THS might be a good time for THS

Shock news from Johnson Matthey that PGMs have been in deficit since 2023

Dear reader

We were meant to all be abandoning ICE cars, going electric and PGM demand would plummet. Prices did plummet of course. Back in 2021, Rhodium was $14,000 an ounce (it touched $23k I think) and holdings like Sylvania Platinum (SLP) was one of my largest holdings. SLP gave a magnificent 10% a year dividend. After seeing a wobble I exited. A crash ensued. So I was very surprised to read Johnson Matthey’s 2024 PGM Market Report speak of “the largest supply shortfall in 10 years”.

Eh?!

The theory behind PGMs seemed sound. Yes, ICE vehicles would decline, but hybrids need even more PGMs, Plug Ins more so. Meanwhile industrial demand would continue to grow and its use for pollution control a further growth area. Finally the Energy Transition requires PGMs. A 1 GW Wind Turbine uses about 10,000 tonnes of glass fibre and 1 GW Solar Farm 3,500 tonnes of Glass Fibre. In case you’re wondering what Glass fibre has to do with PGMs well production of glass making (including glass fibre) needs PGMs. PEM Electrolysers need them too, as part of the catalyser.

“PGMs” probably need some explanation. There are several PGMs or Platinum Group Metals and Platinum itself is probably the most well known. Followed by Palladium and both of these are used in catalytic convertors. You then have Rhodium, also for catalytic converters, and Ruthenium (Chemicals & Electronics), Iridium (Electrochemical) and Osmium (Fountain Pen Tips and a catalyst). A feature of PGMs is you can “thrift” which is to find ways to reduce their use as well as substitute one for another. For example devise ways to replace palladium and rhodium with platinum - as has happened - Palladium and Rhodium being particularly expensive were thrifted and susbstituted for cheaper Platinum. But also Chinese glass makers, particularly, found so many ways to replace Rhodium that they had excess and at record high prices they sold their rhodium and the volumes being dumped on the market, combined with an uptick in PGM production in South Africa crashed the price. Since then South African Rhodium production has fallen by 10%, rhodium recycling has fallen by 20%, while automative demand has fallen by around 7%.

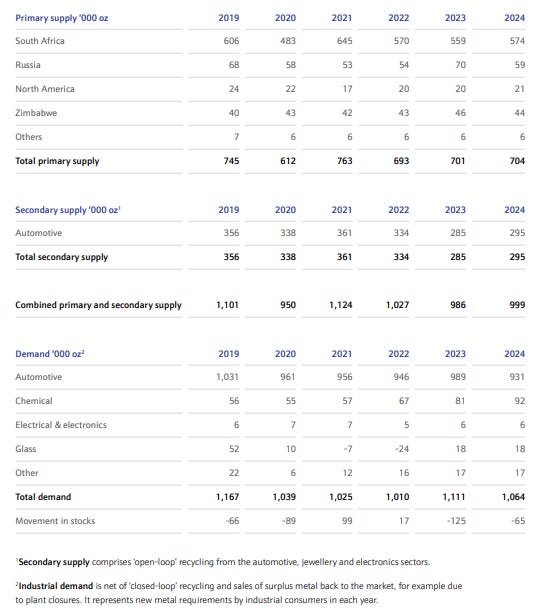

This chart from Johnson Matthey confirms Platinum has automotive and industrial growth forecast for 2024, and a 598Koz shortage - and that’s based on some aggressive EV growth. “Aggressive” translates from 11% of light vehicles in 2023 to 14% in 2024 according to the IEA.

In the chart above is firm evidence that sentiment - not just fundamentals - can drain or flood the PGM market.

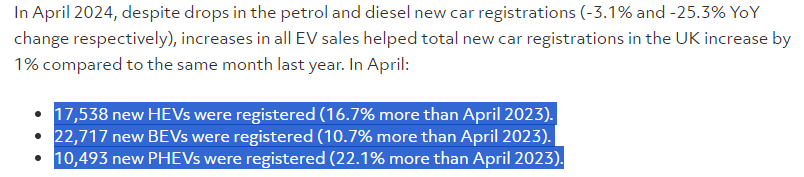

But what if that EV growth is being outpaced by the growth of ICE vehicles with a hybrid or plug in hybrid capability? Demand for PGMs (including Rhodium) would be higher than even Johnson Matthey expects. Potentially much higher. Latest numbers appear to confirm this where HEV and PHEVs are growing faster than BEVs - at least in the UK. 28k non BEVs vs 22.7k BEVs. And growth of non-BEVs is faster.

What if you knew that PHEVs require 5%-10% MORE PGMs (than non-hybrid ICE cars) not fewer?

The answer, reader, is you’d have the mother of all bull runs in what is a tight market where profits have smashed the balance sheets of the supply and rhodium can only increase in response to shortages.

What if you knew that PHEVs are able to deliver 2X-3X the electrical range compared to earlier models from just a couple of years ago? This is a link to the TopGear Top 10 PHEVs by Range - enjoy! - tell me which is your favourite PHEV :)

Investment Flows for PGMs

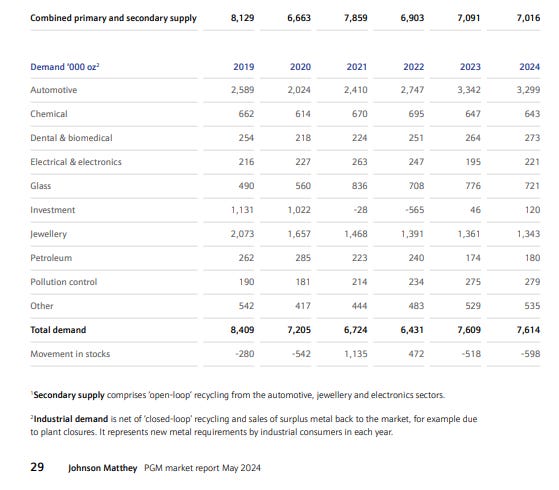

Returning to Platinum and looking at Platinum demand and supply in the diagram above, it is noticeable that investment flows in 2019 and 2020 of 1moz created a large deficit but subsequent reversals in 2021 and 2022 reversed that. There is firm evidence that sentiment - not just fundamentals - can drain or flood the PGM market. A rising number of people are now talking commodities, particularly Copper, Gold and Silver. How long until PGMs - the forgotten precious metal becomes the next hot idea? Especially as they play a role in Energy Transition - same as copper - and are a precious metal - same as gold and silver. In fact a quick scan of YouTube and the number of PGM tout videos has shot up.

In fact let’s compare Platinum and Gold. A week ago an ounce of gold could buy you 2.55 ounces of Platinum. But in the past week Platinum has outpaced gold to below 2.3 to 1, so a 10% improvement. Gold did fall about 4% from a high of $2,420 to $2,330 while Platinum strengthened about 6% - hence the upward line has started falling quite sharply. Perhaps that’s a co-incidence - or perhaps the start of a PGM move upwards?

What to do with this shock news?

I’ve compared Anglo, Sylvania, Jubilee and Tharisa. I’ve found I really like Tharisa.

Only 18% of Anglo American is PGMs and they are under bid takeover pressure due to their copper business so I’m excluding those. Too expensive. I’m excluding non-UK listed. This leaves Sylvania and Jubilee as options but more expensive on a P/E, P/B and FCF basis. Also on an absolute PGM ounces THS wins too. 131.4koz vs SLP’s 75.5koz vs JLP’s 43koz. THS recent Interim Results show a P/E of just 3.8.

Also JLP and THS are major Chrome miners while SLP doesn’t appear to be. Chrome is at elevated prices and South Africa supplies 44% of the world’s Chrome, and 80% of the Chrome to China (which has ramped up its imports).

Also THS is building a 2nd mine, Karo, slated for 2026 but is being built on a “go slow” as THS preserves cash during current low prices. Debt finance is being discussed, but it presumably hasn’t made sense to fast track this.

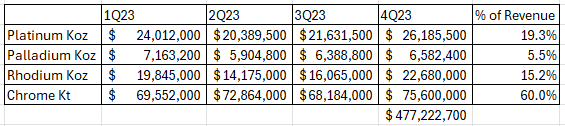

I next took Tharisa’s 2023 production and applied today’s prices so to get an idea of the product mix. THS appears to have a relatively high amount of Platinum and Rhodium.

This means even with fairly conservative reversion on prices (Rhodium returns to $10k and Platinum to $1.5k) an additional $122m would drop to the bottom line (PBT). That’s before we consider the future profit impact of Karo. That would equate on a share you can buy for 77p today to 41.9p per THS share extra profit.

Karo is a Tier 1 low-cost, open-pit PGM and Chrome asset located on the Great Dyke in Zimbabwe capable of 174 koz/year for 11 years LoM and NPV10 of $494m. Given the 131.4Koz it would more than double Tharisa’s PGMs and likely take Tharisa above $1bn revenue a year. The capital cost is $391m and $110.5m has so far been spent with spending slowed while debt capital is considered since cash flows are diminished with lower PGM prices.

The combined resource size for Tharisa Mine and Karo comes to 1Bt containing 52 Moz of 6E PGMs. Tharisa Mine has potential a 40yr life, of which the next 18 will be open pit, with a 20 year underground option. The I&I of Karo is 10Moz of 6E PGMs. This is based on 100m depth even though the resource goes to 1000m. In fact previous estimates of Karo by Zimplats, were 96Moz of 4E PGMs (so more inc. 6E) or c.10x the resource being currently measured in the Stage 1 production plan. Other benefits to Karo is a supportive tax regime of 15% for 10 years and ability to export (rather than sell to a government monopsony), and no BEE (black empowerment) legislation where you effectively give away a share of ownership for nothing. There are other miners in the area like Zimplats and Anglo so an educated and (mining) experienced workforce too.

Further Hidden Value

THS operates a “Mine-to-Megawatt” philosophy of vertical integration. So incredibly THS not only owns two Tier 1 mines (1 active, 1 under construction) but also downstream facilities too:

ARXO Metals produces specialised higher margin chemical and foundry grade chrome concentrates, operates Sibanye-Stillwater’s K3 UG2 chrome plant in Rustenburg and is the Group’s research and development arm. It also conducts research and development into technologies and beneficiation opportunities. Out of its testing site (AMBS) it operates a 1MW DC furnace to produce PGM-rich metal alloys with the aim to further beneficiate the PGM concentrate from the Tharisa Mine. This means THS can concentrate the PGMs to sell to smelters with a 97% payability rather than the standard 85%.

ARXO Logistics owned 100% by THS - manages the rail and road distribution of PGM concentrate and chrome concentrates produced by the Tharisa Mine, and chrome concentrates from Sibanye-Stillwater’s K3 UG2 chrome plant. These products are transported to customers in South Africa and international customers via port facilities in Richards Bay, Durban and Maputo, Mozambique.

MetQ (South Africa) owned 100% by THS - MetQ manufactures equipment used in the mining industry, with a particular focus on beneficiation.

Salene Manganese (South Africa) is an option THS has for 70% Salene Manganese’s principal activity is a manganese exploration and mining company. The Mining Right is for the mining of iron ore and manganese ore. Manganese recently shot up by around a third, and Iron Ore at around $120/tonne is not doing badly either.

Salene Chrome (Zimbabwe) is owned 100% and is an early stage open pit chrome project adjacent to the Great Dyke of Zimbabwe. Chrome prices are on a tear too.

Redox One – the final part of THS’ “Mine-to-Megawatt” launched their product at the Africa Energy Indaba. This is an energy storage not dissimilar to a VRFB but uses different chemistry i.e. an iron-chromium flow battery technology (ICRFB). It was “well received”, reports Tamesis. Demonstration units are being produced and tested in real world conditions. Eagle-eyed readers will know of the opportunity of Energy Storage which is worth around £0.4m/MWh of storage capacity or £0.04m/MWh under licence (these are my assessments based on available info - see my Trajectory of Invinity article). Assuming a capital light model and even just 200MWh being built under licence per year that’s £1m additional future profit with little or no marginal cost. 200MWh may sound a lot but IES have a 6TWh pipeline by comparison which would equate to £30m under a licence model (which was THS entire 1H24 profit). Of course this assumes THS’ technology is as good as IES which we simply do not know and is unlikely to be the case. In general, an ICRFB vs a VRFB is 4X cheaper but inferior in terms of longevity.

Conclusion

THS offers incredible value and the timing is now. Not only has THS been able to generate earnings of £60m a year during a time when PGM producers are suffering (mainly due to its Chrome byproduct sales), but it has fingers in a number of pies. Its 2nd mine is nowhere in the price and if/when PGM prices recover - and there appears to be strong evidence they shall and in fact are (28th May PGMs are up 2.7% as I write) - THS is incredibly well-leveraged for growth but also to take advantage. A 4X share price is conceivable (and the opinion of Brokers too). THS aren’t shy at giving dividends either.

The fact that PHEVs have improved, makes their popularity no surprise. No range anxiety combined with cheap electrical power bragging rights in a gorgeous car - what’s not to like? Rather than backing a car manufacturer, backing THS is a picks and shovels play to a PHEV’s popularity - and the insight that PGMs have been punished due to short term moves from running down stockpiles - which has masked and now demasks their long-term prospects.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip"

I've held for two years, through the dip and hoping for improvement now. I subscribe to the EV revolution gaining strength fast actually, but I'll take the PHEV benefit here if people insist on going slowly.