La Mano De Oro

Translation: Golden Hand (the hand that connects GoldFinger Part 1&2)

Dear reader

The price of Gold.

Goldman reckon it could go to $2,700 in 2024 and with a name like that who’d disagree.

Meanwhile the price of miners has increased. Does value remain within precious metals? I think the answer is yes, and this article is to begin to surface some ideas where. Of course part of the equation is your continued believe in the price of gold. It is my approach to believe in simple things. The three things I put to you which I believe are driving the price of gold are trust, religion and strange bedfellows.

TRUST

The Chinese (and there are many of them) have been fundamentally left up the creek without a paddle on property. Culturally they relied on property, invested in property, and now that trust in property is deeply broken. Chinese cannot move their money abroad (legally) due to capital controls. Gold is the natural successor to this people’s prolific desire to save and build assets. Swiss exports is a strong indicator that the Chinese are massively buying gold. Much of the gold they buy is Swiss produced.

RELIGION

The Indians (and there are many of them) grow wealthier and gold is intrinsically linked with Hinduism.

The strange bedfellows: Crypto and the West’s betrayal

Readers will know my scepticism and fairly intense dislike for Crypto and the simple cliff face it faces in the future that what keeps the metaphorical lights on when the incentive to produce crypto is exhausted? Miners doing their crypto mining delivers the ongoing and vast electrical cost and infrastructure cost of maintaining the distributed ledgers and transaction capability. The “halving” as a means to cost push the price higher which is counter to basic economic theory and the supply curve.

But there is a growing number of people who see Gold and Crypto as being linked or interchangeable - like Scaramucci (will you do the Fandango) below. The only “get out” I can see for Crypto when they run out of greater fools would be for governments to adopt Crypto and therefore pay for or provide the infrastructure - as they do for other things. The UK pays around £150m to provide notes and coins.

Some would say governments are always the greatest fool. But this would essentially be a return to the Gold Standard, and an end to the funny money/QE/debasing/money printing etc. The problem is which government will be the Turkey which will vote for Christmas? The only scenario I see is the one that wins power following a future crisis due to debasement. A Liz Truss on steroids moment. People like the cheerful Nouriel Roubini aka Dr Doom have predicted this doom every year for numerous years.

It is my belief that Gold wins now with debasing (store of value), but also wins in a gold standard scenario (means of exchange). It wins if it gains a strange bedfellow in crypto (means of exchange). It wins if Dr Doom is right (uncorrelated asset). Win-win-win-win.

It is noticeable how gold and bitcoin have become more closely correlated (although the Chinese can’t touch bitcoin - legally) so we do see some divergence in 2024 - due to trust, of course. But also central bank buying including China and also as a counter to the Western World’s treatment of Russia and Belarus. Regardless of the morality, the expropriation of Russian assets by the West is a betrayal of the global monetary system. Gold is a huge benefactor to that betrayal.

So there are strange bedfellows in the “anti West”, who make up much of the world and who want to de-dollarise. Gold is the best and easiest way to do this because none have currencies that could realistically replace the dollar.

Moving on to Gold Miners

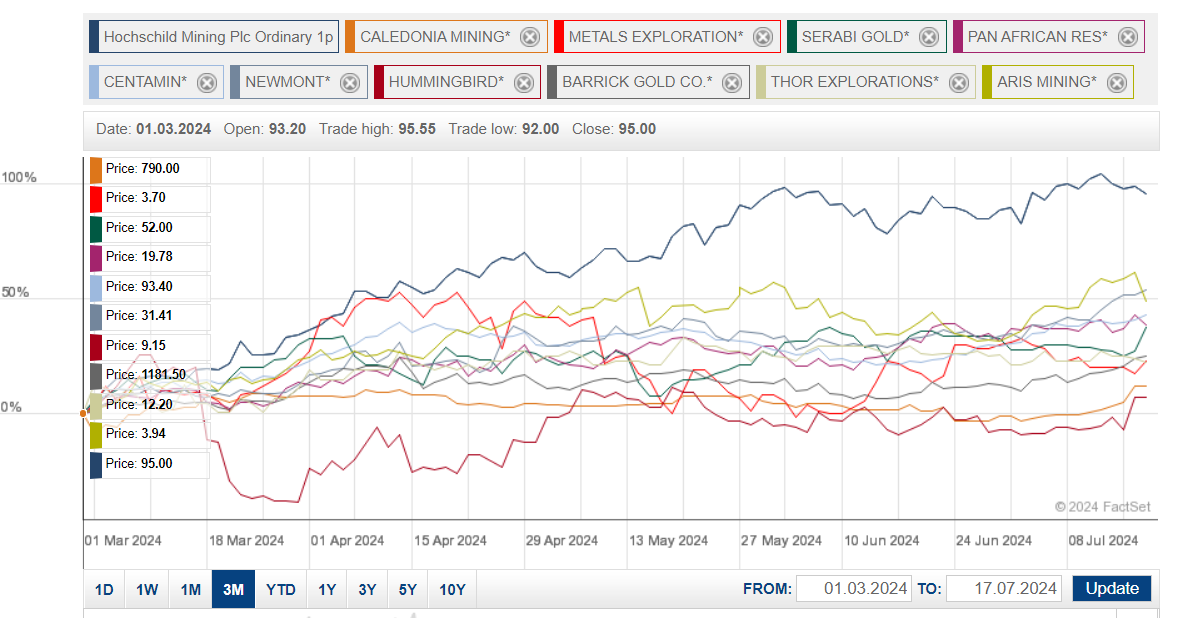

Eagle eyed readers will know I spoke about Gold Finger Part 1 and Part 2 back in March. In those articles I spoke about the positive prospects for gold, and some ways to play those. Those and other gold trades have worked well for me; but now at close to $2,500 is there more to come?

Let’s find out what happened to some of these:

If you followed my articles I liked HOC (e.g. HOC-key 19th Feb) and that has stood out at a clear winner - today it’s nearly a double bag. More on that later.

I didn’t like HUM and 4 months on it’s a ho-hum 7% gain, and I believe a work stoppage disagreement over a few months, which has now ended.

Only marginally better is Caledonia (CMCL) which I like - but as part of Baker Steel (BSRT) - and which is up over 30% YTD. Although CMCL itself has done less well and actually hit 760p a fortnight ago. I considered that far too cheap so I added CMCL directly and it’s up 15% since.

Thor/MTL/Barrick up a respectable 20%, while Serabi/PAF/Centamin are up 30%-40% (there was some debate whether CEY or PAF was better - but so far since March CEY pips it by a tiny bit - sorry PAF-fers).

Finally Newmont and Aris are around 50% up.

It is going to be hard to condense this into a single article so don’t be surprised if there’s a Golden Hand Part Two, or perhaps I’ll deep dive into individual stocks. Just think of the title possibilities, reader:

Is PAF naff or an upwards graff? Is Hum a hum-dinger or a share-slinger? should you say CEY-you later to Centamin? Dad joke titles galore. Bet you can’t wait.

Plus readers make many useful suggestions:

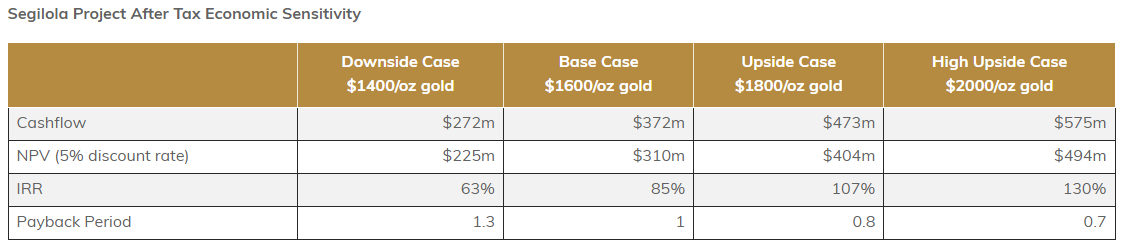

Things like they really like Thor (Ticker AIM: THX). Down 25% over 1 year but some nice metrics around it like a P/E of 3.3, debt of $7.9m but it repaid $7.9m debt in 1Q25 (ending 30/06/24) so should be debt free in the next few months. It produced 21.7Koz in 1Q24, and aims to produce 100Koz in FY2025 (year ending 31/3/25). Its mining operation is in Nigeria which appears very mining friendly, and the management has delivered on its promises over a timescale.

Let’s say it achieves just 88Koz at $2400 (upside potential to both) then revenue of $162m, an AISC of circa $1100, means an EBITDA of around $65m, and net profit of $35m or more, so £28m or more on a market cap of £96m.

Its drilling program at new project Douta gives a future lifeline after the current mine is exhausted in 2028, although deeper resources at Segilola also exist. Just follow the yellow dotted lines downwards.

I think I really like Thor too.

PAF

Pan AfricanResources (Ticker PAF) also looks very cheap, even with its doubling in price over the last year to 25.1p. Its P/E of 5.5 for FY2024 (ending June 2024) looks cheap.

But what about FY25? By my reckoning and based on a 215Koz-225Koz production guidance at a $2,450 gold price and $1325-$1350 AISC then we are looking at an EBIT growing to $236.5m (Growing from $102.4m in 2023 and $159.4m in 2024 - estimated). Taking tax and similar finance/royalty/other expenses then you easily get to a $150m net profit (£115m). So the P/E drops to 4.5 (Edison speak to a P/E of 5.3 but don’t say how they get to that. It’s likely their higher P/E is based on a lower gold price, in fact calculating forecast revenue of just $420.8m in FY25 by 215Koz is $1950 per ounce. Either Edison know something about a forthcoming crash in the price of gold or their numbers are about 12 months out of date (to be fair they do say conservative - but I just find using obsolete numbers a bit irritating).

CEY

This week Centamin released the DFS for its Cote D’Ivoire Project.

Stunning metrics of $1,047/oz AISC over 10 years with $971/oz for the first five. A 167Koz per annum mine wth 207Koz for the first 5 years.

A 34% IRR based on $1900/oz gold, but this exceed 60% IRR at current gold prices. Or higher still given the fact there are inferred resources outside and within the current pit shells, extensions to mineralisation, but also capital and opex cost savings too, through process optimisation.

A $373m construction cost with 27 months to first gold.

An NPV above $800m at current gold prices.

Next step is to get the mining licence approval in 2H24.

-

Meanwhile CEY’s Sukari mine has FY2024 (Dec 24) of 470Koz at up to $1350 AISC. So EBIT should move from $262m (in 2023) to $484m for 2024. That equates to a net profit of around $410m. Deducting the SGM (Egyptian Government ownership) this leaves CEY with around $180m-$200m forecast net profit, up over 100% YoY.

MTL

Another BSRT holding is Metals Exploration who meanwhile have been busy bees. Settling their creditor dispute, buying out their JV partner at Runruno, now debt free and no longer subject to operational restrictions imposed by finance agreements.

It is forecast by H&P to earn $172.9m this year and a GP of $57.3m but its 6 month results out today put it at $91m revenue and $64m gross profit…. in other words it’s hit its forecast profit is less than half the time!

Costs are below target, the AISC is $1,066 in 2024, while average price per oz is $2,190 ($2,320 in Q2). Net profit should be around or just above $80m.

$80m is a P/E of 1.6.

H&P say the target price is 6.37p based on an NPV of $139.5m.

But hold on reader.

The numbers produced by H&P and indeed my numbers don’t take account for the minority share of 18.6% they just bought out. 18.6/81.4 is a 22.8% increase.

Forecast net profit grows 22.8% to $98.3m in FY2024 and that’s based on a $2,200 average price. Or at today’s $2,400 an Oz that’s a further $5.7m after tax.

$104m net profit potentially in FY2024 does not equate to an NPV of $139.5m used in H&P’s 6.37p target price. Runruno has 4 years production left. The purchase of the new mine project Abra 200Km north will be finalising next month.

6.37p is too pessimistic imo. A valuation closer to 10p is more realistic.

For BSRT-ties that means a £6m increase to the NAV of Baker Steel who own 5.4% of MTL. That’s equal to 10% of BSRT’s market cap.

Other Miners

Condor (ticker CNR) is an idea from a reader.

Its “La India” asset is up for sale, and valued (on the balance sheet) at £42.4m, CNR’s market cap meanwhile is £48m. Jim Mellon (of Agronomics) holds 26.12%.

La India is fully permitted, has a DFS, has a 2.33moz JORC resource. The project has compelling economics with an IRR of 61%

Around 0.6Moz is in an open pit, the site is cleared. It needs an 18 month build and is shovel ready and “good to go”. In a recent interview the CEO says there are three potential buyers. But in their presentation deck meanwhile speaks to 5 offers and 8 companies under NDA. So let’s say 3-13 potential suitors.

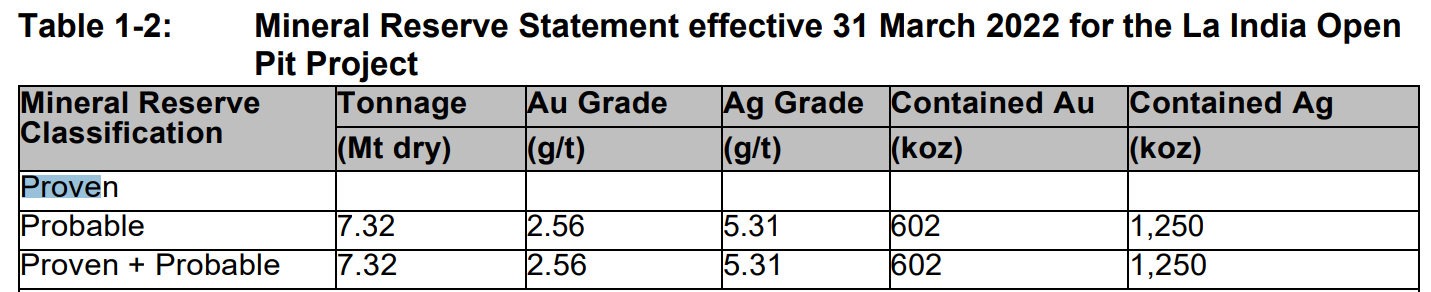

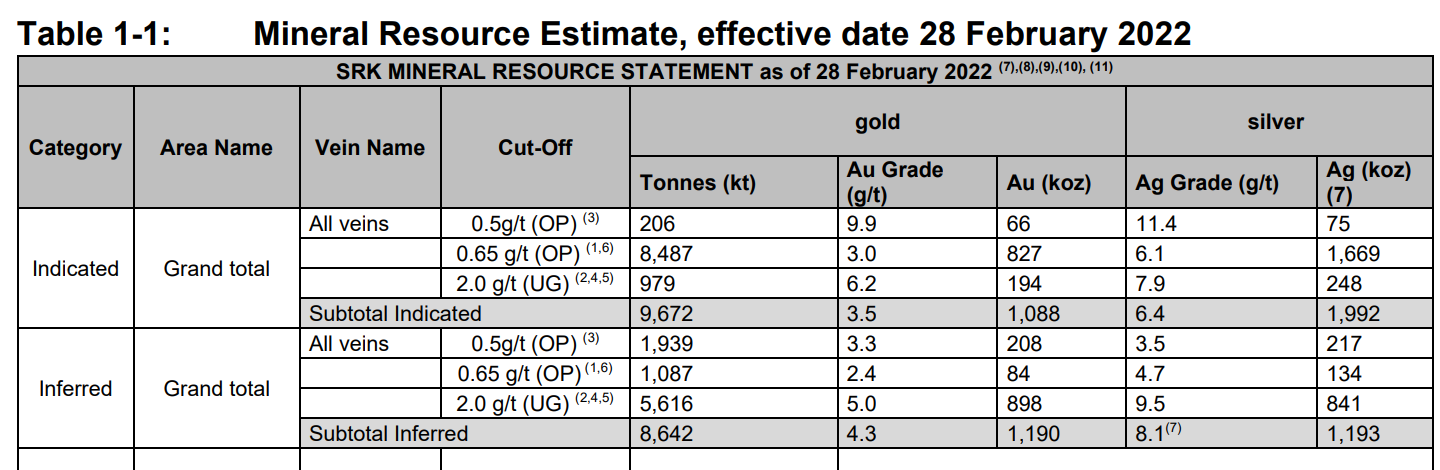

The best way I can think of to evaluate this asset is to compare it with another asset in Latin America which was sold. The asset is Mara Rosa in Brazil. HOC bought it for £85m back in 2021 when gold prices were $1,800 and this was a 0.9Moz Proved and Probable with 1.7Moz inferred. At 1.66g/t and 1.72g/t grades. A $200m capex.

La India meanwhile is 1.2Moz P&P (at 0.6g/t cut off) and 1.2Moz inferred (and 2 Moz indicated). At noticeably higher grades, of 2.56g/t and 8.1g/t and with some marginal silver credits too.

So it’s quite hard to think how La India could sell for less than £85m (double today’s market cap), and quite easy to think how it could be valued higher - due to higher gold prices, producers three years later with CASH IN THEIR POCKETS, and the better economics of a higher grade. The 0.6Moz open pit proportion is highly attractive too. Yes Nicaragua is less attractive than Brazil yet gold is a major export for Nica and there are numerous other companies operating there without issue.

In fact did you know reader, Nicaragua is a rapidly growing tourist destination? 142% up in 2024. It’s on the OB bucket list for sure. In a little side step to talking gold for a minute here’s a top 7:

In fact who better to buy the Condor asset than Hochschild? They pride themselves in being the leading Latin American gold producer. Their Y/E 2023 accounts show they had $300m headroom, their cash generation for H1 will be well in excess of $100m so an estimate of $400m headroom. They could - if they wished - buy La India.

KEFI

Kefi is another idea from a reader. Either spectacular value or something isn't right. Looking at the numbers it is a pre-revenue miner with some interesting projects in Saudi and Ethiopia.

I may do a deeper dive on this but from what I read I didn’t like it.

KODAL

Kodal Minerals has 2 gold mines which I suspect are now more valuable than its lithium prospects, which is all it seems to care about. This could be an interesting opportunity, it's on my list.

TRR

Royalty Companies with gold are on my radar too. Of course the Oak Bloke idea Trident features but with a 49p bid and a vote this week that probably is going to be approved, to the chagrin of many, I’m not going to spend more time discussing this today.

POW

This article wouldn’t be complete without considering POW. Its holding FCM went shooting (back) up yesterday by 35%, but still is great value as discussed in my article Premium Prices. But POW has numerous other gold holdings which when you consider how much further the projects have progressed in the past few years.

POW vs Gold - 3 year view:

Conclusion

There is still deep value to be found in gold miners in my opinion.

Many investors are reading broker notes which appear to have hopelessly inaccurate numbers because the current $2400 gold price isn’t being used (or the brokers are not re-issuing notes).

I get the “be conservative” argument but as an investor you also need to make informed choices. Are investors being informed? Eventually, yes, because results will surprise to the upside.

While HOC has double bagged and others 50% that’s not to say these are fully valued. If I’m right on HOC being $400m Adj EBITDA in 2024 and a net profit of something like £170m and using today’s £940m market cap puts HOC on a 5.5 P/E. Or put another way, each year each £1 invested in HOC generates 18.2p of earnings - to pay you dividends or pay down debt, or expand the business. If that level of earnings can be maintained into the future, a future dividend of 5%-10% appears entirely reasonable.

My preference is around producers rather than explorers so I’ve mainly covered those in this article. But POW is a huge exception to that. And Condor as an idea is intriguing too. Not forgetting Panthera (PAT) who I covered yesterday too.

The final thought I’d share is what if you were reading (or re-reading) this article some time in the future and the price of gold is not $2,400 but higher? Maybe $2,700 like Goldman think? The way mining works is it is a leveraged bet so higher prices mean much higher profits. (And lower prices much lower profits). To avoid the criticism that I’m “always too optimistic” my gold-related articles this year have featured gold prices lower than reality to remain conservative. Using my HOC profit model today and seeing the numbers at $2,400 an ounce is a salutary reminder that we are all in danger of undercooking the Turkey and not realising the profit opportunity in gold mining of higher prices.

Regards

The Oak Bloke

Disclaimers:

This is not advice

Micro cap and Nano cap holdings might have a higher risk and higher volatility than companies that are traditionally defined as "blue chip".