DGI DGI DGI 9

Digging into DGI9 - one of the Oak Bloke Top 20

Verne

The sale is still ongoing and volcanic eruption remains a theoretical risk. However the eruption has turned back south away from Verne. My thoughts go out to the people of Grindavik which is being evacuated as I write, 1 casualty where the earth quite literally swallowed him up.

Having covered Arqiva in detail previously here’s the remainder of the portfolio and what they do.

Aqua Comms

Provides 3 x 20Tbps bandwidth of data connections between Ireland/UK/France and the USA. Two connections are active a third went live during Q32023. This third connection was a collaboration with Vodafone, Microsoft and Meta and the cable itself comprises 16 fiber pairs and 400 Tbps, Amitié is the highest capacity transoceanic communications cable ever deployed.

EMIC-1, also operated and managed by Aqua Comms, connects the key European hubs of Barcelona, Marseille and Genoa with Salalah, Oman and Mumbai, India, bringing a new, high capacity cable system to underserved markets experiencing exponential growth. It is slated for a Q2 2025 completion.

SeaEdge

This is a data centre asset and subsea fibre landing station, located on the UK’s largest purpose-built data centre campus in Newcastle. It is the UK’s only landing station for the North Sea Connect subsea cable. The asset is leased on fully repairing and insuring terms to the tenant and operator, Stellium Data Centres Limited, via a 25-year occupational lease with over 23 years remaining. Stellium continues to meet its payment obligations under the lease, delivering on the Company’s target yield at acquisition.

Elio

Elio Networks continued its growth in wireless connectivity operations in 2023, with unique customer connections of c.2,800 by June 2023. The Company has a diverse client base including larger multinationals, government bodies, global technology companies, small professional service firms, retail and hospitality companies. It focused early on addressing the growing requirement for affordable high-speed broadband in the greater Dublin area, and is now the largest wireless Internet Service Provider (“ISP”) in the greater Dublin region. As part of its 5-year business plan, Elio Networks has identified a growth capital expenditure pipeline of c.€8 million (c.£7 million) for the period to 2027, including €1.3 million (£1.1 million) in 2023.

Forecasts

Working from the basis that Verne is disposed (see my analysis of that here), and noting the “strategic review” I have created some initial forecasts. These are a “best guess” but help paint a picture to what is an investment trust which has been presented in a complicated manner (in my opinion).

This is my best guess of once you strip away all the complicated structures what the net position looks like as we begin 2024. Investments comprise the 5 holdings ex-Verne, debtors is largely Verne (the earn in), cash is the mid year balance plus Verne.

On the sources of finance, the RCF has reduced by £300m due to Verne. The VLN has grown due to interest accruing, equity is taken from the interim so a balancing figure is the retained loss (or put another way shareholder funds are £747.50m)

The big problem we see is the remaining debt. The VLN must be settled before any distributions from Arqiva can be made.

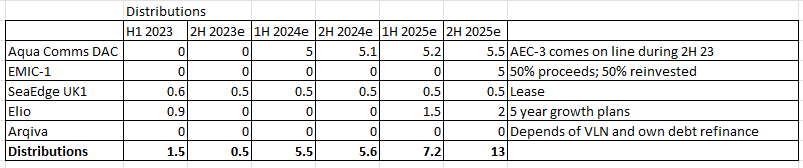

EBITDA should grow in 2024 and 2025. I’ve assumed EMIC provides the promised “exponential growth to an underserved market”, while Aqua provides a mild improvement (which may be conservative). Elio continues to grow as it reaches out over other Irish cities, and Arqiva grows through its metering and broadcasting units.

Distributions (dividends paid to D9) improve but only slowly…. if Arqiva cannot make distributions. Notice I’m assuming Elio is cash hungry as it grows and EMIC-1 makes no distribution until 2H 25. Aqua begins distributions in 2024.

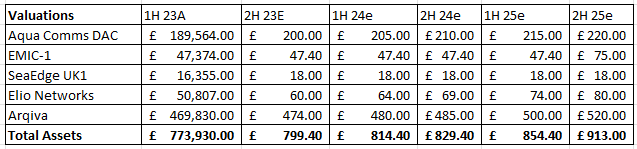

Valuations improve, particularly for Elio and EMIC-1 (once operational).

What to do? The Strategic Choice facing DGI9

It slightly baffles me that these Strategic Reviews take so long. The choices appear obvious. Of course the answer is in the execution. But this might be what DGI9 are thinking.

Sell other holding(s). There’s a large disparity between the return of different holdings. This is partly due to leverage. The EV/EBITDA of Arqiva is around 13-16. Also some holdings may appreciate in value as well as generate returns.

However Seaedge UK1 seems an obvious candidate to go. Partly because its economics are less attractive but also there is no growth potential that I can see. It’s a building lease and that’s it.

But a 2nd candidate must be Aqua Comms. If a value north of £180m can be obtained then that completely clears the VLN and some more of the RCF. Gross cash looks like it could cover the RCF value too, but these are very rough numbers so it would be good to have some cash head room. If it were bundled with EMIC-1 (since Aqua Comms manage and operate this) a sale for the pair might fetch north of £300m. Remember data use is growing exponentially so these assets are hot property and remember too its co-funders are Microsoft, Meta and Vodafone. Perhaps Vodafone is a little debt laden (although I owned C&W who Vodafone bought if I remember rightly), but if not them would the other two be interested in using a little of their mountains of cash to own more of this strategic asset?

It may sound a bit crazy but an IPO of Aqua Comms might also be an option?

Refinance is another approach. It is not inconceivable that long term finance could be obtained at increasingly competitive rates. Kicking the can down the road provides optionality.

A rights issue another. But at today’s market cap I can’t see this to be an option.

Conclusion

A focus in on growing Elio, Arqiva and possibly EMIC-1 seem the best prospects for DGI9. Disposing of the rest. If a combined £300m sale is possible, then this leaves DGI9 with shareholder equity of some £850m, debt free with firepower (excluding any new debt) of some £150m. Remember too, this is only a £245m market cap. That cash if returned to shareholders would be a 60% special dividend at today’s prices.

Or put another way, let’s say the 3 are sold for half that - a cut price £150m. Even then DGI9 is debt free (with no cash but £127m of short term debtors). (No 60% though, sorry). But crucially, with Arqiva able to make distributions as I showed in deep dive into Arqiva a £50m or more distribution would be eminently possible. If paid out in dividends this is upwards of a gross 20% yield for shareholders.

Is DGI9 mispriced? Do the maths.

This is not advice. Just musings.

Oak

Aqua Comms is likely next to be sold. Expect an announcement in the not too distant future

So looking back to this article, you were suggesting that they could get possibly £180m from a sale of Aqua Comms. It's hard to understand how they ended up with just about £40m. I think the most likely reason is that the management received a kickback/bribe from the buyers to give them a cheap price. Or the valuers in 2023 were extremely negligent -these are supposed to be growing business rather than declining businesses, so the valuation should have been moving up. There could even be a case for damages against the valuers.

https://www.hl.co.uk/feeds/apps/rns?id=34820854