WISE cracks

The complicated and simple story of the unmatchable Take Rate

Dear reader

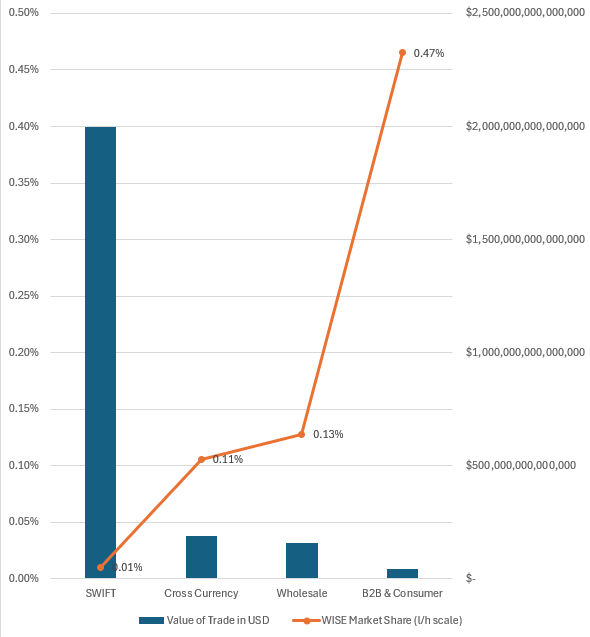

$2 quadrillion. That’s the value of funds which flowed via SWIFT in 2025.

SWIFT: Processes roughly $6 trillion every single day.

Wise: Processes approximately £150 billion ($200 billion) per year. That’s $0.0002 quadrillion. How’s that for a runway for growth?

The Reality: SWIFT often moves more money in one hour than Wise moves in an entire year. This is because SWIFT is the “backbone” for central banks, stock exchanges, and multinational payrolls, whereas Wise primarily handles smaller retail and SME transfers….. until recently.

$0.19 quadrillion. That’s the value of funds which flowed CROSS-CURRENCY in 2025.

Non-wholesale: $43 trillion of the $190 trillion were B2B and consumer payments.

SWIFT: $27tn is still moved via SWIFT

“Alternative Rails” non-SWIFT which includes Wise moved $16tn. Wise moved $200bn

It’s only when you put these numbers in a chart that you perhaps realise the scale of the opportunity for WISE. It has a 0.47% market share in B2B cross-currency payments. But only a 0.01% market share in the growing SWIFT payments market.

As of early 2026, Wise Platform has grown into a major infrastructure provider, used by over 100 financial institutions worldwide. Instead of competing with banks, Wise increasingly acts as the “plumbing” that powers their international transfer features…. it’s part of their wholesale banking.

The following banks and financial institutions currently use Wise’s platform to offer low-cost, high-speed cross-border payments directly within their own apps:

1. Major Tier-1 & Global Banks

Morgan Stanley (USA): In a landmark 2024/2025 deal, Morgan Stanley became the first major US investment bank to use Wise Platform for its corporate and private wealth clients.

Standard Chartered: Uses Wise to power its “SC Remit” service across Asia and the Middle East, allowing transfers in 21+ currencies.

Raiffeisen Bank International (Europe): One of the largest banking groups in Central and Eastern Europe recently integrated Wise to modernise its cross-border infrastructure.

Itaú Unibanco (Brazil): The largest bank in Latin America uses Wise to fill capability gaps for its international payment offerings.

2. Digital & “Neobanks”

Wise is the standard partner for the world’s most popular digital banks.

Monzo (UK): One of Wise’s longest and largest partners; all international transfers in the Monzo app are “Powered by Wise.”

Nubank (Brazil): Uses Wise to provide multi-currency accounts and international debit cards to its 100 million+ customers.

N26 (Europe): Fully integrated Wise into its app so users can send money in 30+ currencies without a separate Wise account.

Mox Bank (Hong Kong): Standard Chartered’s digital-only bank in HK uses Wise for its remittance services.

Bunq (Netherlands): One of the first European neobanks to integrate the Wise API for its “travel card” and transfer features.

3. Business & Specialised Banks

Allica Bank (UK): A leading bank for SMEs (Small and Medium Enterprises) that uses Wise to help business owners pay international suppliers.

Shine (France): A business-focused neobank for freelancers and small companies.

GMO Aozora Net Bank (Japan): Wise’s first major partner in the Japanese market.

4. Non-Bank Platforms

Wise also powers international payouts for companies that aren’t technically banks but handle large volumes of money:

Upwork: Uses Wise infrastructure to pay freelancers globally.

Tiger Brokers: An investment platform that uses Wise to allow users to fund their accounts and spend via a Wise-powered debit card.

Google Pay: In certain regions, Google Pay’s cross-border transfer feature is built on the Wise API.

Understanding WISE

1. The “Wise Platform” (Wholesale as a Service)

Wise has a division called Wise Platform that allows Tier-1 global financial institutions to use Wise’s internal “local-to-local” network instead of the SWIFT/Correspondent banking network.

Current Partners: As of early 2026, heavyweights like Morgan Stanley, Standard Chartered, Itaú Unibanco (Brazil), and Raiffeisen Bank have integrated Wise into their backend.

How it works: When a Morgan Stanley corporate client sends a cross-currency payment, the bank may route the “small-to-medium” portion of that flow through Wise’s rails to ensure it arrives instantly and cheaply, while keeping the client within the bank’s own branded interface.

2. Why Wholesale is only being addressed now:

There are two main barriers that Wise is only now overcoming:

Forward Contracts & Hedging: Traditional wholesale FX isn’t just “spot” trades (sending money now). It involves Forward Contracts (locking in a rate for X months from now). Until recently, Wise’s API only could handle “Spot.” Competitors like Mr Hill’s Equals Money remain ahead in this for the SME market, but Wise has pivoted by adding advanced Treasury tools to capture more of the B2B wholesale flow - and allowing banks to interact with their preferred choice of hedging tool(s).

Volume Limits: Until 2024, Wise had relatively low transfer limits. They have since introduced “Large Amount” transfers specifically for the wholesale and mid-market corporate sectors, allowing for multi-million pound single transactions.

3. The SWIFT “Co-opetition”

In a fascinating twist, SWIFT and Wise partnered in late 2023.

This allows a wholesale bank to send a standard SWIFT message (the language they speak), but have the actual settlement carried out by Wise (the rails they want).

This removed the biggest barrier for wholesale: the need to rewrite their entire IT system. They can keep using their legacy SWIFT terminal but get “Wise-like” speed and cost.

4. Market Share Gap

Wise’s share of the “Large Enterprise” and Wholesale market is still miniscule at 0.01%.

SWIFT Domain: Trillion-dollar interbank liquidity and government bonds will likely stay on SWIFT (or move to new Central Bank Digital Currencies/CBDCs) because they require “Finality of Settlement” that a private company’s ledger can’t always provide.

Wise Domain: The “commercial” wholesale market—global payroll, supplier payments for multinationals, and mid-tier bank FX—is where Wise is winning.

The economics of WISE

Consider that competitors cannot touch Wise.

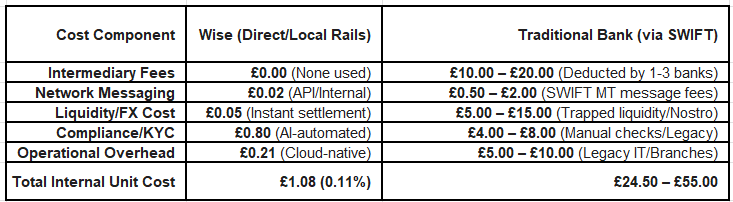

Legacy providers (Banks) have costs 20X-50X that of Wise. That’s COSTS. Not any gross profit, let alone net profit (which Banks want to make).

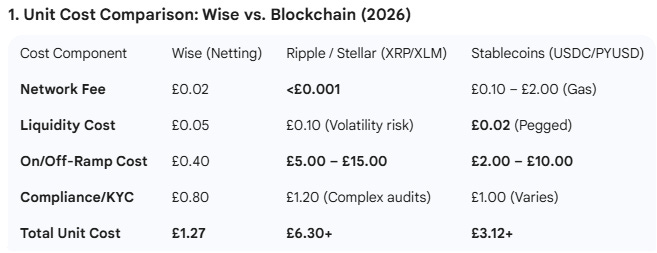

Other Fintechs cannot touch Wise either. While Blockchain “could” be cheaper in reality hidden costs mean it isn’t on a like-for-like basis. 3X more expensive at £3.12 per £1000 moved is the most optimistic cost and the true cost could be 13X more expensive (unluckily for them)

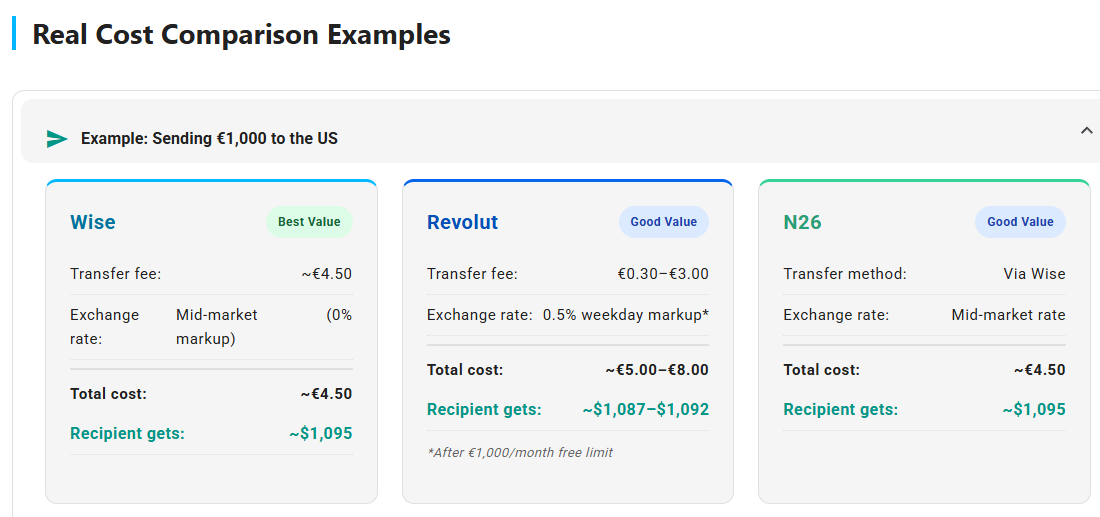

A leading blockchain OB idea would be Revolut (held via INOV or GROW), but Wise wins during the week and Revolut charges more at weekends or above a thousand Euros in a month.

Could Stablecoin eventually win out? Theoretically possible but unlikely. Every government of the world would need to give up their central bank, and their ability to print their own currency opting instead for stablecoins so that there was no longer any on ramp and off ramp (and good luck with that quest).

While national currencies remain the dominant form of exchange and while the banking system as we know it today remains in place, Wise with its long term 0.35% take rate will dominate.

Wise is part of the banking system and uses the banking system so needs no off ramp and on ramp.

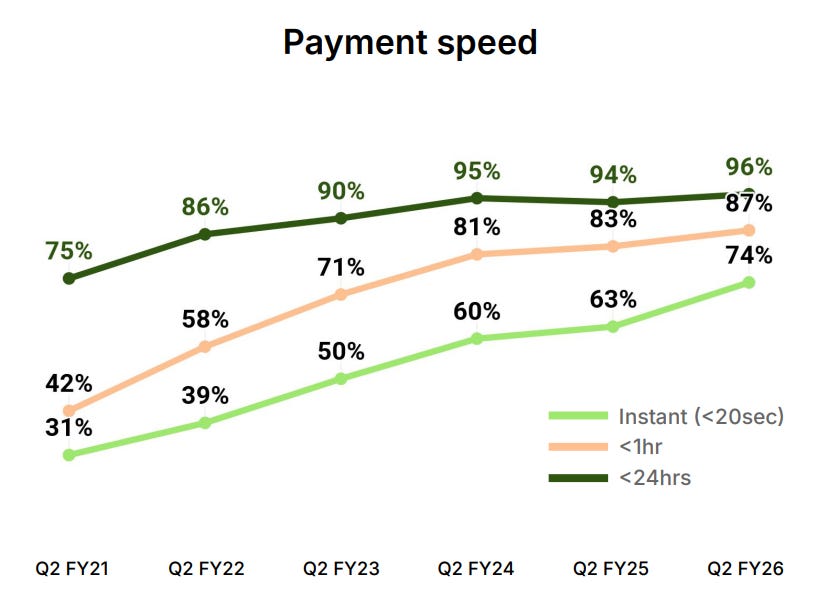

The Speed of Wise

WISE is not just about being cheaper, it’s also being faster. Faster means activity can happen faster

WISE FINANCIALS

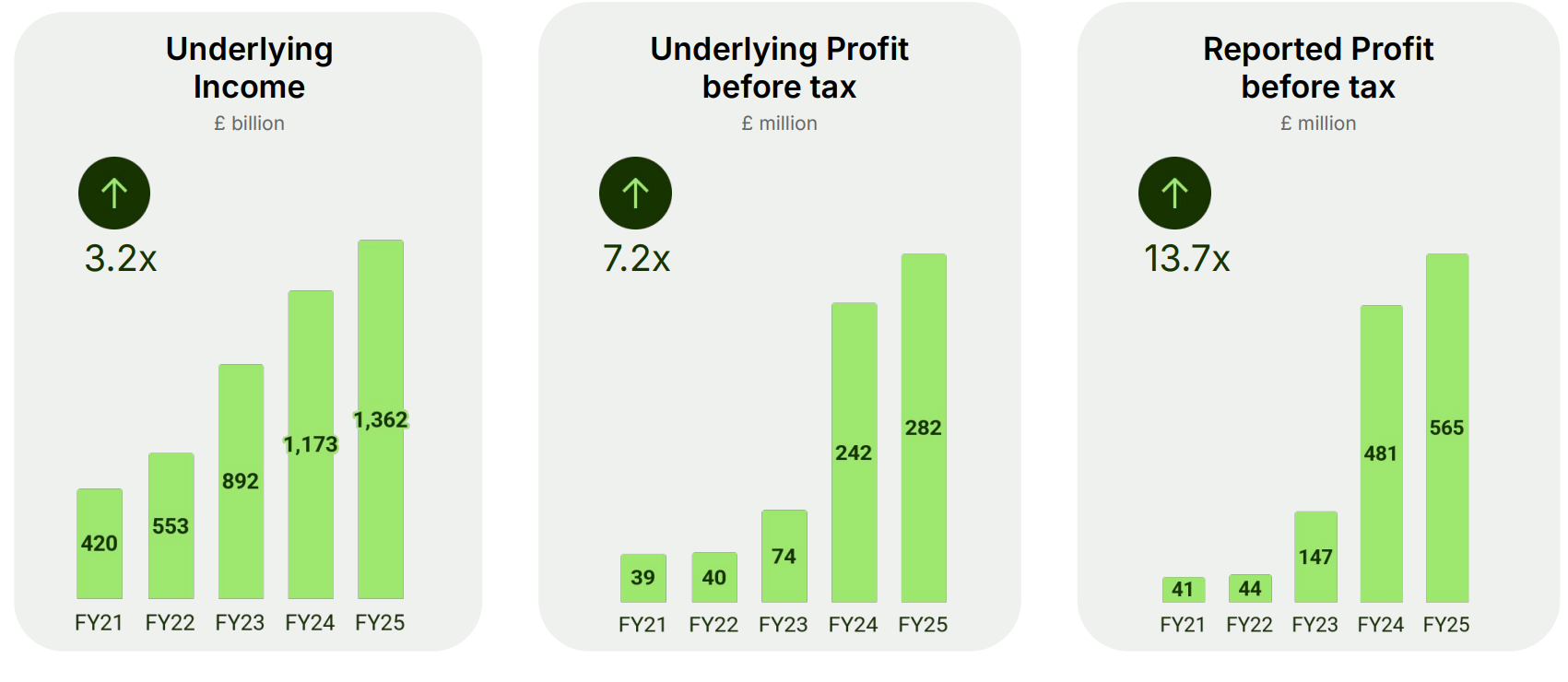

WISE is an £8.6bn marcap, down -19% since 01/01/2025 even though it continues to grow users, volumes, and continues to extend its presence into new countries such as South Africa, Philippines, Japan and India.

Profits which grew since FY21 are forecast to “stagnate” over the next few years but the word “stagnate” misses the point. What point is that?

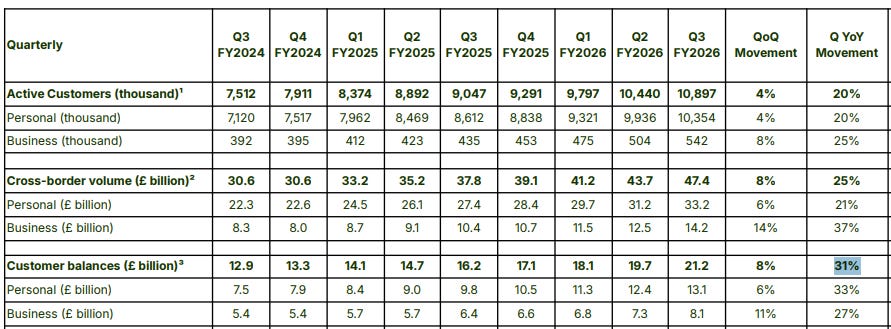

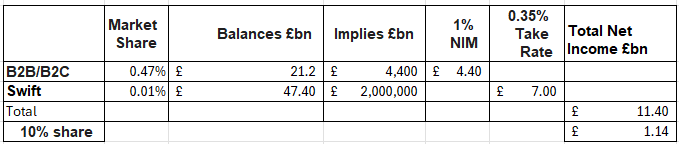

YoY growth of 31% is great, but the market penetration of B2B and B2C today is only 0.47%. Balances are £21bn today. Pro rated with 100% share that could be customer balances of £4.4tn. What’s the point of holding those?

Judging this on a “P/E ratio” misses the point. What point is that? I’m getting there.

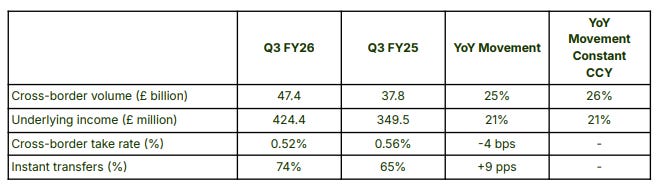

The “E” is getting swallowed in dropping the cross-border rate take rate the strategy being to achieve 0.35% eventually. Currently the rate averages 0.52%.

Some of that is the fact that the Wholesale rate is likely 0.1%-0.15%. There are far fewer costs associated with Wholesale since the customer handles compliance, and is simply a platform user.

With a 10% share of the market WISE would earn well in excess of £1bn net profit per year. That further assumes (as they do) that 1% NIM is the extent of the earnings capability of holding customer balances. Currently that NIM is closer to 3%.

What valuation does that attract? 20X? £22bn would be 150% upside to today. The question is how quickly can it get to 10%? (And can it get to 10%?)

Short Term:

The 1H26 result (to September 2025) delivered a 16.3% underlying PBT margin. £122m underlying PBT vs £749.5m income.

So the 3Q26 news that the full year would be close to 16% excluding one-off costs is encouraging to see.

Conclusion

Sacrificing profitability to deliver scale more rapidly is the strategy. The goal? Dominate so that you can capture a large part of the B2B and B2C FX payments space. But more than this to break in to the Wholesale market and capture a far larger prize, a multi quadrillion prize.

It’s like going hungry and pinning every fish you pull out the water, as bait to capture Moby Dick.

At even a whale, just a tenth of the size would value WISE at 2.5X today’s market cap.

And who can stop them?

Regards

The Oak Bloke.

Disclaimers:

This is not advice, make your own investment decisions.

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as “blue chip”

Wise has a great moat and is a world beating company. I hold 2000 shares for the long term. They have sacrificed short term profit for the future growth.

Excellent write up which focuses on nuances missed by most others. Thank you