RTW - Buy-o-tech?

RTW - Buy-o-tech?

What does the post Arix world look like?

Dear reader,

Arix was an IC bargain share of the year. 2022 vintage possibly. It turned out to be a sleepy affair where a mountain of cash sat idle while and for a long time after biotech went through a dramatic downturn. Now, I am no biotech shares specialist but that’s why you pay 1.5% to Arix for their expertise. Surely, I thought, they will deploy that capital. Or buy back Arix shares at what was at one point a 60% discount. But no, the cash slept and I cannot speak for the investment manager.

Fast forward and after watching a tense Arix presentation the news came Arix had sold themselves - I was intrigued. Its buyer, RTW Biotech, could not be accused of sleepiness. Double espresso macchiato New York Sass, RTW is an active beast. Goody, I thought, all that Arix cash will be put to work. I covered the story in IPOs for IPO where I discussed how it was acquiring Arix and how there was a value disconnect. Well, reader, I look full advantage of that fact (and perhaps you did too), that you were getting 1.4633 RTW shares for each Arix share - even better terms than the #1 shareholder Acacia who did a deal to get cash. RTW shares worked out 10% more lucrative and the discount to RTW seemed to guarantee a profit.

Now sitting on said tidy profit, what should I do next?

As I contemplated this what caught my eye that the NAV/share had grown again. From $1.90 to $1.93 as it marches upwards. (Up from $1.68/share last June)

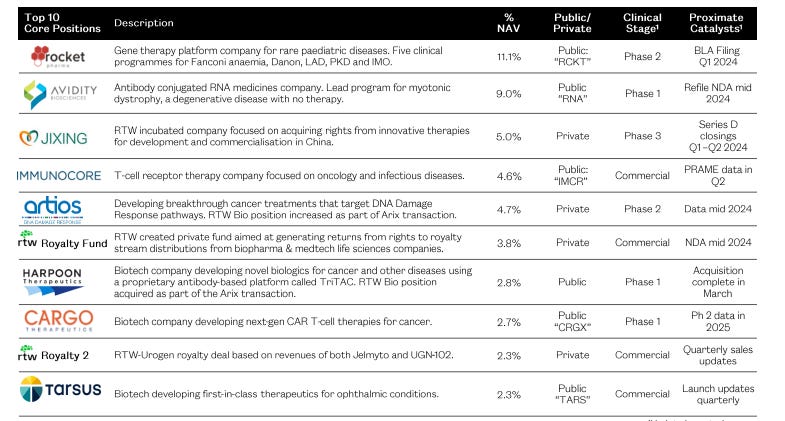

What, next, caught my eye were the “Proximate Catalysts”. Now I know Arix had these also and in fact Harpoon and Artios are from the Arix stable. Six out of 10 with a 2024 event.

Next, I started to research their public holdings.

While with private holdings they aren’t regularly marked to market, each publicly listed holding is daily and has analyst target prices too.

This chart shows the publicly listed, with valuation as at 30/06/23, the NAV % at that date, then the 30/06/22 value and percent. Next I applied today’s market price in “Valuation at 22/3/24”. Next I cross referenced the newsletter from 29/02/24. Hmph. The numbers were wildly different. I realised there have been further purchases post June 2023, and so I settled on using the 29/02/24 number.

I then compared the current (22/3/24) price and consensus target price. The final column is the value at the consensus target price.

I was astounded. $194m of upside. That’s 40% of RTW’s $500 market cap. Now of course, reader, these are target prices but I found on each one was a “STRONG BUY”. Nothing other than “STRONG BUY”.

I haven’t sought (yet) to analyse the basis for their recommendation, or whether RTW invested in holdings which became strong buys or just bought existing strong buys, but it does suggest that there is upside to the holdings from their current price and the current RTW 32.4% discount to NAV appears unwarranted, or at least doesn’t appear to be easily justifiable.

Returning to the earlier columns we see many uplifts 2022→2023 as well as 2023→22/3/24. For example Rocket has err, rocketed from $32m to $59.6m (or $73m). In fact apart from GH Research which is is at 1X two years later and Cincor at 0.16X the remainder have double bagged in aggregate. 8 out of 10 of the publicly listed are double baggers over 21 months

8 out of 10 are double baggers over 21 months

How is it this investment trust isn’t more well known? I guess 1.9% ongoing charges might put some off. 20% performance fee above 8% others. For me, if they can perform I can live with that.

Buy Backs

With 12.6% of NAV as cash RTW are not messing around. In the space of 5 weeks they have already bought back about 1% of its own shares. This has uplifted the NAV by over 1c/share already.

In fact if we stripped out cash we arrive at a deeper 36% discount, and if we stripped out publicly listed and cash the remaining private and royalties portfolio is on an 85% discount.

In fact if you could sell the royalties at their NAV value too, then you’d effectively pay $506m to get $533m cash back plus hold $124m of private Biotechs.

… and that’s ignoring the target price of those publicly listed holdings of course. The maths grows to $506m for $727m cash back and $124m of private Biotechs.

Maturity

It is also notable where Phase 2, 3 and Commercial make up 71% of the NAV.

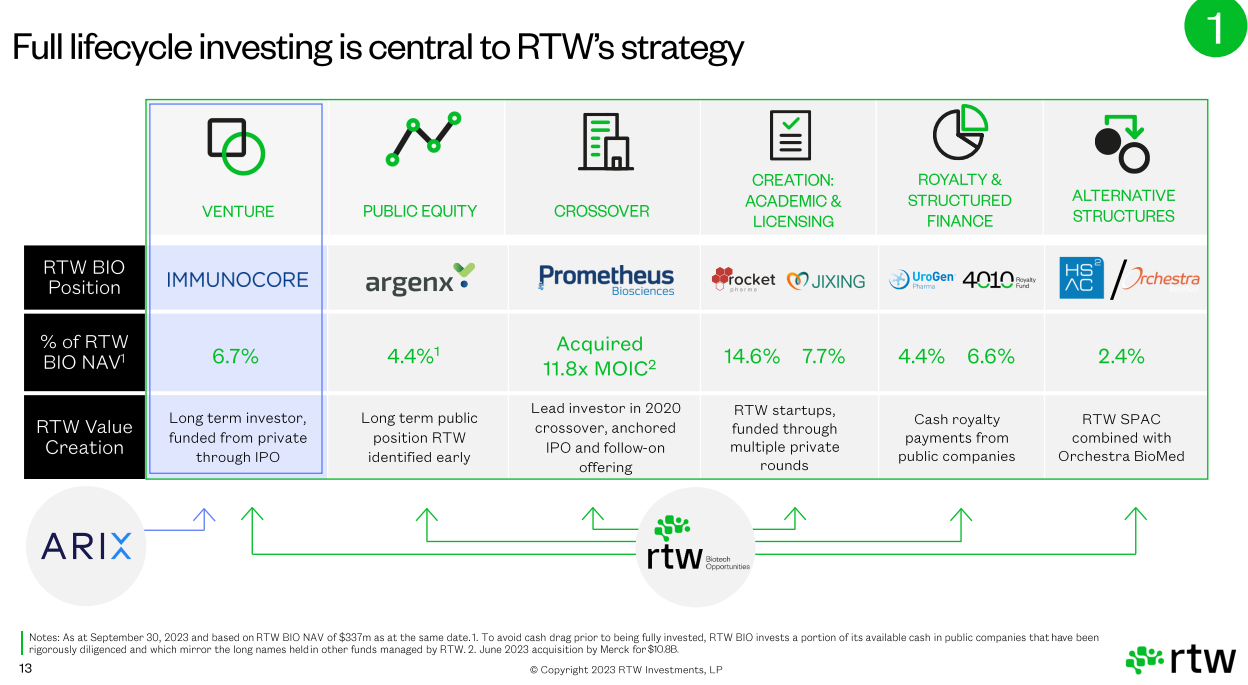

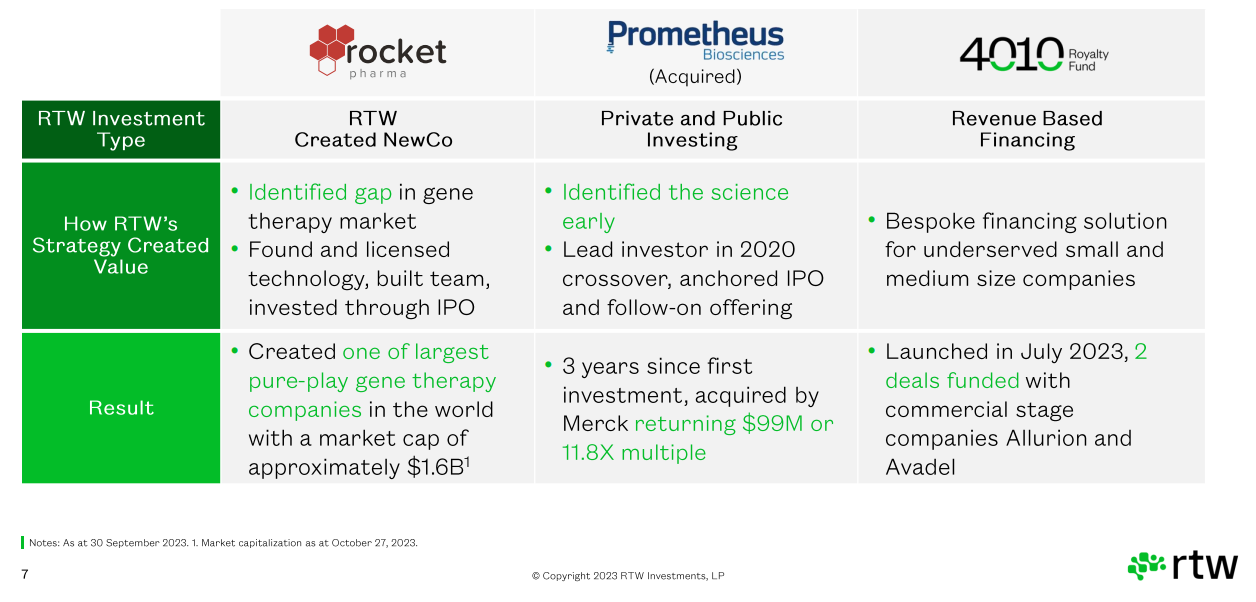

But it’s worth also pointing out that RTW see “full lifecycle” as a crucial value add - so it’s not just about buying and flipping - it’s about capturing multiple inflection points, potentially, if the science bears it out.

Listening to this interview this was the key point I took - that RTW obsessively understand the science very deeply. But understanding that, they can often succeed.

For example in these case studies creating value began with IDENTIFYING. There are 13 PHDs working for RTW.

So to conclude, while I cannot say that I’ve done any kind of deep analysis on biotechs and nor can I say that I deeply understand the intricate world of biotech science, the accounting numbers tell a story. The macro drivers of big pharma needing new blood, of faster/cheaper discovery, of breakthroughs in disease. A portfolio with many near term catalysts and newsflow. Healthcare is a defensive sector, once you have successfully completed the phases and have something to commercialise. While a 32% discount on a share where the average discount over 3 years is 7%, and where there are multiple shots at goal. Where there’s a clutch of multi baggers, and where even after this these publicly listed holdings are STRONG BUY with more multi bag upsides. There’s lots to like about RTW.

This is not advice

Oak