BMN's Q4 update

Will 2024 be a better year for Bushveld?

Dear reader,

Here is your Q4 update. I jest.

You’d be doing well if you were a BMN shareholder and could afford an Audi Q4 right now. In my last article BMN-great I spoke about the positive news of the refinance, and that completed last week. Yet, an 11th hour problem with SPR funding its share purchase has set BMN back, plus disrupted the plant’s production due to lack of funds.

We are not told quite why BMN is sailing so close to the wind, but it adds some credence that my sums in BMN Great were within a few million dollars accurate (as pictured below). I calculated $15.7m net cash (assuming the $12.5m from SPR had actually come in - which it hasn’t…. yet) so my $10m FCF estimate is about $5.2m too high - because the $2m interest free loan was (I think) the amount of money Craig rang SPR and said if you don’t get $2m to us pronto, your Mokopane purchase and 50% of Vanchem is toast, my man. ($15.7m-$12.5m SPR -$5.2m FCF inaccuracy = $2m shortfall).

Considering FCF in H1 was -$2.7m and considering too the falling price for vanadium in 2H2023 and now in Q1 2024, I was being optimistic estimating $10m FCF. Also problems such as the tailings dam and other challenges also affected production and involved unforeseen costs. Without these challenges, and price falls $10m FCF would have been beaten, I believe.

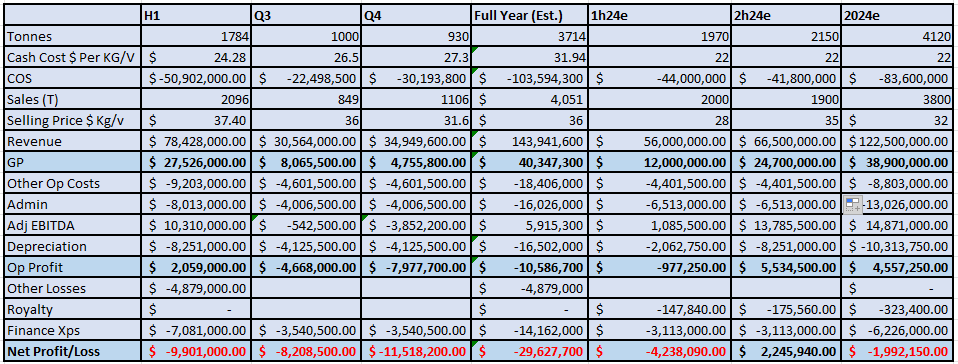

So here is my estimate for the 2023 full year. The brain boxes at Hannam decided not to issue a profit model today, and BNP Paribas have ceased coverage so it’s left to the Oak Bloke to have a crack.

The H1 numbers are nailed on and I’ve taken the actual cash costs, sales, average selling prices, and assumed a steady state for everything else. We know Craig has cut admin costs at the end of 2023, so reducing admin by $1.5m in 2024.

The estimated $29m loss isn’t great but did anyone expect anything much better than this?

Clearly someone did (and was disappointed enough to sell today)

Do you love the smell of opportunity in the morning?

As I said in my Why I didn’t pick ‘em article. I see BMN as a 2025 Oak Bloke Top 20 candidate. 2024 is a year to retrench.

The refinance is complete as I predicted in Value Trap or Up You Snap (except for the $12.5m SPR share purchase which is a few weeks away), and the vanadium price is at a crazy low price today. Yet the world economic outlook is far brighter. China is reflating, and it’s put Evergrande to the sword so working through its construction problem, meanwhile India is growing great guns, the US is growing great guns. Cathy Wood pointed out last Friday that worker productivity is growing at 3.2% per year - all of this is positive for Vanadium demand.

Vanadium as a power storage continues to grow too. Hebei announcing a GWH size vanadium battery a few days ago. The Chinese installed a vast amount of solar power in 2023 (216GW) - that’s about 13X the TOTAL current total solar power in the UK! Just in 1 year! Storage of that power also will need to grow. In 2022 it doubled to 59.4GWH and is forecast to grow by 18.9% CAGR for the next decade.

Each MWH translates to something between 3.3-10 tonnes of vanadium per MWH.

Invinity with 500% yoy growth and a 6000MWH pipeline, and to put that in perspective in 2023 it deployed 28MWH.

6,000MWH is 20kt-60kt of Vanadium demand! That’s somewhere between 6 and 16 years of Bushveld Minerals production!

By 2031 VRFB’s alone might require over 5x that amount!

About IES (a VRFB supplier)

IES, at a £47m market cap (down from around £100m market cap last year) is worth 2X Bushveld’s Market Cap.

Meanwhile, Bushveld owns part of a company like IES. Around the same size as IES. With a “Mistral” program like IES that will halve the cost of a VRFB. But BMN is looking to sell its 29% Cellcube holding. Cellcube is the hidden creature under the Bushveld stairs, sadly unloved by Craig Coltman who sees focus focus focus as the way forward. As I wrote about in my article 5 more drivers to value it is roughly comparable to IES and even at the current bombed-out price of £47m, BMN’s holding is approximately worth £15m, so 60% of Bushveld’s market cap in other words!!!

Arguably to the right buyer Cellcube could be worth at least double that (just as IES was last year). So theoretically if you buy Bushveld you could be getting 20% cashback and the rest of BMN for free. In fact the current low Vanadium price is bad news for BMN but is a boon for the likes of IES and Cellcube. The cost of the electrolyte is a large part of its costs. The Inflation Reduction Act is incredibly positive for Vanadium Flow Batteries too.

IRA tax credits for VRFBs:

a) Standalone storage investment tax credit: The industry has availed the ITC benefit on solar-paired projects in the past few years, but this is the first time that standalone energy storage is eligible for an ITC. While there are several tiers for the ITC value, it is generally accepted that most projects will at least qualify for a 30% tax credit

b) Advanced manufacturing tax credit 45X (!): The IRA introduced a manufacturing tax credit for various clean energy technologies, including battery cells and modules

If only someone could sell them electrolyte…..

What, someone like Bushveld energy?! That’s another part of BMN’s assets also not in the price. In today’s update, 3 battery companies are happy with the vanadium electrolyte. Outside of China, Bushveld are one of the only options to supply electrolyte. That’s incredibly bullish, or should’ve been…. but that baby flew out in today’s bathwater.

BMN’s 45% share of Belco has been achieved through a $10m investment (Meaning Belco is worth $22m overall?) again nowhere is this value of the asset in the share price.

Nor have I accounted for the revenue 8m litres of electrolyte this plant could produce in 2024 but there’s an upside here once supply contracts commence. These are in discussion, we learn today. Nice. If the $22m plant can generate a $3m-$4m profit that’s worth $2m to BMN, and if they sold their 45% holding at a 8X-10X valuation, a gain on disposal of $10m-$20m isn’t impossible… that’s another 50% of BMN’s market cap.

For the want of 180 tonnes the battle was lost…..

Today’s price crash appeared to be on the news that January production was affected by the SPR shenanigans. 267 tonnes produced in January is around 90 tonnes below the bottom of the 20024 target so 75% of the minimum. It’s fairly safe to assume February will be similarly affected. But that’s 180 tonnes on a 4300-4500 target. So let’s take it on the chin, drop the target to 4120 tonnes for 2024. I’m not sure why the clever analysts can’t just recalculate around that, but there we go. Noticeable that BMN is not picked on by a popular share shorting site today. I would have expected them to gleefully announce something - is that a bullish signal too?!

The OB 2024 forecast.

As I just said I’ve assumed 180 tonnes affected in the first half of 2024 and gone with the lower target production as my forecast. I’m working on the basis that sales of 2,000 tonnes at a lower $28/kg fev in 1H. Today (5th Feb) it’s at around $29/kilo even in the USA and appears to still be falling. This price for Vanadium is crazy by any measure - well below the production cost of any primary supplier. For the secondary suppliers tied to steel Fitch tell us that demand for steel is due to increase 20-30MT in 2024 compared to 2023. That’s positive for Vanadium prices.

So I’m forecasting a bounce back or normalisation to a $35 average price later this year which seems reasonable. So a $32 average price in 2024 based on sales of 3,900 tonnes of Vanadium.

I’ve calculated royalties at 0.264% (and was surprised how negligible this is - at least for now); finance is based on an estimated $28.3m at 11% interest. I’m assuming flat depreciation, and am assuming the 50% sale of Vanchem (40% of production) and the 36% acquisition of Vametco (60% of production) more or less cancel each other out. Ideally I’d split these out but my brain is tired.

Admin falls by $1.5m per annum per the 40% head count cut in December 23, and the Vametco Minigrid I estimate to save $0.4m (10% of power) per annum, so reduces Other Op Costs.

I’m not considering the enriched ore due to become a highly enriched feed for the Vanchem plant from SPR. I’m assuming we don’t see this until 2025 - but I might be too pessimistic about that!

The conclusion I’d draw is that BMN stabilises in 2024, with a small loss (which could easily be a small profit through the various upsides I’ve discussed), but cash generative, and ready for 2025 when it will be well positioned for a vanadium upswing.

Patience in 2024 is required, and buying in at a bargain price (as set out in BMN-eck! the assets, the ore deal with SPR, the 36% Vametco) ahead of the rush could be very rewarding. Most, but not all, of the risks are overcome. Buying at 1.3p a share is a much safer bet today than when it was this price in Q4 2023 - before the refinance had been agreed. H&P forecast a target price of 6p (320% upside) using an undisclosed DCF analysis and BNP Paribas previously thought 3.8p-4.8p.

This is not advice

Oak