Tapping in to the IPO-campus

High growth at high discounts

Dear reader

IP Group contains 67 holdings in CleanTech, DeepTech and HealthTech.

Today I’m going to cover forecast realisations and movements. Despite other VC trusts re-rating (notably GROW up 19% today), IP Group has remained at a stubborn discount.

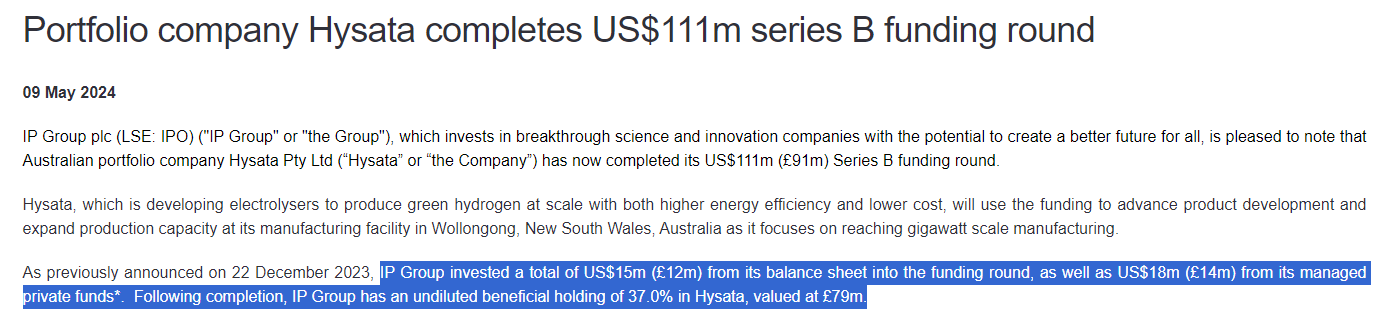

Hysata

Last month a series B round for Hysata meant a slight negative adjustment for IP Group, albeit at a slightly higher ownership level, and following a large uplift in 2023 (a rerate which of course was validated in May). £79m is 16.4% of today’s market price.

Of course Hysata is on a 3X MOIC (multiple of invested capital). Hysata are making astonishing progress in electrolysis. Electrolysers convert electricity into hydrogen. Hydrogen is a fuel which can be used for pretty much anything, steel making, flight, fuel cells and has some useful characteristics which can replace metallurgical coal, naptha and other fossil fuels.

Eagle-eyed readers will spot I covered Ceres recently (also developing electrolysers) is aiming for a 36KWh/kg with Shell. The difference there is that is achieved with 700 Celsius heat, whereas Hysata doesn’t (need to) use heat.

Trading Energy: Spain is a typical country which is investing in renewable energy generation. 19GW in 2022 and 76GW by 2030. And 28GW of wind.

What becomes apparent looking at Spain’s spot electricity is that there are times when power is almost free. While interconnectors and export via cable is one way to deal with that power, an electrolyser is another.

There are lots of countries where the success of renewables pioneered by countries like Spain (and the UK) can be replicated. South America, SE Asia, Africa and the Indian subcontinent are ripe opportunities.

Not forgetting the USA of course.

Specifically its Inflation Reduction Act expanded tax credits for renewable electricity and clean hydrogen. From 2023 can receive a production tax credit of 2.6 cents per kWh and up to $3 per kg of clean hydrogen, respectively, for the first 10 years of operation.

If you can produce renewable energy at say 3.5c per KG essentially the net cost is 0.9c after subsidy so $0.37 of renewable electricity makes 1Kg of Hydrogen where the competitive fossil fuel price is $1.50-$2.00/Kg.

Meanwhile growth projections according to Precedence are exciting too.

Growth is exciting and owning 37% of a company uniquely positioned could be quite exciting! Hysata has a current £213m valuation, and IPO own 37% of that.

But if we saw Hysata at a £0.5bn valuation on the basis of 2% market share of the $11.2bn FY27 market size then Hysata would have a £171m turnover and at a 15% margin, earnings of around £25m and using a PE of 20X gets me to £500m. 37% of that is £185m.

£79m to £185m without considering the 60% discount to NAV (£31.6m to £185m if you do - so a three year 5.85X upside from here)

Garrison

IP Group announced today that portfolio company Garrison Technology Ltd ("Garrison") has been acquired by US-based cybersecurity firm Everfox (formerly Forcepoint Federal).

The Group will receive cash consideration for its holding in Garrison. The transaction will not result in a significant change in the Group's Net Asset Value, reinforcing the Group's valuation approach. The transaction is subject to regulatory review and customary closing conditions and is expected to complete this summer.

That doesn’t sounds terribly exciting but a realisation at book when you can buy IP Group at a 60% discount to NAV is actually a 2.5X upside. The £31.6m cash is 6.5% of the market cap, and adding that to the estimated £265m current assets nearly 70% of the market cap is covered by cash and including ONT the number rises to over 80%. So the private listings less long term debt are at an astonishing 80.9% discount to NAV.

If you agree Hysata’s private valuation is fairly solid (since it was 1 month ago) then you get to a 95.5% discount to NAV

Private listings less long term debt are at an astonishing 80.9% discount to NAV, or including Hysata at book value you get to a 95.5% discount

But that’s not the whole picture either. Garrison has steadily grown by around 10% a year in valuation too since 2021.

The fact that IP group has maintained its discount in 2024 but there is a key reason that has held IP Group back.

Oxford Nanopore. ONT is down 60% in 12 months, and most of that in 2024. The value of IPO’s holding has reduced from £173.6m at 31/12/23 to £85.1m today.

While I’m not an expert in the area of genetic sequencing I’ve read other experts who do speak highly of ONT and its products. I’ve covered ONT’s Fy2023 update in this article fairly recently. ONT is now an £876m market cap, on P/Sales 5X and falling, for what could be a $150bn market in just a few years. If ONT can continue to expand revenue at 2/3 of its historic rate, and maintain R&D at current levels it will reach cash break even in 24 months and profitability in 36. There’s over £230m of cash cushion margin of safety to my numbers held by ONT if they don’t.

Progress seen in their London Calling customer day suggests they stand good odds.

ONT is actually now the 2nd largest LifeScience holding - behind Istesso, and Hinge Health isn’t far behind (and growing fast).

Istesso and 5 others all have potentially game-changing Phase2/3 results in 2024.

Conclusion

Today’s news might not be seen as terribly significant but it actually underlines the fact that an asset the market thinks should be discounted by 80.9% when IPO achieves a zero discount or a premium on realisations. This is yet another example where the IP Group stable holds valuable holdings worth far more than the market believes.

It’s true the estimated NAV has fallen by an estimated net 6.9p a share post period, due to ONT, but continues to offer exceptional value in my opinion.

Regards,

The Oak Bloke.

Disclaimers:

This is not advice

Micro cap and Nano cap holdings even those held in VC stocks might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".