Three Disconnects

Deep value that doesn't make sense

Dear reader

More evidence the reign of the Small Cap has returned. Can you spot a theme to the top funds for May 2024?

I’m not writing specifically about Small Caps today - instead I want to write about some holdings that make no sense:

3 NO SENSE HOLDINGS

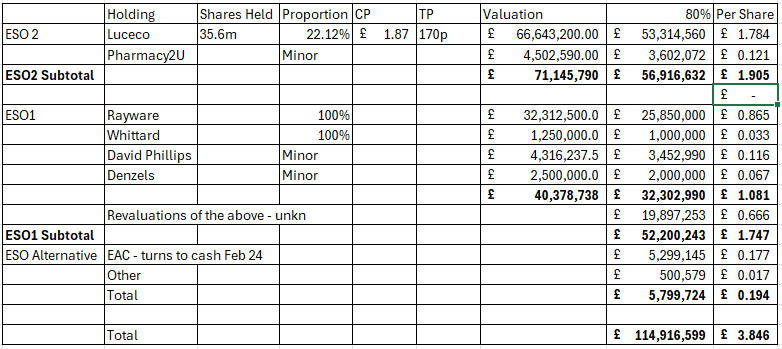

1# ESO:

I see Liberum have increased their target on Luceco to 192p. It’s 5p below that, and ESO’s 35.6m shares in Luceco are now worth £53.3m.

£53.3m is more than the ESO Market Cap.

In fact if you strip out cash (£19.8m), debt (a bond) )(-£18.4m) and the listed Luceco holding ESO is on a 112% discount to NAV.

You are actually getting paid £5.5m to own 100% of Whittards of Chelsea, 100% of Rayware (worth around £46m), and 3 minority stakes worth around £10m (book value).

Also see my article “A net of 0p for 21.2p of cash and 188.4p of holdings”

#2 VSL

VSL posted a positive +0.64% return in March (positive both for loan revenue and for equity) but the share price has fallen yet further. VSL holds high interest secured loans and equity positions in mainly US Fintech/eCommerce companies. It’s fallen to the point where the entire Fintech/Ecommerce equity holdings could be wiped out and worth zero and there’s still 25% upside from the loans. Loans where VSL is Senior and Equity where VSL has preference.

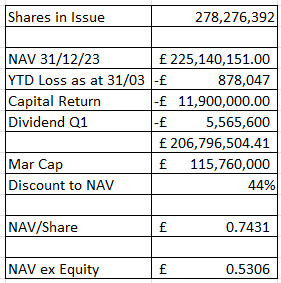

A 44% discount where dividends and capital returns over the next 12 months alone should be a further 8p+16p = 24p.

On a simple returns basis that leaves you owed 16.5p a share, while the remaining NAV could be around 60p a share net assets…. a 72.5% discount to NAV.

With further capital, dividend returns, and equity holdings which might surprise to the upside, I reckon you could get to a <100% discount to NAV in due course.

#3 TMT

More positive news from TMT. Two more uplifts.

Their holding OneNotary (https://onenotary.us) completed its Series A equity funding round of US$5m and entered into a partnership with Docusign (NASDAQ: DOCU) to provide Docusign Notary (powered by OneNotary).

OneNotary is the only digital service recognised in all 50 US States and offers a subscription and ad hoc option. It already has 30,000 notaries on its system. It is being rolled out to all Docusign customers imminently.

The transaction represented a revaluation uplift of 85% (US$0.4m) in the fair value of TMT's investment in OneNotary, compared to the reported amount as of 31 December 2023.

Praktika

Praktika.ai is a language learning app with personalised AI-powered avatar tutors.

Bit cheesy but a great idea - I tried it out and it works brilliantly:

Praktica has completed a new US$35.5m Series A equity funding round, led by Blossom Capital. The Series A equity funding round represented a revaluation uplift of 1,144% (US$4.6m) in the fair value of TMT's investment in Praktika.ai, compared to the reported amount as at 31 December 2023.

This positive revaluation of 12.4x in only 5 months represents the fastest significant revaluation of a portfolio company in TMT's 13-year history.

At the end of May 2024, Praktika reported 1.2 million active monthly users across 100 countries, with revenue of almost US$20.0m in the last twelve months.

Backblaze and Bolt

There is a corresponding reduction in TMT’s NAV due to Backblaze falling from $7.59 a share to $6.02 post period.

However the read across from Uber and Lyft continue to suggest that Bolt offers potential upside. Bolt expects to turn profitable in the next 12 months and its CEO Villig said the company is doing single-digit billions of dollars of transactions on the platform every year.

We do know Bolt reported net losses of just €72 million on €1.26 billion in revenue in 2022, where revenue grew 152% year on year. Judging by the growth in the number of cities and countries served the “low single” must be at least €2 billion in revenue, putting Bolt at 1/18 of Uber’s revenue. 1/18 of its market cap would be just over $8bn - which was the valuation in its 2022 upround.

TMT’s NAV and estimated discount to NAV:

Once again the last official discount was 49%. Given the movements and read across values the discount rises to 58%. TMT owns 1.26% of Bolt and values it at $72.2m, which puts Bolt on a $5.73bn valuation. This is a 31.7% discount to the last funding round which was $8.4bn. So the mark-to-market approach and comparisons of number of drivers, of number of customers, of estimated revenue, and the 24 months of news flow all resonate with Bolt.eu being worth more than a $5.73bn valuation. It could well be worth more than in 2022. There are other examples like Klarna or Starling where the prior valuation are likely to be exceeded.

If you agree with that, and if you therefore stripped out cash, the $112.80m “proper” valuation of Bolt.eu, the 3m shares in BLZE (at their current depressed price) you actually end up at 129.42% discount to NAV.

So that means you pay $106.3m to receive $137.6m, theoretically.

So you are being paid $31.3m to have 55 other holdings for free, 11 of which increased in 2H2023 and 2 increased in 1H2024 - by over $15m.

Conclusion

If this were anything other than 3 overlooked shares, people would think you were either mad or wrong. Surely it’s too good to be true. Or is it?

Three companies where you literally can pay to get paid, and then be gifted assets that cost you nothing.

I could list other holdings BSRT, GROW, CGEO, NSCI, TEK and others which belong in this list too.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

ESO does make some sense. If you check the liquidity of the listed holding, it’s effectively illiquid. It would take months and or a large discount to current market price to realise current value.

How long do you estimate the time to wind down VSL Oak?