxury Hotels of the World (“SLH”), which is seeing better-than-expected owner uptake with 400 hotels poised to join the Hilton system. The SLH partnership expands Hilton’s network into a new category of hotel, while providing incremental sources of value for Hilton Honors members and travelers. While Hilton only earns fee revenue on the proportion of sales that comes through Hilton’s channels, the comparatively higher average nightly rate of SLH hotels relative to Hilton’s systemwide average means that even modest penetration levels could become a meaningful incremental fee stream to Hilton. Over the medium-term, strong net unit growth combined with continued RevPAR growth (which has compounded at a 3% rate over the last 15 years) and a double-digit rate of growth from Hilton’s non-RevPAR fee revenue, which comprises about 20% of revenues, all combine to generate strong high-single-digit revenue growth. Coupled with excellent cost control, high incremental margins, and a substantial capital return program Hilton should continue to realise robust mid-to-high-teens compounded earnings growth for the foreseeable future.

Restaurant Brands (“QSR”) 10.2%

QSR’s two largest brands delivered impressive results this quarter. Tim Hortons’ same-store sales in Canada grew by nearly 5%, outpacing all competitors and the broader industry. These strong results are due to the multi-year investment the company has made in broadening its food platform and expanding its lead in cold beverages. Burger King International reported same-store sales of more than 2%, despite ongoing boycotts of western brands. Burger King is outperforming McDonald’s on a one-year basis and relative to pre-covid levels. Its success in international markets provides a blueprint for its ongoing turnaround in the U.S., where the company is focused on modernising its store base and growing its digital business. As part of that effort, the company acquired Carrols, Burger King’s largest franchisee, which will allow the company to accelerate remodels and help shift the franchise system towards smaller more entrepreneurial operators, setting the brand up for long-term success. The company intends to refranchise the Carrols restaurants to smaller operators once the stores are performing at strong levels. In light of weakening economic conditions and ongoing boycotts, the company lowered its net restaurant and system-wide sales growth outlook this year. In response, the company is enacting a cost savings program which will enable it to grow operating profits by more than 8%. While an uncertain environment may impact unit growth in the near-term, PSH believe each of the company’s brands will benefit in a slower economic environment with consumers trading down. Despite strong performance at its largest brands, consistent operating profit growth, and a business model that benefits in a recessionary environment, QSR still trades at a meaningful discount to its peers. As the company returns to its historic midsingle-digit unit growth and delivers consistent performance at each of its brands, PSH believe the company’s share price will more accurately reflect its improving fundamentals.

Chipotle (“CMG”) 9.6% of NAV

On August 13th, Chipotle announced that CEO Brian Niccol would be leaving the company to become the CEO of Starbucks. Brian has led a superb turnaround at Chipotle, which has put the company firmly on the path of sustainable long-term growth. While we are disappointed to see Brian go, one of the measures of a great CEO is the company that he leaves behind. Brian has built an extraordinary team at Chipotle that we expect will not lose a step in his departure. We are grateful to Brian for the extraordinary value he has created for CMG shareholders and Pershing Square. Chipotle delivered outstanding results in the first half of 2024 as the brand’s industry-leading value proposition of fresh food, customisation, and convenience at fair prices continues to resonate with customers.

During the second quarter, same-store sales grew an impressive 11%, or 55% from 2019 levels. Successful marketing, including the return of the fan-favorite Chicken Al Pastor limited time offering, and faster throughput drove transaction growth of over 8%, with gains across all income cohorts. Although sales growth has moderated in the summer amid a broader deceleration in the restaurant industry, Chipotle continues to gain share. The launch of Smoked Brisket for a limited time starting in September, one of the company’s most requested menu items, should further improve trends. Strong sales growth and more efficient operations led to restaurant-level margin expansion of 140 basis points in the second quarter. We believe that Chipotle’s attractive economic model remains firmly intact despite several near-term headwinds, including higher avocado costs and investments in improving portion consistency, the latter of which is already producing improvements in customer survey scores. Management has several exciting initiatives underway to simplify operations and improve throughput, including optimisation of staff deployment as well as new equipment and automation technology. The dual-sided grill, which can cook chicken and steak in less than half the time as the current plancha with more consistent execution, will be deployed in 84 restaurants by the end of this year, ahead of a broader rollout. Longer-term, the fully automated digital make-line, which will be installed in a restaurant for the first time this summer, has the potential to have a transformational impact on throughput and the customer and employee experience. Chipotle is on track to open approximately 300 new restaurants this year, and expects to more than double its store base to at least 7,000 locations in North America over time. International expansion beyond Canada remains a largely untapped opportunity. The new leadership team in Europe is making good progress on improving unit economics of the company owned stores, while Chipotle’s first franchised restaurant in Kuwait is off to a great start.

Howard Hughes (“HHH”) 9.6% of NAV

HHH’s results through the first half of 2024 demonstrate solid business momentum across all segments, highlighting the advantage of owning master planned communities (“MPC”). In its land sales segment, the company is on track to generate nearly $300 million in full-year profits. New home sales, a leading indicator for future homebuilder demand for land, continues to be supported by limited supply of resale housing inventory and the highly desirable qualities of HHH’s amenity-rich MPCs, which are well-located in growth markets with favorable demographic trends. The strength of this demand is most clearly evident in the pricing the company is able to command for its residential land, with its average price per acre reaching an all-time high of $1.0 million in the most recent quarter. In the company’s portfolio of stabilised income-producing operating assets, net operating income (“NOI”) grew 4% on a samestore basis during the first half of the year driven by strong leasing momentum and steady rental rate increases. In its Ward Village development in Hawaii, HHH continues to experience robust sales momentum. The company has pre-sold 51% of inventory at its newest condominium tower, The Launiu, despite only having launched sales in February. Outside of Ward Village, the company is developing its first condominium project in the Woodlands, the Ritz-Carlton Residences. As the first-of-its-kind luxury development in Houston, the Ritz-Carlton Residences has been met with tremendous demand and has already pre-sold 65% of its available units, representing future revenue of $313 million. On August 1st, the company successfully completed its spin-off of Seaport Entertainment Group (NYSE: SEG), which is comprised of the Seaport District in New York City, the Las Vegas Aviators minor league baseball team and certain other noncore entertainment assets. Under the leadership of CEO Anton Nikodemus, former President & COO of MGM CityCenter and an entertainment industry veteran with over 30 years of experience, PSH are optimistic that SEG will unlock the significant embedded upside potential in its unique collection of assets. PSH is retaining its shares of SEG received from the spin-off and, along with the other Pershing Square funds, has entered into a standby purchase agreement to backstop a $175 million rights offering which SEG intends to launch shortly. Proceeds from the rights offering will provide SEG with the required liquidity to execute on its growth plan. Pershing Square is the largest shareholder of SEG. Anthony Massaro, a member of the investment team, has joined the Board of SEG. PSH believe the separation of SEG further positions HHH as a streamlined, pure-play MPC company with a decades-long runway for growth. PSH intends to continue its investment in HHH, including a possible transaction in which it may acquire all or substantially all of the shares of HHH not owned by them and their affiliates and in connection therewith take HHH private.

Canadian Pacific Kansas City (“CPKC”) 8.9% of NAV

In 2023, Canadian Pacific’s transformative acquisition of Kansas City Southern established the only railroad with a direct route linking Canada, the United States, and Mexico. The combined network connects shippers to new markets and enables nearshoring in North America while creating significant shareholder value.

CPKC celebrated the anniversary of its acquisition with a second year of growth in this multi-year growth story. Volume growth of 6% in the second quarter was well ahead of management’s expectations, driven by synergy wins and solid Canadian grain shipments. CPKC has made considerable progress on realising revenue synergies despite a challenging freight environment, and now expects to exit 2024 with C$800 million of new business. These wins span a wide variety of endmarkets from automotive to corn, demonstrating the unique value proposition of CPKC’s network.

Cost synergies are also tracking ahead of plan as CPKC realises savings from combining procurement and general and administrative functions. These cost savings together with strong operations across the network led to a 280 basis point yearover-year improvement in CPKC’s adjusted operating ratio in the second quarter. PSH believe that CPKC’s one-of-a-kind network and industry-leading management team are well positioned to deliver continued synergy wins and excellent operations, which should generate strong double-digit earnings growth in the coming years.

Brookfield 10.9% of NAV

With $900bn AUM, where those assets are employing ~240k operating employees Brookfield is the biggest company you’ve never heard of. Turning $1m into $143.3m is a great party trick though.

BN operates in the areas of Private Equity, Infrastructure, Renewables, Insurance and Asset Management. Its balance sheet is geared through a structure of borrowings ($322bn) and non-controlling interests ($122.5bn) and Preference Shares meaning ordinary equity (including PSH’s 10% holding) of $40bn gets magnified.

But the non-controlling interests reduce the distributable earnings and FCF by about 80% so ~$1bn is over 1.5bn shares about 67 cents (on a $60 share). FCF is actually ~$9bn for ordinary holders… $6 per share.

By continuing to grow the business, forecast 2028 earnings will be double that of today.

But if the business ploughs cash back in for further growth then earnings will be 2.6X today.

Fannie Mae and Freddie Mac

Fannie Mae and Freddie Mac remain valuable, effectively perpetual options on the companies’ exit from conservatorship. They are fully capitalised and their exit would also reduce the Federal Government’s liability i.e. it moves it off balance sheet.

You’ve got to imagine this would be an attractive option for the likes of the business minds of Musk and Trump.

If this happens PSH stand to gain an unspecified upside.

Swaptions

These are murky and undisclosed but you can bet that Bill Ackman has some 1000-to-1 bets on certain events happening or not happening. If there is a run on the dollar it wouldn’t surprise me if PSH were positioned to profit (protect) from such a scenario; or if the S&P were to precitiously plummet that an option or put would provide some protection.

I can only point to the superb track record for the value of this.

Bringing it all together

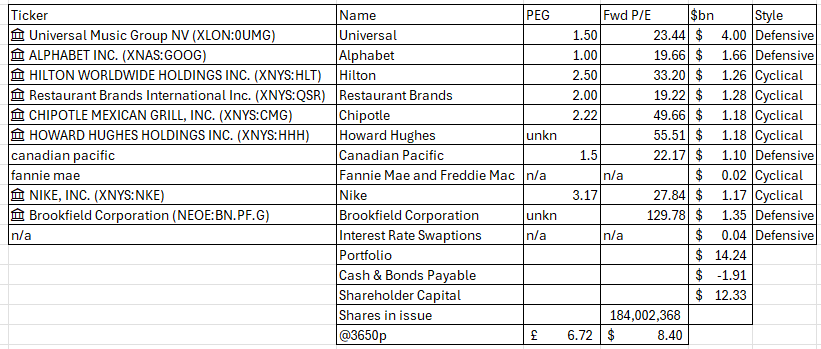

This was a PSH disclosure as at 31/10/24:

This meanwhile was the last “official” balance sheet as at 30/06/24.

This is (as best I can determine from the various disclosures) the approximate current position of PSH. You have to be comfortable with the idea (probably unsurprisingly) that PSH don’t signal and share exact positions and positioning. Tomorrow the wind might change and they decide to sell a position to triple a position. Shareholders get limited pontification rights.

So at 3650p you are paying £6.72bn or $8.4bn to buy PSH.

If you agree with my analysis that music fees, internet advertising and data centres, train transportation, infrastructure are all defensive then that covers $8.11bn. The swaptions would be worth $1bn++ in the event of a “defensive” event occurring so I am going to value that at $0.29bn.

By that logic you are getting $4.18bn of holdings (i.e. about 1800p per share bought) in Hilton, Restaurant Brands, Chipotle, Howard Hughes and Nike all for free. And Fannie/Freddie too.

If you disagree that Swaptions should be valued at $290m then change the word free to a 93% effective discount.

So a circa $4bn of discount, a $1bn+ parachute if the wings fall off the world economy in 2025, growing businesses, with Bill Ackman and Team - smart cookies - running the show.

Lots to like with PSH. And don’t fall off your chairs that I’ve picked a FTSE100 stock. Perhaps I’ll pick another. Cash generation is a watch word in the OB picks for 2025.

Regards

The Oak Bloke

Disclaimers:

This is not advice - make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

BIG THANK YOU TO THE 12 FOLKS WHO’VE DONATED SO FAR FOR 2025. FOR THE THOUSANDS READING THIS PLEASE DO THE SAME. KEEP IT FREE.

IT’S COLD OUTSIDE. YOU’D BE GOING PSH-PSH-PSH WITH THE COLD IF YOU WERE HOMELESS. LET’S SOLVE THE HOMELESSNESS PROBLEM TOGETHER WITH A HAND UP NOT A HAND OUT SUPPORTING EMMAUS.

Excellent write up! Thank you.

Thanks OB. Another one to maybe compare/contrast with this is Canadian General Investments. Also sitting on a huge discount but I think without the derivatives