DEC-iphering the Ohio River Valley Institute’s critique

What noise for the Ted'n'Kathy "Sound Research"?

A year ago today Ted Boettner (he/him) and Kathy Hipple (pronouns unknown) (henceforth referred to as Ted’n’Kathy) wrote a follow up to their earlier 2022 article. Let’s examine their latest article.

“Earlier this year” - no, it was the year before, actually. Good start Ted’n’Kathy.

“..the company’s ability to pay” - the $445m already set aside by DEC (25% of its future ARO) is ignored no actual calculations are provided to disprove the mathematics set out by DEC and by the OB in DEC-tecting fact or fiction. Just a general dismissal and sowing seeds of doubt are felt to be sufficient by Ted’n’Kathy. Where are the actual empirical facts? I was expecting “Sound research”.

“Cash flows”, “Continue to pay" & “eliminate its debt obligations” - In the 12 months since this article DEC has demonstrably achieved all three. You can hear the aggrieved tone in Ted’n’Kathy’s writing already, where the desire to make an allegation stick appears to be first and foremost in their minds rather than present the evidence, the facts. Is there another motive at play in your “sound research” Ted’n’Kathy?

Within an hour of searching I found in DEC of Top Trumps several examples where DEC’s ARO relative to its production lifecycle is not only following but even exceeding industry norms. Assuming you agree EQT corporation, Williams, i3 energy, Seplat and Enquest are representative of course. It’s worth pointing out here that it is not just about “industry norms”. More accurately this is actually about common Accountancy Practice - including getting your numbers past an auditor - each year. Past a consortium of 14 banks with ESG criteria too. Past a number of ESG certifying authorities. Past a number of state regulators who agree your well retirement plans. Past the EPA. Nowhere in the “sound research” is the simple fact that accruing for a future cost is a standard practice in any business and the calculation made by DEC is based on the accounting standard of IAS37. Ted’n’Kathy don’t appear to understand this. Or if they do, they ain’t tellin’.

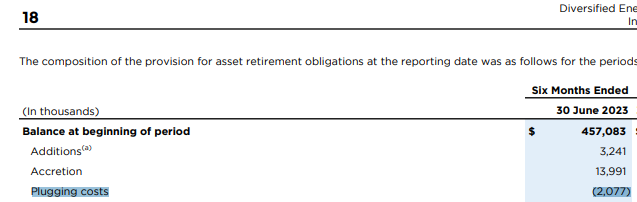

Assumption is an incorrect word. DEC’s audited accounts show $21,000 per well to be a fact ($20,770 to be precise).

Technically insolvent

Nor do Ted’n’Kathy appear to understand IFRS9. If only they’d subscribed to the Oak Bloke, reader. Ha! The OB explained in DEC-the-halls IFRS9, which again is proscribed accountancy practice, for accounting hedge liabilities, which assumes all future theoretical losses and settlements have to be presented as though they were settled in the current year.

“…by some definitions” Ted’n’Kathy, please, that’s laughable. There’s only one definition of insolvency in law, and DEC as a UK-listed entity is governed by UK law which says:

“….its own P&A costs are also questionable….”

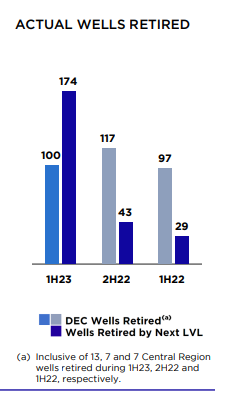

The repetition, the lack of common sense is starting to irritate me, Ted’n’Kathy. Surely you must understand that businesses will bid for work and they will price work based on making a profit. Nice work if you can get it, by the way, at $126k per well. If DEC (via NextLVL) is making those sorts of margins, based on 87 wells x 2 and $126k - $21k = $105k per well could have netted DEC $18.2m extra profit last year NICE!

Moreover, if DEC can make $18.2m a year profit plugging 3rd party wells that covers a the remaining ARO over the next 68 years. ($1.25bn/$0.018) (even before considering the $8bn PV10 future cash flows). Or even sooner, if only they grew their NextLVL operations. Oops, but they did.

By the way, I don’t think Ted’n’Kathy are correct in their claim or allegation (or “sound research”?) of $126k per well, and as has been pointed out in reader comments it depends on the wells, their depth, complexity - some wells can cost much more than others to plug. However we know the average over multiple periods - and the costs of plugging at competitors like i3e are in those ball parks. What if the price of P&A goes up in the future? So does gas. The whole point of NPV10 is the future value of gas is DISCOUNTED by 10% a year so to ensure things like ARO can be covered. So $8bn at NPV10 is actually something like $20-30bn in the future but which is worth $8bn in today’s money.

Using the same simplistic logic as Ted’n’Kathy appear to use that DEC is exploiting what appears to be portrayed as hapless State regulators (i.e. ignoring that business is a competitive process) then their own arguments actually prove DEC is well able to meet its ARO (even before the $8bn PV10 future cash flows).

And now for Ted’n’Kathy’s next own goal…IRA and Grants

Correct! Correct! Correct! Ted’n’Kathy, who seem so determined to paint a negative picture, don’t pause to think this criticism through….. $5.4bn of funds. Hmm.

The EIA tells us there are 912,000 Oil & Gas wells. Extrapolating the data from Statista gives us about 450,000 Natural Gas wells. 68,000 wells is 15% of US wells therefore. 15% of $5.4bn of funds is $816m. DEC’s total ARO is $1.7bn less $0.45bn that’s already been set aside.

So an ARO shortfall of $1.25bn where two thirds of that could be covered by grants?!!?!!?!!

Thanks Ted’n’Kathy!

But hang on… if NextLVL is hoovering up plugging contracts for States tackling orphaned wells (which actually is where much of the Federal Grants ARE directed if only Ted’n’Kathy had read OB’s research on MERP), then that number could be more like 30% of $5.4bn…. but that’s $1,632m. So $382m more than DEC’s ARO shortfall. So an ARO surplus (even before the $8bn PV10 future cash flows)! Are Ted’n’Kathy shuffling from foot to foot in embarrassment?

Can they win it back with Gain on Bargain Purchase?

To describe this as “uncommon” is just silly too. It demonstrates a lack of understanding. The definition is you typically have to consider a gain or loss when acquiring assets. See the definition below, courtesy of PWC’s web site. Typically does not mean uncommon, does it reader?

Why is a gain being made? I would reply the sellers are offloading non-core assets. Both the valuation and the lifespan can differ - and often do. Let me tell you a story to illustrate what I mean.

An analogy to conclude:

Let me tell you a story that illustrates why Ted’n’Kathy’s “sound research” is wrong.

Have you ever bought a car? Let us consider this BMW 4 Series. The seller was a guy called Bob. He was a salesman. He drove the car 30,000 miles a year for 3 years. The buyer (the Oak Bloke) hardly drives. Too busy writing DEC articles, day and night! Bob depreciated the BMW by £7,000 a year. Bob’s cars don’t last long as Bob is a busy lad. He sells fast and drives fast. Bob took the car to the BMW garage every year costing well over £500. What will the OB do? First of all Bob was desperate to sell. The OB took it off his hands at a great price. £12k. The OB recognises a gain on acquisition because he knows he can flog that Beemer for £3,000 more than he bought it. OB sold the same Beemer 6 months ago for £15,000 and made £3,000 profit. So the OB’s auditor is happy to recognise a gain on (bargain) purchase. The OB who hardly drives, will run that BMW for the next 20 years doing 4,500 miles a year. The OB is a master mechanic so pays the BMW garage zero. Once it gets to 180,000 miles it’s exhausted and the Oak Bloke will scrap it. Because the Oak Bloke knows he has 20 years to save up for another Beemer so puts aside £750 a year for the next 20 years (in a savings account so inflation doesn’t eat into it). So the OB’s depreciation is much less than Bob’s - for the same car. (Just to be clear that’s the OB’s equivalent to ARO). One day the government offers a scrappage scheme and will pay the OB £8k to scrap it in 10 years time. Nice! Another £2k profit on disposal!

Hopefully the Oak Bloke’s 4-series story summarises why Ted’n’Kathy are simply wrong. They appear to present a coherent story, and wrote an impressive looking report but it’s full of holes. I went through their web site to scrutinise using my 6 friends (What and Why and When And How And Where and Who). While Ted’n’Kathy do campaign vigorously for all sorts of issues in Appalachia - good for them - the basic logic on DEC is absent.

A final thought

Who funded Ted’n’Kathy to write that story about DEC? That’s what I want to know, Ted’n’Kathy. Do you disclose that? No! But I do notice you are a 9 person business, recruiting a 10th for $55k-$70k a year so someone must be funding. You’re not doing it out just for the love of ol’ Appalachia, it seems. Is it “Sound Research” to not disclose who funds you? O&G is an industry where M&A is rife, where off balancing DEC could be a sneaky tactic, or maybe some strategy to launch a takeover. Who knows why they spent so much time writing a 40+page report? What social justice did it serve exactly? Especially compared to their other articles which do seem to be more about actual social justice the DEC report seems to stand apart. Is the OB suffering paranoia reminiscent of Kazera Sosei. Or is it an intriguing and unanswered question?

What noise for the Ted'n'Kathy "Sound Research"? A raspberry, perhaps?!

Now if you’ll excuse me, I’ve got a BMW to drive.

This is not advice.

Oak

(Disclosure: I am a DEC shareholder which is why I write about DEC. No one funds me and I don’t recruit people for $55k-$70k a year to help. I write because it helps me be a better investor, it amuses me, and because sometimes the OB’s readers stick their hands in their pocket to donate to a charity the OB suggests and this gives the OB a warm fuzzy feeling that he’s achieving some good in the world).

I agree with most you write on DEC - not all but most. Irrespective of that, I appreciate the time and effort you give, and accordingly, I for one, was happy to give a donation in acknowledgement of such.

Oak. The investor bulletin boards are full of calculations on the ARO's of DEC. (The methane emission claims of Ohio River seem to be discredited already). The key disputed variables appear to be the the life expectancy of the portfolio and the anticipated future NG price required to provide cash to pay for ARO's and divs. I assume that you have been monitoring the gossip and that there is nothing that has shaken your confidence in your calcs